Update 325 — Economic Groundhog Day

No Shadows; Corporate Debt Clouding Horizon

The American debt binge is not limited to the national debt. As we will show below and in the next update, private debt has scaled up in recent years just as precipitously, to mix monetary metaphors.

We start today with a look at the financial health of US companies and the impact of corporate debt, now at record levels and climbing, on the prospects for a recession.

Best,

Dana

————

In an era of quantitative easing (QE) by the Fed and low interest rates following the financial crisis, US companies have loaded up with debt. Are the debt-fueled boom times over now that the Fed is tightening monetary policy, reversing QE, and raising interest rates? And does that imply a sharp contraction if companies are practically drowning in unsustainable debt?

High Debt at Low Interest

Over the past decade, total corporate debt in the US has risen to record levels, almost doubling from around $4.9 trillion in 2007 to nearly $9.1 trillion in 2018. In addition to its size, the quality of the debt is becoming a concern for regulators and lawmakers. Around half of investment-grade corporate bonds are one step away from “junk” status and loosely regulated borrowing, known as leveraged lending, has come to the fore as the primary mode of buying low-quality credit.

Seven S&P 500 companies owe over $90 billion of this debt, including household names such as Campbell’s Soup and Waste Management. This debt may be manageable in the short-term, but as interest rates continue to rise and the debt becomes ever more expensive to service, it could soon spiral out of control.

Fed Stability Report

Last November, the Fed released its Financial Stability Report, providing an overview of the health of the financial system. In the report, the Fed outlined four areas of vulnerability, one of which was excessive borrowing by businesses and households. Historically, heightened borrowing by businesses and households has resulted in major stress on consumers, as well as the financial system. Through the current expansion, total business sector debt grew faster than GDP and is now at a historically high rate relative to GDP.

Business debt levels show signs of increased risky debt issuance and deteriorating credit standards. Risky debt rose 5 percent over 2018 and represents about $2 trillion in outstanding debt:

- $1.2 trillion in leveraged loans

- $700 billion in private debt

The Fed’s report understates the danger this situation poses to the health of the economy. Former Fed Chair Janet Yellen believes this risky debt creates systemic risk and could become very problematic in an economic downturn. This past fall, Yellen was quoted saying, “If we have a downturn in the economy, there are a lot of firms that will go bankrupt, I think, because of this debt…it would probably worsen the downturn.”

Leveraged Lending — Canary in a Coal Mine?

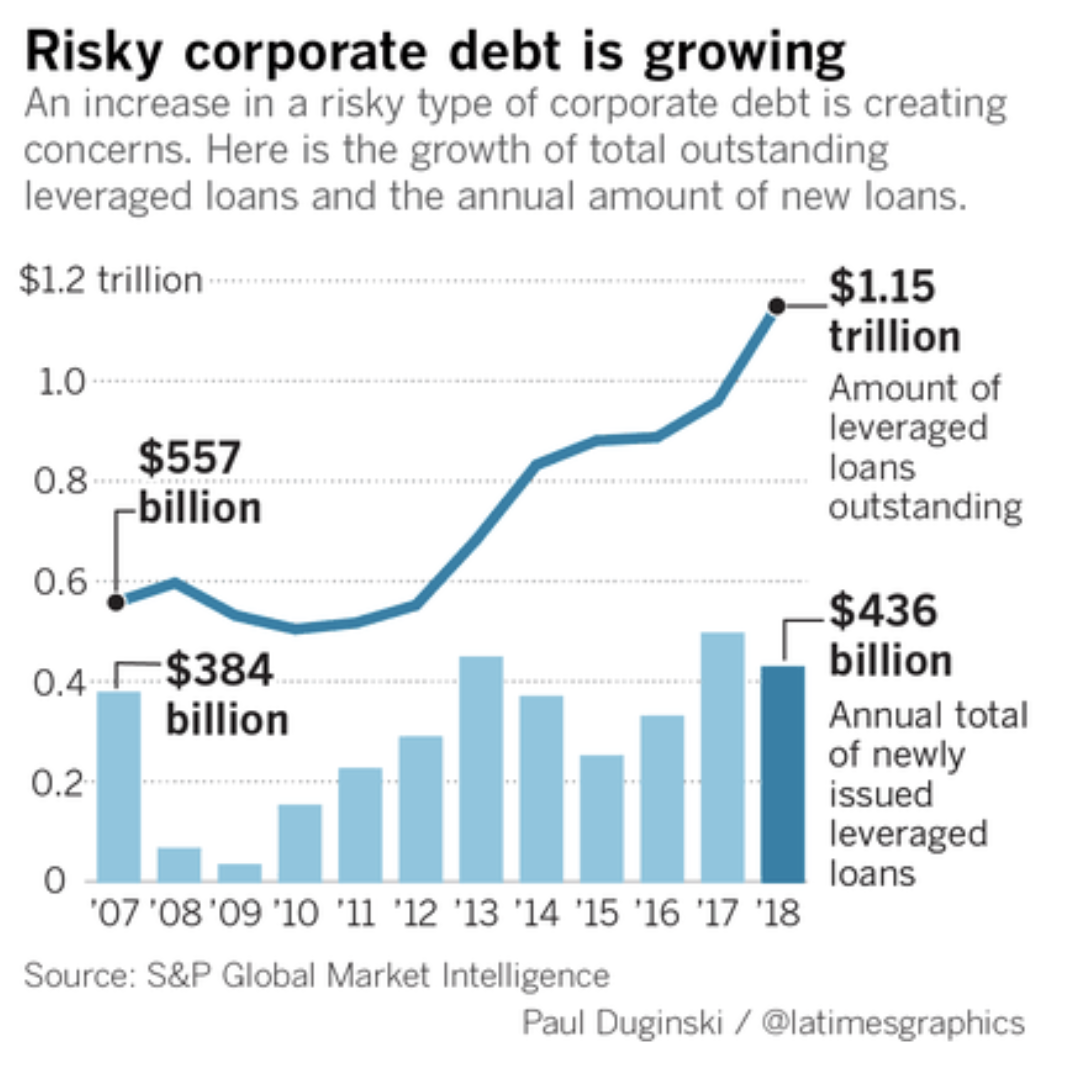

Of particular concern in the corporate debt market is the growth of so-called leveraged loans, a market now worth over $1 trillion. Leveraged loans are extended to companies already burdened with significant amounts of debt and/or with a poor credit history. Recently, they have surpassed the high-yield bond market as a source of cheap credit for these more indebted companies. In less than a decade, the leveraged loan market has grown from under $250 billion to $1.2 trillion, amid loosened regulatory oversight and investor protection regulation.

In late 2018, the turbulence in the stock market caused leveraged loan prices to stumble, drawing alarm bells from former Federal Reserve Chair Janet Yellen, the Bank of England, and the IMF. Policymakers and economists warn that the last-quarter drop in 2018 could only be a taste of what’s to come.

Source: Los Angeles Times

In November last year, Senator Elizabeth Warren joined the chorus of economists to warn about the imminent systemic risk to the financial system:

“Banks are making a record amount of loans to companies swimming in debt, then pushing the risk to investors. Just like the pre-2008 subprime mortgage market, it’s a ticking time bomb that could blow another hole in our economy.”

Regulators Acknowledging, But Not Acting

The regulators are watching, but are essentially unable to act. The Government Accountability Office decided that regulators overstepped their authority when the OCC, the Fed, and the FDIC issued joint supervisory guidance on leveraged lending in 2013. Banks are also shifting this risk on to other investors — it is increasingly small banks and nonbank lenders offering leveraged loans. Leveraged loans by large banks have declined from 80 percent in 2010 to just 54 percent in 2018.

Leveraged loans are slinking off into the shadows, leading to looser lending standards and worsening investor protections. As economic growth slows and the cost to service the debt increases, invariably more and more defaults on this debt will occur, leaving investors, the FDIC, and, ultimately, taxpayers and the rest of us holding the bag.

free dating near you

free personal ads

browse tinder for free , tinder online

what is tinder

tinder login, how to use tinder

tindr

aut medical centre book online Canon Digital Camera Solution Disk Cd-rom Gratuitement las animas year book 1979

Casino Saint Michel Marcel Langer Toulouse Gemo Geant Casino Jas De Bouffan Galerie Geant Casino Dijon

Galaxy J5 Memory Card Slot Casino En Ligne Belge Qui Accepte Les Francais Balance De Precision 0 01 G Geant Casino

dating sites

indian dating

Pingback: keto meal

gay s and m dating site

gay dating anonomous

gay dating groups

canadian pharmacy viagra quick delivery viagra amex – buy viagra from germany

columbus ohio gay dating

gay sex dating sites

gay strongmen dating

gay older dating

gay sugar baby dating free

is match good for gay dating