Update 324: Our Systemically Riskiest Markets

… Beyond a Shadow of a Notional Doubt

The long weekend ahead —or the furlough as the case may be — affords the opportunity to look at the little-understood but vast shadow banking system. Many firms involved in the 2008 financial crisis continue to operate in a relative regulatory void, known as the shadow markets.

What has changed, if anything, since the financial crisis? Anything to see here in the way of lingering or looming systemic threats lurking in the shadow banking markets?

Happy MLK long weekends to all.

Best,

Dana

————

Banking in the Shadows

Shadow banking is the term used to cover all financial intermediaries that perform certain financial functions, but are not regulated as banks. These financial intermediaries include insurers, pension funds, asset managers, real estate funds, and hedge funds. Some of the leading firms in the shadow markets include household names such as:

- Prudential Financial (insurer)

- Quicken Loans (nonbank lender)

- BlackRock (asset manager)

- Renaissance (hedge fund)

In 2018, shadow banking accounted for 13 percent of total global financial assets, according to the Financial Stability Board. It is highly interconnected with the financial system and, unlike depository institutions, much of its activities remain unregulated.

Shadow Sectors

Shadow market participants engage in a number of activities ranging from mortgage lending and derivatives trading to repurchase agreements and securities lending. In the latter three, hedge funds play an outsized role. The following sectors, each in their own way, but especially mortgage lending, were major players in the Great Recession.

Derivatives

Shadow banking activities are conducted in a set of markets like options contracts, which include futures and derivatives. The global derivatives market is valued at over $500 trillion in notional value — nearly 25 times the GDP of the United States. Repurchase agreements and securities lending largely exist outside of the purview of regulators and are a discounted systemic risk.

November’s Federal Reserve Stability Report highlighted concern over hedge fund leverage, suggesting that leverage in this sector is at post-crisis highs, about one-third over the course of 2016 and 2017: “the increased use of leverage by hedge funds exposes their counterparties to risks and raises the possibility that adverse shocks would result in forced asset sales by hedge funds that could exacerbate price declines.”

But despite the Fed’s report’s view that hedge funds don’t play an outsized role as other financial institutions in the economy, they are still systemically important:

- Regulators only receive limited data on hedge fund activity and exposures — a value judgment on their financial condition and their systemic risk cannot fully be made because it is based on incomplete information

- Interconnectedness — in comparison to assets managed by mutual funds and the big banks, hedge funds look small, but their role in the financial markets is much greater than just the assets on their balance sheet; the presence and activities of hedge funds in financial markets is significant enough to pose a systemic risk threat to the US economy, given their central role as financial intermediaries and their appetite for risky, unregulated margin trades and short-selling

- Their increasing leverage is also a concern — given the recent volatility in the US equities markets, a potential precipitous drop in liquidity for hedge fund investments — as in 2008 — could have disastrous consequences for the markets as they try to unload their portfolios, exacerbating stock price declines

Repurchase Agreements

Repurchase agreements, or repos, serve as short-term loans for hedge funds and other trading firms when exchanging mainly government securities for cash. The seller of the government security agrees to buy back the note a specific time and at a premium to the buyer. The size of the market is huge, with companies holding over $5 trillion in repos on a daily basis.

Hedge funds present an issue for the repo market because, in an unregulated market, they often make risky bets (short-selling and trading risky derivatives). These bets can lead to a situation whereby the hedge fund would need to liquidate a large amount of repos in a short period of time to cover the bad investment.

Securities Lending

Securities lending is loaning a stock, derivative or other security to an investor or firm. The borrower, usually a short-seller, is required to put up a certain amount of capital in case of financial distress. The risk in securities lending comes when the lender uses the cash generated by lending the security to invest in bad bets in the market.

In 2007, AIG’s securities lending portfolio swelled to $80 billion, up from $10 billion in 2001. It used this cash stream to invest invest heavily in residential mortgage-backed securities (we know how that turned out), resulting in the largest bailout ($180 billion) in US history. After the Dodd-Frank Act passed, the securities lending market was curtailed to some extent, shrinking to about a third of its pre-crisis size. Structurally, the securities lending market is still the same, opening the possibility for another AIG or Lehman.

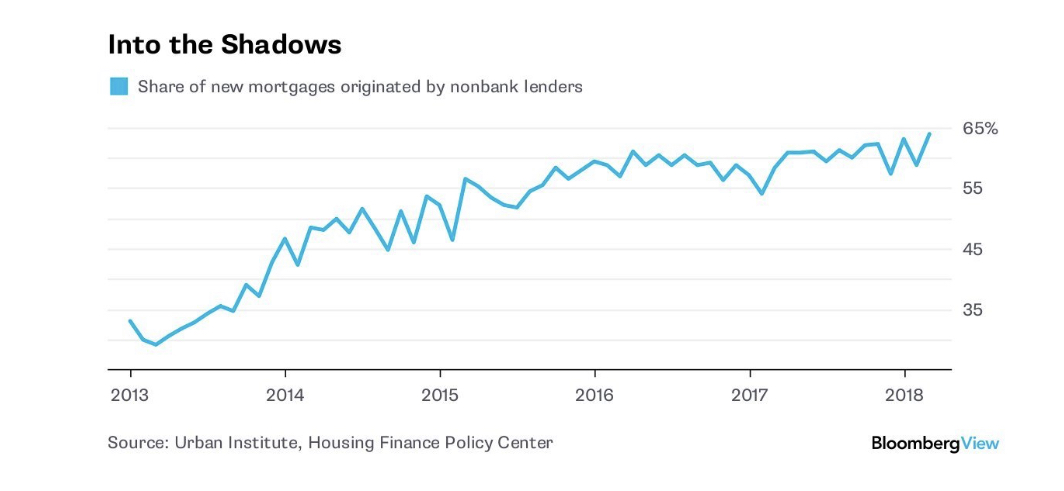

Nonbank Lending in the Housing Market

After the 2008 financial crisis, Dodd-Frank outlined numerous provisions designed to tightly monitor lending and reduce risks inherent in the US banking system, including new oversight councils, credit agency reforms, and increased capital requirements. Mortgages became harder to get, credit seemed to evaporate, and a loan approval became a rare event reserved for the lucky and the few.

The shadow mortgage market has taken up the pedestal left by traditional banking since the financial crisis. Unregulated lenders have recently increased their mortgage offerings to low-income and high-risk applicants. Without oversight and regulation, there is potential for customer abuse and risky lending practices.

Bringing the Shadows Into the Light

With the de-designation of the last nonbank SIFI (Systemically Important Financial Institution), the Financial Stability Oversight Council (FSOC) has chosen to do nothing about the risk from nonbank financial institutions, or the shadow market. Without the knowledge of how well shadow firms would fare under stress or what the process of their failure would look like, systemic risk can, and will, build-up undetected.

In 2010, Dodd-Frank gave the CFTC and the SEC authority to regulate over the counter (OTC) derivatives. As a result of the regulation, transactions and degrees of leverage must be reported, and major participants must be registered with the federal oversight agencies. The Dodd-Frank regulatory framework was a good first step in attempting to regulate shadow banking, but much more must be done.

Other Related Articles

- Update 735: Shutdown Threat In Temporary Remission

- Update 729 — House Elects Speaker: Can Bipartisan Fiscal Policy Follow?

- Update 728 — Suspended Animation:House Left Behind as the World Turns

- Update 722 — From Strikes to Shutdown: Challenges to the Post-Covid Recovery

- Update 720 — Weekly Economic Roundup