Update 764 — FOMC’s Dot Plot Thickens:

Fed Holds Rates Steady, Cut Timing Unsure

The Fed decided once again today to maintain its 5.25 to 5.50 percent interest rate, keeping rates at the same level since July, seeing neither an imminent resurgence in nor retreat from the annualized ballpark three percent inflation rate that has settled over the economy in recent months, forecasting a rate of 4.6 percent by year-end. How long will the Fed stick with its elevated, arguably contractionary rate policy, and how many cuts will we see this year once it does so?

Going into this week‘s FOMC meeting, the Fed has been signaling an easing of rates mid-year, with a total of three 25 basis point cuts in 2024. Today, Fed Chair Jerome Powell reiterated the Committee’s base case forecast of three cuts this year. What does this mean for American households? See below.

Best,

Dana

When will the Fed begin to cut and how many cuts can we expect this year? These were the big questions for the Federal Open Market Committee (FOMC), which opted to hold rates steady at the conclusion of its latest meeting this afternoon. Officials projected three cuts later this year, as they had in December, and projected additional cuts in 2025 and 2026, with rates remaining higher in those years than projected in December. The announcement comes as inflation has fallen drastically from its peak, as concerns grow for those bearing the weight of the Fed’s monetary policy tightening.

Fed Holds Rates Steady, Projecting Three Cuts This Year

The Federal Reserve has opted to hold the federal funds rate steady at the 5.25 to 5.5 percent range for the fifth consecutive occasion after hiking rates from near zero in early 2022 to a 23-year high in its most aggressive series of interest rate hikes since the early 1980s. In his press conference following the meeting today, Fed Chair Jerome Powell said that rates were likely at their peak.

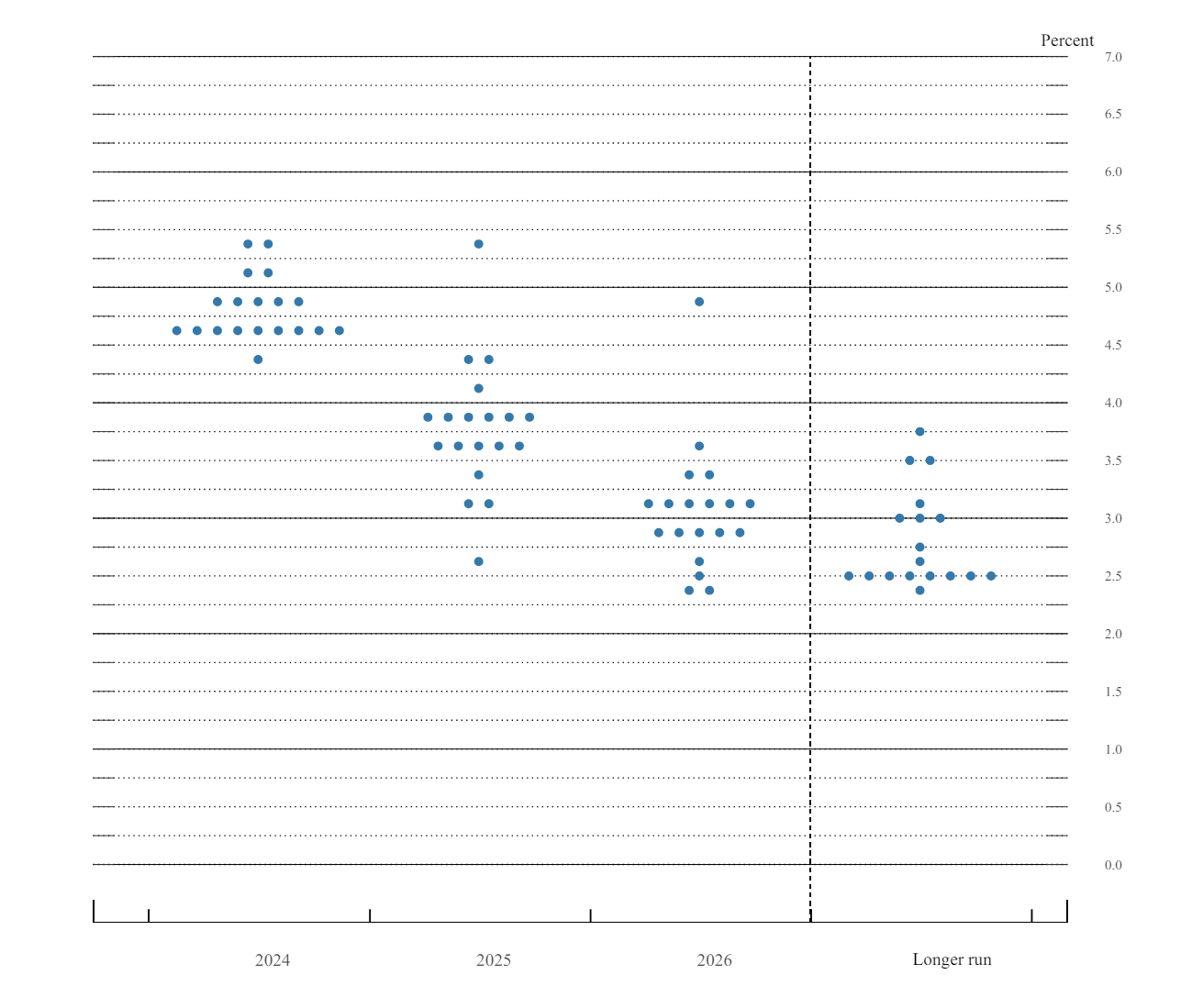

Committee officials projected that, if the economy continues to evolve as expected, interest rates would be cut by 25 basis points three times in 2024, bringing rates to 4.6 percent at the end of this year. Additionally, the Committee projected that they would cut rates to 3.9 percent by the end of 2025 and to 3.1 percent by the end of 2026. This is clear in the Fed’s “dot plots” shown below, released at the conclusion of this week’s meeting. At every other FOMC meeting, each Committee official indicates with a dot the midpoint of the target range they expect interest rates to reach in the current year, two following years, and in the longer run.

FOMC Participants’ Assessments of Appropriate Monetary Policy: Midpoint of Target Range or Target Level for the Federal Funds Rate (March 20, 2024)

Source: Federal Reserve, Summary of Economic Projections, March 20, 2024

Powell indicated that officials were still seeking greater confidence that inflation is moving sustainably toward the Fed’s target of two percent before it begins cutting rates. He stressed that he believes inflation is still too high to begin cutting rates. The median FOMC official projected that the Fed’s preferred gauge of inflation, the personal consumption expenditures (PCE) price index, which had fallen to 2.4 percent in January, would fall to 2.1 to 2.2 percent next year and to 1.9 to 2.0 percent in 2026.

Unnecessary Higher for Longer Interest Rates Risky

The Fed has held interest rates at the 5.25 to 5.5 percent range since July of last year, which has had implications for households and businesses throughout the economy. The burden of the Fed’s monetary policy will only become heavier as the Fed holds rates at an unnecessarily high level for an extended period of time. The remarkable economic resilience of the American economy in the face of the Fed’s rate hike cycle, in which economic growth and employment conditions have remained strong, is not certain to last as this has been driven in part by consumer spending.

The Fed initiated its current cycle of rate hikes in an effort to bring down inflation, which had briefly spiked to 7.1 percent in June 2022 as measured by the PCE. Most Americans may recall inflation as measured by another metric, the consumer price index (CPI), reaching a peak of nine percent..

Since then, the year-on-year change in the PCE has fallen to 2.4 percent, its lowest subsequent rate. On an annualized basis, both headline and core PCE, which strips out volatile food and energy prices, have moved toward the Fed’s two percent target. While Powell has acknowledged that inflation data over the past six months has been favorable, he remains adamant that the Fed must see continued data showing inflation coming down sustainably before it begins to cut rates. With the Fed’s inflation goal all but achieved, holding interest rates higher for longer results is unnecessary but not costless.

Ahead of this week’s meeting, 23 members of Congress, including Senator Elizabeth Warren (D-MA), highlighted exactly these concerns in a letter to Powell led by the Congressional Progressive Caucus. The members called on Fed officials to “develop a prompt timeline for future rate reductions.” In an additional letter citing the impact of high interest rates in blocking progress on green energy, Senators Warren and Sheldon Whitehouse (D-RI) urged the Fed “to cut interest rates throughout 2024.”

Interest Rates Heighten Debt Burden

Household and business balance sheets have become more strained. Households have largely exhausted savings accrued during the pandemic from reduced spending and government relief and student loan payments have resumed. Yet consumer spending has remained strong. Americans have turned to debt to support their spending. American household debt rose by over $600 billion last year to over $17 trillion. At the same time, the Fed’s monetary policy tightening has driven up interest rates on numerous forms of consumer debt.

Credit card debt is one example of this trend. Credit card interest rates reached their highest level in almost three decades last year, soaring to 22.8 percent. During that same period, Americans took on over $600 billion in credit card debt, bringing credit card debt in the United States to a record high of $1.13 trillion by year end. About ten percent of credit card borrowers now have an account balance over $5,000. This level of total credit card debt appears far from sustainable as households’ ability to bear the burden seems to be waning. Credit card delinquencies reached 8.5 percent, their highest level in a decade last year. The same pattern of increased interest rates, increased debt burden, and increased delinquencies is also clear when we look at auto loans.

Additionally, the Fed’s elevated interest rate policy has only exacerbated the affordable housing crisis. The average rate on the 30-year fixed-rate mortgage reached eight percent in October, deterring potential home buyers and inflating mortgage payments of landlords who may opt to pass those costs on to renters.

Approaching a Soft Landing Yet Risks Remain

The American economy appears to be in the final descent to a once-tentative soft landing, in which inflation is reduced without a significant negative impact on the labor market and broader economy. But continued unnecessarily high interest rates could still upend the strong consumer spending that has bolstered growth and made America’s post-pandemic economic recovery the strongest of the developed world. Furthermore, the Fed’s spate of interest rate hikes have a lag effect and will continue to ripple across the economy for months to come though lags in its full impact that may be hard to see through economic data. This may expose risks that may be difficult to predict and successfully respond to.

Over the course of the coming months, the Fed will have to weigh the risks of holding interest rates at an elevated level for too long against those of loosening monetary policy before the economic data reflects progress toward their target outcomes. The FOMC will meet next on April 30 and May 1. February PCE data, to be released next week, will give officials a clearer picture of inflation’s progress toward the Fed’s target.