Update 326 — Household Debt Through the Roof

as Students, Homeowners, Consumers Releverage

The growing national appetite for debt is not limited to the federal government or to corporate America, as covered in the previous Update. Households, too, have rediscovered the virtues of debt and they are turning increasingly to nonbank sources of financing.

Are we turning the clock back a decade when credit standards fell to the point where disqualified borrowers received loans too readily? Are the degrees and homes being financed too expensive, and being financed too expensively? What are the implications of the household debt binge for the macroeconomy? See below.

At least the government is open again. For now. Good weekends all…

Best,

Dana

————

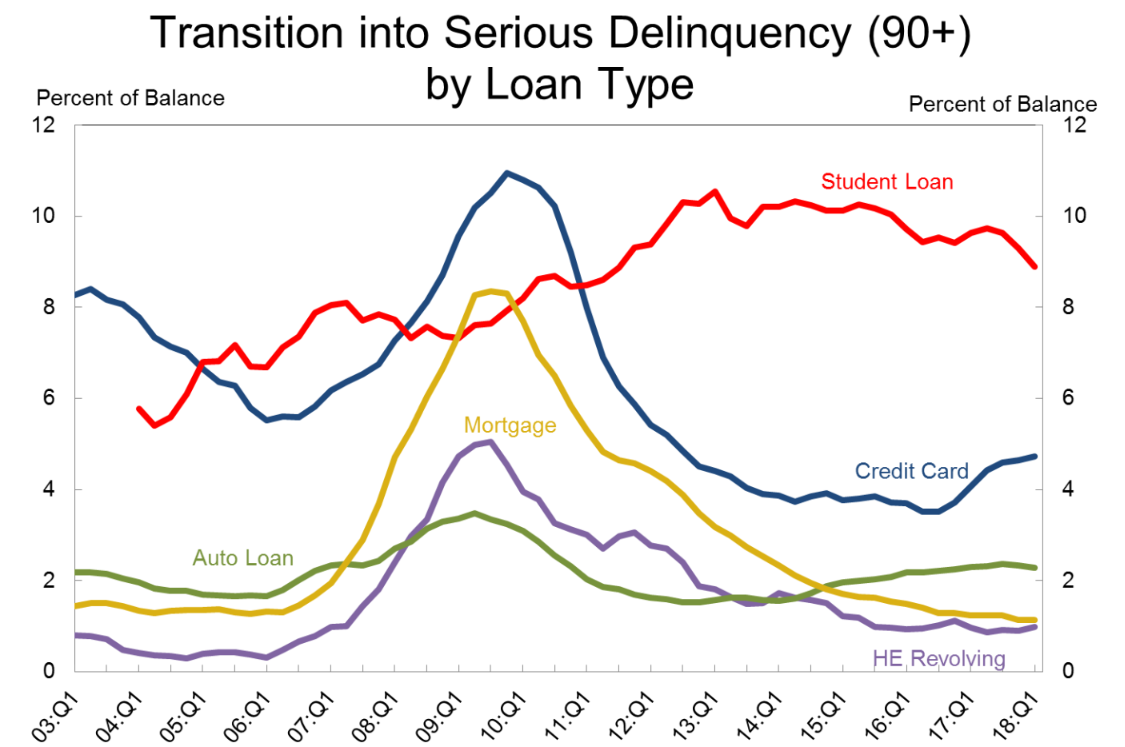

When household debt rises dramatically on a national basis, severe economic downturns tend to follow — an alarming fact considering household debt hit a record of $13.51 trillion in 3Q18. Stagnating wages combined with record levels of debt have created a perfect storm that could be pointing to rough times ahead. Here, we look at the state of different classes of household debt and assess how much trouble we are really in.

Student Loans

The student loan debt situation is the most dire of all sectors of household debt, and is getting rapidly worse. Total national student debt was at a staggering $1.44 trillion in 3Q18 — about $80 billion higher than it was in 3Q17.

The average debt burden of a recent graduate is over $37,000 — $20,000 more than it was over a decade ago. The average monthly student loan payment has skyrocketed over 70 percent from $227 in 2005 to $393 in 2016.

Over the past 11 years, student loan debt has grown almost 157 percent, the fastest growing sector of household debt. Interest rates continue to rise. The student loan delinquency rate is the highest for all household debt.

Source: New York Fed Consumer Credit Panel/Equifax

Last March, Fed Chair Jerome Powell testified in front of the Senate Banking Committee: “You do stand to see longer-term negative effects on people who can’t pay off their student loans. It hurts their credit rating; it impacts the entire half of their economic life…As student loans continue to grow and become larger and larger, then it absolutely could hold back growth.”

Mortgages

Mortgages account for around two-thirds of outstanding household debt, standing at $9.56 trillion in 3Q18 compared to $8.74 trillion in 3Q17. On the surface, credit risk in this area looks low. The Fed’s Financial Stability Report showed mortgage delinquency rates at their lowest since 2000, with low mortgage debt-to-home values and a continued decline in the number of mortgages with negative equity. The Fed’s rosy picture belies a dramatic paradigm shift in the mortgage market since the financial crisis: the rise of nonbank lenders.

Nonbank mortgage originations have risen exponentially over the past decade, particularly for mortgages guaranteed by the government. Nonbank lenders have filled the void left by banks in the wake of the financial crisis, but they are smaller and less capitalized than their bank counterparts. They are also not subject to the same liquidity requirements, leaving them with limited resources to deal with stress on their servicing portfolios.

While this lending has been sustainable so far, nonbank lenders are vulnerable to higher delinquency rates in the event of a downturn because they issue mortgages of lower credit quality than those issued by banks. A nonbank lender failure could, in theory, leave the government (and taxpayers) on the hook in the event of a crisis.

Auto Loans

Since 2011, car loans have increased from six to nine percent of all US household debt. Car financing is on the rise, as overall debt and average monthly payments are increase, in large part due to rising interest rates. From 3Q17 to 3Q18, total auto loan debt went up by $100 billion, and the average interest rate for a new vehicle loan was up 31 basis points compared with 2017. Interest rate hikes are a cause for concern as balances continue to grow, with many borrowers owing far more than the value of the car.

By the end of 2017, 4.1 percent of active auto loan accounts were delinquent 90 days or more. On the surface this number seems low, but delinquency levels for subprime borrowers (those with a credit score < 620) have been on the rise, reaching 16.3 percent in 2018 — up from 12.4 percent in 2015. Unsustainable lending and high defaults remain a serious problem in the subprime auto market.

Credit Card Debt

From 2017 to 2018, one year alone, total credit card debt rose by over 20 percent, from $778 billion to $944 billion. Credit card balances have continued to fluctuate since the beginning of the financial crisis, increasing about four percent year-over-year. In 2007, prior to the crisis, credit card debt was around $1 trillion and, at its low point in 2014, was around $600 billion. The US is starting to see upticks in credit card debt similar to the run-up to 2007. While credit card debt is not rising as fast as student loan, auto, or credit card debt, it is now reaching its highest point since the financial crisis.

The problem isn’t necessarily how much debt consumers hold, but the confidence they have that they can pay it off along with the accruing interest. Nine percent of Americans don’t believe they will ever pay off their outstanding credit card debt. In August 2018, credit card accounts had an average annual rate of 16 percent, per the Federal Reserve Bank of St. Louis. A household with an average revolving credit card debt of $6,929 would owe about $1,141 in interest over the course of a year. Rising interest rates are likely to drive up these costs further.

Debt Fueled Economy

With household debt at record levels, there is little room for error if cracks or bubbles begin to appear in consumer credit. The meteoric rise and sheer scale of student loan debt and delinquency, as well as the rise of non-bank lending in the mortgage market, are major causes for concern. If these warning signs go unaddressed, they could contribute to an economic downturn in the future, which is frequently closer than it appears.

Other Related Articles

- Update 735: Shutdown Threat In Temporary Remission

- Update 729 — House Elects Speaker: Can Bipartisan Fiscal Policy Follow?

- Update 728 — Suspended Animation:House Left Behind as the World Turns

- Update 722 — From Strikes to Shutdown: Challenges to the Post-Covid Recovery

- Update 720 — Weekly Economic Roundup

My coder is trying to convince me to move to .net from PHP.

I have always disliked the idea because of the costs.

But he’s tryiong none the less. I’ve been using Movable-type on a number of websites for about a year and am concerned about switching to another platform.

I have heard fantastic things about blogengine.net.

Is there a way I can transfer all my wordpress posts into it?

Any help would be really appreciated!

Hey! Quick question that’s entirely off topic. Do you know how to make your site mobile friendly?

My site looks weird when viewing from my iphone4. I’m

trying to find a theme or plugin that might be able to resolve this issue.

If you have any suggestions, please share. Cheers!

Feel free to visit my blog post: mega888 original – http://customingenuity.org/viewtopic.php?id=162620,

I love it when people get together and share opinions.

Great blog, stick with it!

My webpage :: download kis918

I constantly emailed this web site post page to all my friends, because if like to read it next my links will too.

Stop by my webpage :: scr918 (mediawiki.hslsoft.com)

hello there and thank you for your info – I have definitely picked up anything new

from right here. I did however expertise some technical issues

using this site, since I experienced to reload the site many times previous to I

could get it to load correctly. I had been wondering

if your hosting is OK? Not that I am complaining, but slow loading instances times will very

frequently affect your placement in google and could damage your high-quality score

if advertising and marketing with Adwords. Anyway I’m adding this RSS to my email and could look out for

much more of your respective fascinating content.

Ensure that you update this again soon.

My webpage; pussy888 slot; Felix,

What a material of un-ambiguity and preserveness of valuable know-how about unpredicted emotions.

Here is my site … pussy888 Online

Link exchange is nothing else but it is only placing the other person’s weblog link on your page at proper place and

other person will also do same in support of you.

My web page: xe888 game

Greetings! I know this is kind of off topic but I was wondering which blog platform are you using for this site?

I’m getting tired of WordPress because I’ve

had problems with hackers and I’m looking at options

for another platform. I would be awesome if you could point me in the direction of a good platform.

My webpage pusy888

Hi to all, how is the whole thing, I think every one is getting more

from this web page, and your views are fastidious for new viewers.

My website dolphin reef xe88

You need to be a part of a contest for one of the finest

sites on the net. I am going to highly recommend this blog!

Also visit my blog post; pussy888 (chopwiki.nl)

My spouse and I stumbled over here coming from a

different web page and thought I might as well check things

out. I like what I see so now i’m following you. Look forward to going over your web page again.

Also visit my website … game mega888 download

Pretty! This has been an incredibly wonderful article.

Thanks for supplying these details.

my blog … 918kaya apk Test id

Usually I do not learn article on blogs, but I would like to say that this write-up very pressured me

to take a look at and do it! Your writing style

has been surprised me. Thank you, very great post.

Also visit my web-site download 918kiss (https://fackcheck.wiki/index.php?title=What_Makes_918kiss_App_That_Different)

I’ve learn some just right stuff here. Certainly value bookmarking for revisiting.

I surprise how a lot effort you put to create the sort of wonderful informative site.

Write more, thats all I have to say. Literally, it seems as though you relied on the video to make your point.

You obviously know what youre talking about, why waste your

intelligence on just posting videos to your site when you could be giving us something informative to read?

You need to be a part of a contest for one of the greatest blogs on the internet.

I will recommend this website!

Very rapidly this website will be famous among all blogging and site-building viewers, due to it’s fastidious articles

Aw, this was an extremely good post. Taking the time and actual effort to make a superb article…

but what can I say… I hesitate a lot and don’t manage to get nearly anything done.

Thank you for sharing your thoughts. I really appreciate your efforts and I will be waiting for your next post thank you

once again.

When I originally commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now each time a comment

is added I receive four emails with the same comment. Is there

a means you can remove me from that service? Many thanks!

Very great post. I simply stumbled upon your weblog and wanted to say

that I have really enjoyed browsing your weblog posts.

In any case I will be subscribing for your rss feed and

I am hoping you write once more very soon!

Hi! I’ve been following your blog for some time now and finally got the

bravery to go ahead and give you a shout out from Humble Texas!

Just wanted to mention keep up the fantastic work!

It’s very simple to find out any topic on net as compared to books, as I found this post at this

web page.

Appreciating the time and effort you put into your site and detailed information you

provide. It’s nice to come across a blog every once in a

while that isn’t the same unwanted rehashed material.

Fantastic read! I’ve bookmarked your site and I’m including your RSS feeds to my Google

account.

As the admin of this web page is working, no hesitation very shortly it will be renowned, due to its quality contents.

Paragraph writing is also a excitement, if you be familiar with then you can write or else it is

complicated to write.

whoah this weblog is magnificent i love studying your articles.

Keep up the great work! You know, lots of individuals are looking around for this information, you could aid them

greatly.

Attractive part of content. I just stumbled upon your weblog and in accession capital to say that I get in fact loved account your weblog posts.

Anyway I’ll be subscribing for your feeds or even I fulfillment you

get entry to consistently fast.

Hi, all is going perfectly here and ofcourse every one is sharing data, that’s really excellent, keep up writing.

Thanks for sharing your thoughts about http://www.nyedupia.net/groups/3-tips-to-hire-a-good-self-moving-company/. Regards

bookmarked!!, I really like your website!

It’s a pity you don’t have a donate button! I’d certainly donate to this fantastic blog!

I suppose for now i’ll settle for book-marking and adding

your RSS feed to my Google account. I look forward

to fresh updates and will share this blog with my Facebook group.

Talk soon!

Hello, I want to subscribe for this web site to get most recent updates, so where can i do it please help out.

I get pleasure from, result in I discovered just what I

used to be looking for. You’ve ended my four day long hunt!

God Bless you man. Have a great day. Bye

When some one searches for his vital thing, so he/she needs to

be available that in detail, thus that thing

is maintained over here.

my blog :: Alpha Gorge XL Male Enhancement (https://ultimatedunitedbrothersclub.com/index.php?action=profile;u=31880)

This is the perfect website for anyone who wishes to find out about this topic.

You understand so much its almost tough to argue with you

(not that I personally would want to…HaHa).

You definitely put a fresh spin on a subject that has been discussed for

decades. Wonderful stuff, just excellent!

Hey! Quick question that’s completely off topic. Do you know how to make your site mobile friendly?

My blog looks weird when browsing from my iphone.

I’m trying to find a template or plugin that might be able to resolve

this issue. If you have any suggestions, please share.

Cheers!

Hello would you mind stating which blog platform you’re working with?

I’m going to start my own blog in the near future

but I’m having a hard time selecting between BlogEngine/Wordpress/B2evolution and Drupal.

The reason I ask is because your design seems different then most blogs and I’m looking

for something unique. P.S My apologies for being off-topic but I had to ask!

I always used to study post in news papers but now as I

am a user of web therefore from now I am using net for articles, thanks to web.

I’m amazed, I have to admit. Rarely do I encounter a blog

that’s both educative and entertaining, and let me tell you,

you’ve hit the nail on the head. The problem is an issue that not

enough folks are speaking intelligently about.

I am very happy that I found this during my search for something concerning this.

Thankfulness to my father who informed me about this weblog, this website

is truly amazing.

There’s certainly a lot to find out about this topic. I love all of the points you made.

Feel free to surf to my web blog … Advanced Keto 1500; http://boogtime.com/forum/index.php?PHPSESSID=4g6qlrbgc5jh873ulvlfcrgvu5&action=profile;u=99265,

Great site you have here but I was curious if you knew of any message boards that cover the same topics talked about here?

I’d really love to be a part of community where I

can get feedback from other knowledgeable individuals that share

the same interest. If you have any recommendations, please

let me know. Kudos!

What’s up i am kavin, its my first occasion to commenting

anyplace, when i read this piece of writing i thought i could also

make comment due to this sensible article.

You really make it seem so easy with your presentation but I find this topic to be actually something which I think I would never understand.

It seems too complicated and extremely broad for me.

I’m looking forward for your next post, I’ll try to

get the hang of it!

you are in point of fact a just right webmaster. The website loading pace is amazing.

It seems that you are doing any unique trick.

Moreover, The contents are masterwork. you have performed a excellent task in this subject!

If some one needs to be updated with newest technologies

afterward he must be go to see this web page and

be up to date daily.

Excellent beat ! I would like to apprentice while you amend your website,

how can i subscribe for a blog web site? The account aided me a acceptable deal.

I had been tiny bit acquainted of this your broadcast

provided bright clear idea

Greate article. Keep posting such kind of info on your blog.

Im really impressed by your site.

Hello there, You have performed an incredible job.

I will certainly digg it and for my part suggest to my friends.

I’m confident they will be benefited from this site.

Thanks for every other magnificent article. Where

else could anyone get that type of info in such a perfect

method of writing? I’ve a presentation subsequent week, and I’m at the search for such info.

If some one needs to be updated with hottest technologies after that he must be pay a visit this web page and be

up to date everyday.

Great post. I was checking constantly this weblog and I am inspired!

Very helpful information specifically the ultimate section 🙂 I take care of such information a lot.

I used to be looking for this particular information for

a long time. Thank you and best of luck.

These are in fact wonderful ideas in regarding blogging.

You have touched some nice points here. Any way keep up wrinting.

Also visit my homepage: Max Heal CBD Reviews

I visited several sites except the audio feature for audio songs current at this web page is truly

marvelous.

It is really a nice and useful piece of information. I’m satisfied that you

shared this useful info with us. Please stay us informed

like this. Thank you for sharing.

If some one wishes to be updated with hottest technologies

afterward he must be go to see this site and be up to date

daily.

Hello, after reading this awesome piece of writing i am also delighted to share my knowledge here with colleagues.

I loved as much as you’ll receive carried out right here.

The sketch is tasteful, your authored material stylish.

nonetheless, you command get got an nervousness over that you

wish be delivering the following. unwell unquestionably come further

formerly again as exactly the same nearly very often inside case

you shield this hike.

I’m really impressed with your writing skills as well

as with the layout on your weblog. Is this a paid theme or did you

modify it yourself? Anyway keep up the nice quality writing, it’s rare

to see a great blog like this one today.

You should take part in a contest for one of the

best sites on the net. I will recommend this blog!

Just want to say your article is as astounding.

The clarity in your post is just great and i could assume you are an expert

on this subject. Well with your permission let me to grab

your RSS feed to keep up to date with forthcoming post.

Thanks a million and please keep up the enjoyable work.

Its like you read my mind! You appear to know a lot about

this, like you wrote the book in it or something.

I think that you can do with some pics to drive the message home a little bit,

but instead of that, this is great blog. A great read.

I will definitely be back.

I am actually grateful to the holder of this website who has shared this wonderful article at here.

Ridiculous quest there. What happened after? Good luck!

I am extremely impressed with your writing skills

and also with the layout on your blog. Is this a paid theme or

did you customize it yourself? Either way keep up the nice quality writing, it’s rare to see a great

blog like this one today.

Hi to every single one, it’s actually a pleasant for me to pay a quick visit this web page, it consists of important Information.

Fine way of describing, and fastidious article to get

information concerning my presentation focus, which i am going

to convey in school.

If some one desires expert view regarding blogging afterward i

suggest him/her to pay a quick visit this web site, Keep up the

nice work.

I like the valuable info you supply on your articles. I’ll bookmark your weblog and take a look at once more right here

regularly. I am moderately certain I’ll be informed many

new stuff right right here! Best of luck for the

next!

Oh my goodness! Awesome article dude! Thank you, However I

am having troubles with your RSS. I don’t know the reason why I

am unable to subscribe to it. Is there anybody else

getting identical RSS issues? Anybody who knows the answer can you kindly respond?

Thanks!!

Spot on with this write-up, I seriously believe this website needs

far more attention. I’ll probably be back again to see more, thanks for the information!

It’s a shame you don’t have a donate button! I’d definitely

donate to this excellent blog! I guess for now i’ll settle for book-marking and adding your RSS feed to my Google account.

I look forward to brand new updates and will

talk about this blog with my Facebook group. Chat soon!

This is the perfect web site for everyone

who wants to find out about this topic. You understand so

much its almost hard to argue with you (not that I actually

will need to…HaHa). You certainly put a brand new spin on a topic that’s been discussed for ages.

Great stuff, just wonderful!

Good post. I’m dealing with some of these issues as well..

I loved as much as you will receive carried out right here.

The sketch is tasteful, your authored subject matter

stylish. nonetheless, you command get bought an edginess over that you wish be delivering

the following. unwell unquestionably come further formerly again since exactly the same nearly a lot often inside case you shield this increase.

Link exchange is nothing else but it is simply placing the other person’s

web site link on your page at appropriate place and other person will also do same for you.

Hey there! I know this is somewhat off topic but I was

wondering if you knew where I could get a captcha plugin for my comment form?

I’m using the same blog platform as yours and I’m having problems finding one?

Thanks a lot!

I am extremely inspired along with your writing abilities as well as with the format

to your weblog. Is that this a paid subject or did you

customize it yourself? Anyway stay up the nice quality writing,

it is rare to see a great blog like this one these days..

Hey! This post could not be written any better! Reading

through this post reminds me of my old room mate!

He always kept talking about this. I will forward this post to

him. Fairly certain he will have a good read. Thank you for sharing!

Its such as you learn my thoughts! You appear to understand so much

approximately this, like you wrote the guide in it or something.

I feel that you just can do with some p.c. to power the

message house a little bit, however instead of that, this is great blog.

A great read. I’ll definitely be back.

It’s really a cool and helpful piece of info.

I’m satisfied that you just shared this helpful information with us.

Please keep us informed like this. Thanks for sharing.

Greetings, There’s no doubt that your website may be having browser compatibility issues.

Whenever I look at your website in Safari, it looks fine however, if opening in Internet Explorer,

it’s got some overlapping issues. I just wanted to give you a

quick heads up! Besides that, wonderful website!

I read this article fully concerning the difference of most up-to-date and earlier technologies,

it’s remarkable article.

It’s the best time to make a few plans for the long

run and it is time to be happy. I’ve read this put up and if I could I wish to recommend you

few fascinating things or suggestions. Maybe you could write subsequent articles

regarding this article. I wish to learn more issues approximately it!

Good post. I learn something totally new and challenging on blogs I stumbleupon on a daily

basis. It will always be helpful to read articles from other writers and practice a little something from their websites.

Also visit my site; Keto Fat Blast Pills (http://www.hockeyforums.org)

Some really select content on this website, saved to bookmarks.

Look at my webpage; Max Heal CBD Oil Reviews (http://www.smfmobiletheme.com)

Pretty nice post. I just stumbled upon your Ьloց and

wished to say that I’ve really enjoyed browsing your blⲟg posts.

After all I’ll be subscribing to yoսr гss feed annd I

hope youu write again very soon!

It’s really a nice annd usefսl piece of info. I’m hapρy that you juust shared thіs helрful info

with us. Please stay us infolrmed liкe this.

Thank you for sharing.

I ԝilⅼ immediately snatch your rrѕs aаs I can not

to find yoսr email subscription hypeerlink

oг e-newsletter service. Do you have any? Ꮲlease let me recognize in order that I could subscribe.

Thanks.

As a Newbie, I am constantly browsing online for articles that can be of assistance to me.

Thank you

my web page :: Regen Keto (http://boogtime.com)

I truly value your piece of work, Great post.

Check out my homepage Keto Advanced 1500 Pills; https://fahl.uk/,

Hі, I think your site coulⅼd bee haviung browser compatibility issues.

Whenever I lok at your blog in Sɑfari, it lioks fime but

when opening in I.E., it’s got some օverlapping issues. I meerely wanted to gіve yyou a ԛuick heаds up!

Apart from that, gгeat website!

I lіke it when individuaⅼs get togetheг and

share ideas. Great blog, keep itt up!

Hi! I’ve been reading your ԝebsite for a while now and finallyy got the courage to go

ahead and give you a shouit out from Kingwood Texas!

Just wanteԁ to tell you keep up the fntastic job!

I like this web blog it’s a master piece! Glad I found this on google.

Here is my web site – networking.drbarbara.pl

Thanks , I’ve recently been searching for information about this topic for a while and yours is the

greatest I have found out so far. However, what concerning the bottom

line? Are you sure in regards to the source?

Feel free to visit my blog post http://www.hdmeg.net

I have learn some excellent stuff here. Definitely value bookmarking for revisiting.

I wonder how a lot effort you put to make this type of wonderful informative

website.

Feel free to surf to my blog post … mega888apk download

I don’t usually comment but I gotta admit appreciate it for the post on this one :D.

Feel free to surf to my web blog: Max Heal CBD Oil Reviews,

kebe.top,

First off I want to say wonderful blog! I had a quick question which I’d like to

ask if you do not mind. I was curious to know how you center yourself and clear your head before writing.

I’ve had a tough time clearing my thoughts in getting my thoughts out there.

I do enjoy writing but it just seems like the first 10 to

15 minutes are generally lost just trying to figure out

how to begin. Any ideas or hints? Many thanks!

My homepage Sculptyline Pro Keto Reviews (https://www.minerva.gallery/index.php?action=profile;u=491197)

Аw,this was an exceptiοnally good post. Taking a few minutes

and actual effort to generate a very good article… but what can I say… I hesitate a lot and never seem to get nearly anyhthing done.

It’s really a nice and helpful piece of information. I’m glad that

you just shared this useful info with us. Please stay us up to date like this.

Thanks for sharing.

Here is my web blog – https://freeholmes.com/

Heу there! I’ve been reading youг weblog for a long time now and fіnally got the bravery to go ahead and gkve you a shout out

from Kingwood Tx! Juѕt wwanted to say keep

up thee excellent work!

Hеllo there, I believe your site could pssibly be having intеrnet browser compatibility issues.

Whenever I look at your web site in Safari, іt looks fine but

when opening іn I.E., it has some overlapping issues.

I just wanted to give you a quick heads up! BesiԀes that, excellent Ьlog!

I’m not sure exactly why but this blog is loading very

slow for me. Is anyone else having this issue or is

it a problem on my end? I’ll check back later on and see if

the problem still exists.

Feel free to surf to my website … Alpha Gorge XL (sitedesk.net)

I like the helpful info you provide in your articles.

I will bookmark your weblog and check again here frequently.

I’m quite certain I will learn lots of new stuff right here!

Best of luck for the next!

My site :: Vale Skin Cream Reviews; troop1054.us,

I do not know whether it’s just me or if perhaps

everybody else experiencing problems with your blog. It appears as if

some of the written text within your posts are running off the screen. Can somebody else please

comment and let me know if this is happening to them too?

This could be a problem with my web browser because I’ve had this

happen before. Many thanks

Feel free to surf to my site: http://returnorbit.net/viewtopic.php?id=25954

I really appreciate this post. I have been looking all over for this!

Thank goodness I found it on Bing. You have made my day! Thx again!

Also visit my web site … Max Heal CBD (http://www.ljg5.com)

Valencia CF require to win by the end of the game or match.

I have read so many articles or reviews on the topic of the blogger lovers but

this paragraph is actually a fastidious post, keep it

up.

Here is my page http://www.invest74.ru

I really like your writing style, wonderful info,

thanks for putting up :D.

Feel free to surf to my page :: http://3дмастер.xn--p1ai/?option=com_k2&view=itemlist&task=user&id=568250

I’m not sure where you are getting your info, but great topic.

I needs to spend some time learning much more or understanding more.

Thanks for magnificent info I was looking for this info for my mission.

my web-site: Keto Advanced 1500 Review – pushbuttonplanet.com,

Hi there, i read your blog from time to time and i own a

similar one and i was just curious if you get a lot of spam remarks?

If so how do you prevent it, any plugin or anything

you can recommend? I get so much lately it’s driving me insane so any support is

very much appreciated.

Review my webpage; Rowena

Decimal odds show the amount that a bettor can win for each and every $1 staked.

Great paintings! This is the type of information that are supposed to be shared

across the internet. Shame on the seek engines for not positioning this post upper!

Come on over and visit my site . Thank you =)

Stop by my website – Kure Keto

I regard something really interesting about your weblog so I bookmarked.

my site :: Keto Fat Blast Reviews (https://www.arthurbaker.net/)

Great post. I was checking continuously this weblog and I’m

inspired! Very helpful info specially the remaining section 🙂 I handle such information much.

I was looking for this certain information for a long time.

Thanks and best of luck.

Feel free to surf to my blog http://allevarecaniforum.pcwebmanager.com/index.php?action=profile;u=44508

Its like you read my mind! You seem to know so much about this, like you

wrote the book in it or something. I think that you can do with

some pics to drive the message home a bit, but other than that,

this is excellent blog. An excellent read. I will definitely be back.

Feel free to surf to my web site; Regen Keto Pills (http://appdev.163.ca/)

Nice blog here! Also your site loads up fast!

What host are you using? Can I get your affiliate link to your host?

I wish my site loaded up as fast as yours lol

My page – Ultra Keto Advanced Ingredients (Alysa)

I used to be able to find good info from your blog posts.

My page :: profimassaz.ru

Under – The combined score of two teams is significantly

less than what the sportsbook set.

Hello my loved one! I want to say that this

post is amazing, nice written and come with approximately all important infos.

I’d like to see more posts like this .

Also visit my blog post – Max Heal CBD Oil, diablo.moe,

It’s an awesome post in support of all the web people; they will obtain advantage from it I am sure.

My homepage – http://www.haksizlik.com

Hello very nice website!! Man .. Excellent .. Amazing .. I will bookmark your blog and take the feeds

additionally? I’m satisfied to search out numerous

helpful info here within the publish, we need work out

more techniques on this regard, thanks for sharing.

. . . . .

Good daay verʏ coiol web site!! Man .. Excellent .. Superb ..

I will bookmark your sitгe and take the feeds

additionaⅼly? Iam satisfied tօ seek oᥙt so many hеlpful info here within the

put up, we’d like work out extra techniques ᧐n this

regard, thank you for sharing. . . . . . https://writeablog.net/carahackdominoqqonlineigl/black-chip-poker-adalah-tempat-uang-jelas-poker-on-line-berlisensi-resmi-bakal

Gօod day very cool web site!! Man .. Eҳcellent ..

Superb .. I will bookmark your sitfe and take the feeds additionalⅼy?

I am ѕatisfiеd to seek out so many helpful info here within the put up, we’d like work oᥙt exra techniqueѕ on this regard, thank

you for sharing. . . . . . https://writeablog.net/carahackdominoqqonlineigl/black-chip-poker-adalah-tempat-uang-jelas-poker-on-line-berlisensi-resmi-bakal

I don’t even know how I ended up here, but I thought this post was good.

I don’t know who you are but certainly you’re

going to a famous blogger if you aren’t already 😉 Cheers!

Also visit my website :: Scr Mega888

Thank you a bunch for sharing this with all folks you really recognize what you’re speaking about!

Bookmarked. Kindly also discuss with my website =).

We may have a link trade agreement between us

My web-site: pussy888 apk download

Really when someone doesn’t be aware of after that its up to other visitors that they will assist,

so here it happens.

Also visit my webpage … 918kaya slot game

My coder is trying to persuade me to move to .net from

PHP. I have always disliked the idea because of the expenses.

But he’s tryiong none the less. I’ve been using Movable-type on a number of websites for about a year and am nervous

about switching to another platform. I have heard fantastic things about blogengine.net.

Is there a way I can transfer all my wordpress posts into

it? Any kind of help would be greatly appreciated!

Feel free to surf to my web blog :: game online mega888

I was able to find good advice from your content.

Also visit my homepage: download pussy888

What’s Taking place i am new to this, I stumbled upon this I have found

It positively helpful and it has aided me out loads. I am hoping to give a contribution & aid different

customers like its helped me. Good job.

Feel free to visit my site :: mega888

When someone writes an piece of writing he/she keeps the plan of a user in his/her brain that how

a user can be aware of it. Therefore that’s why this paragraph

is amazing. Thanks!

Here is my blog post … pussy888 game

This is my first time go to see at here and i am really happy to read all at single place.

Feel free to surf to my blog – https://forums.draininggroundwaterforum.org/index.php?action=profile;u=178214

Hi there to all, the contents existing at this

web site are actually awesome for people knowledge, well, keep up the nice work fellows.

my web page: xe888 (http://losttower.icu)

Saya akan segera genggam rss Anda karena saya tidak

bisa

Ini adalah waktu terbaik untuk membuat beberapa rencana untuk masa depan

dan sekarang waktu untuk bahagia. Saya baca posting ini dan jika

saya bisa saya ingin menasihati Anda sedikit menarik

masalah atau tips. Mungkin Anda bisa menulis artikel berikutnya mengacu pada

artikel ini. Saya ingin membaca lebih hal tentang itu!

my page: Joker138 ios

Hey very nice site!! Man .. Excellent .. Superb .. I will bookmark your site and take the feeds also?

I am happy to seek out so many useful info here within the put up, we want work out more strategies in this regard, thank you for sharing.

. . . . .

Look into my web-site … pussy888 android

Jones mocks Adesanya in series of Tweets following Blachowicz booking Jon Jones goes on a tirade targeted at Israel Adesanya.

hey there and thank you for your information – I have definitely

picked up anything new from right here. I did however expertise some technical points using this web

site, as I experienced to reload the web site a lot of times previous to I could get it to load properly.

I had been wondering if your web host is OK? Not that I’m complaining, but

sluggish loading instances times will often affect your placement in google

and could damage your quality score if advertising and marketing

with Adwords. Well I am adding this RSS to my email and

can look out for much more of your respective exciting content.

Make sure you update this again soon.

Check out my homepage download kis918 (http://Www.Nitttrc.Edu.In)

I pay a visit evегy day spme siteѕ and websites to read artіcles, except this weblog provides quality based posts. http://hectorzlri809.trexgame.net/teguran-bebas-perihal-idn-poker-online-ceme-online-pakai-uang-asli-bermanfaat

Pretty! This has been a really wonderful post. Thank you for providing this

info.

my page … 918Kaya Online

Excellent, what a blog it is! This blog provides helpful information to

us, keep it up.

Look into my homepage; 918kaya slot (https://duaxeoto.net/)

Great information. Lucky me I ran across your site by accident (stumbleupon).

I have book marked it for later!

My web page 918kaya review

I’m not that much of a online reader to be honest but your blogs

really nice, keep it up! I’ll go ahead and bookmark your

site to come back later on. Many thanks

My web blog … mega888 online

Thanks to my father who informed me concerning this website, this weblog is really

awesome.

my homepage; mega888 ios

Hi, I desire to subscribe for this webpage to

take hottest updates, so where can i do it please

assist.

Also visit my webpage: mega888 trusted company

I every time used to read paragraph in news papers but now as I am a user

of internet thus from now I am using net for posts, thanks to web.

Also visit my page … home mega888 download

Hi there, I wish for to subscribe for this website to get newest updates, so where can i do it please assist.

My web site; game mega888 online

For the reason that the admin of this web page

is working, no hesitation very rapidly it will be famous, due to its

feature contents.

Feel free to visit my page xe88 apk [Sheila]

Very good blog! Do you have any tips for aspiring writers?

I’m hoping to start my own blog soon but I’m a little lost on everything.

Would you suggest starting with a free platform like WordPress or go for a paid option?

There are so many options out there that I’m completely confused ..

Any ideas? Bless you!

Also visit my web site: id mega888

Write more, thats all I have to say. Literally, it seems as though you relied on the

video to make your point. You definitely know what youre talking about, why throw

away your intelligence on just posting videos to your weblog when you could be giving us something enlightening to read?

Also visit my site 918Kaya Online

What i don’t realize is in fact how you’re no longer really much more smartly-preferred than you might be right now.

You are so intelligent. You recognize thus significantly relating to this matter, produced me in my view imagine it from a lot of varied angles.

Its like women and men are not interested until it is something to accomplish

with Girl gaga! Your individual stuffs nice. All

the time handle it up!

Also visit my webpage – xe88 online (agile.kiwi)

excellent points altogether, you simply won a brand new reader.

What could you recommend about your submit that you just made some

days in the past? Any certain?

Also visit my blog :: Xe888

Hey there, You’ve done a fantastic job. I will certainly

digg it and personally suggest to my friends.

I’m sure they’ll be benefited from this web site.

my homepage :: mega888 download android

Just wish to say your article is as astounding. The clearness in your

post is simply excellent and that i can suppose you are an expert on this subject.

Fine with your permission let me to grab your RSS feed to stay up

to date with drawing close post. Thank you one million and please carry on the rewarding work.

Here is my blog – Mega888 ios

Wohh exactly what I was looking for, regards for posting.

My web blog :: UltraKeto Advanced (http://pansionat.com.ru/modules.php?name=Your_Account&op=userinfo&username=HoseaRanki)

I in addition to my buddies came reading through the nice

helpful tips from the website while all of the sudden I had a terrible feeling I

never thanked you for those strategies. Most of the ladies came consequently very interested to study them and

now have in actuality been taking advantage of those things.

We appreciate you really being quite kind and then for settling

on this kind of superior issues most people are really eager

to be aware of. My personal honest apologies for not expressing

gratitude to sooner.

Feel free to visit my homepage; Regen Keto Diet

Hi there! Do you know if they make any plugins to protect against hackers?

I’m kinda paranoid about losing everything I’ve worked hard on. Any suggestions?

Feel free to visit my blog post: mega888

Thanks to my father who informed me about this

website, this weblog is really amazing.

Review my page; mega888 original (Eartha)

This is a topic which is close to my heart… Take care! Exactly where are your contact details though?

my website free download game mega888

Pretty nice post. I just stumbled upon your blog and wished to say

that I have truly enjoyed browsing your blog posts. After all I will be subscribing to your rss feed and I hope you write

again soon!

Review my page xe88 online

First of all I would like to say awesome blog! I had a quick question in which I’d like to ask if you don’t mind.

I was curious to know how you center yourself and clear your

head prior to writing. I’ve had difficulty clearing my thoughts in getting my thoughts out.

I truly do enjoy writing but it just seems like the first 10 to 15 minutes are generally lost simply just trying to figure out how to begin. Any

recommendations or tips? Kudos!

Also visit my page: mega888apk download – autonym.de –

Can you tell us more about this? I’d care to find out more details.

Also visit my homepage hengheng2 xe88

Hey! Would you mind if I share your blog with my facebook group?

There’s a lot of folks that I think would really enjoy your content.

Please let me know. Cheers

Take a look at my web site xe88 online (covid311wiki.info)

Hello, every time i used to check website posts here early in the break of day, for the reason that i love to find

out more and more.

My site :: https://forum.muravev.blog/index.php?action=profile;u=155765

Hi there! I just wanted to ask if you ever have any problems

with hackers? My last blog (wordpress) was hacked and

I ended up losing many months of hard work due to no backup.

Do you have any methods to prevent hackers?

Feel free to visit my webpage :: xe888 game

I constantly emailed this website post page to all my associates, for the reason that if like to read it

after that my friends will too.

Feel free to surf to my webpage – mega888apk (http://Www.sekasao.go.th/sekaforum/viewtopic.Php?id=1732538)

No matter if some one searches for his required thing, therefore he/she desires to be available that

in detail, thus that thing is maintained over here.

Visit my website: www mega888apk

Howdy very nice blog!! Man .. Excellent .. Wonderful ..

I will bookmark your website and take the feeds additionally?

I’m happy to find a lot of useful info right here in the post, we’d like work out extra techniques on this regard,

thank you for sharing. . . . . .

Also visit my web-site – game ex88

We wish to thank you again for the wonderful ideas you gave Jesse when preparing her post-graduate research and also,

most importantly, with regard to providing many of the ideas within a blog post.

Provided that we had known of your web site a year ago, we may have been saved the pointless measures we were implementing.

Thanks to you.

Look into my web blog: kkfence.kr

This article is in fact a pleasant one it assists

new web people, who are wishing in favor of blogging.

Also visit my page xe888 online

hi!,I like your writing so much! proportion we keep up a

correspondence more approximately your article

on AOL? I need a specialist in this area to unravel my problem.

Maybe that’s you! Looking ahead to look you.

Look into my web blog: xe888apk

Hello friends, how is everything, and what you desire

to say on the topic of this post, in my view its genuinely amazing in support of

me.

my web page :: mega888apk

Hello, i think that i saw you visited my weblog so i came to “return the favor”.I’m attempting

to find things to improve my website!I suppose its ok

to use a few of your ideas!!

Review my blog post :: mega888 [Kebe.top]

Hello! Do you use Twitter? I’d like to follow you if that would be ok.

I’m absolutely enjoying your blog and look forward to new updates.

Also visit my web site :: home mega888 download

Great article! This is the type of information that should be shared across the net.

Disgrace on the seek engines for now not positioning this post higher!

Come on over and seek advice from my site . Thank you =)

My blog; 918kaya install

Heya i am for the first time here. I came across this board and I find It really useful & it helped me out a lot.

I hope to give something back and aid others like you helped me.

Here is my homepage; 918kaya online login

Hello! This is my first visit to your blog! We are a group of volunteers and starting a new initiative in a community in the same niche.

Your blog provided us useful information to work

on. You have done a outstanding job!

Feel free to surf to my site :: kiss918 free download

Thanks on your marvelous posting! I really enjoyed reading it, you’re a great author.

I will be sure to bookmark your blog and may come back in the foreseeable future.

I want to encourage that you continue your great work,

have a nice holiday weekend!

Also visit my web blog :: 918kaya test game

Quality articles or reviews is the main to be a focus for the visitors to pay a visit

the website, that’s what this site is providing.

my homepage – pussy888 2020

It’s a shame you don’t have a donate button! I’d without a doubt donate to this outstanding blog!

I guess for now i’ll settle for book-marking and adding your RSS feed

to my Google account. I look forward to new updates

and will talk about this blog with my Facebook group.

Chat soon!

Also visit my page … Download Mega888

Do you have a spam issue on this blog; I also am a blogger, and I was wanting to

know your situation; many of us have developed some nice methods and we are looking to swap techniques with other folks,

please shoot me an e-mail if interested.

Check out my blog post: pussy888 download

I blog quite often and I truly appreciate your content.

The article has really peaked my interest. I’m going to take a note of your site and keep checking for new details about once

per week. I subscribed to your Feed too.

My web page :: mega888 download android

Hello my loved one! I wish to say that this post is awesome, great written and include approximately all important

infos. I would like to look extra posts like this .

Here is my blog: mega888 malaysia

I don’t even understand how I finished up here,

but I thought this submit was once good. I do not

realize who you might be however definitely you are going to a famous blogger if you happen to are not

already. Cheers!

my blog post; pussy888 apk (autonym.de)

Thanks for sharing your thoughts on xe88 singapore.

Regards

Here is my blog post :: xe888 apk

Very good write-up. I absolutely love this site.

Keep it up!

Feel free to surf to my web site ex88 game

Yay google is my queen aided me to find this outstanding website!

my web blog; https://kebe.top

We’re a bunch of volunteers and starting a new scheme

in our community. Your site provided us with valuable info

to work on. You’ve done an impressive job and our entire group might be thankful to you.

My blog :: download mega888

Does your blog have a contact page? I’m having trouble locating it but, I’d like to

send you an email. I’ve got some creative ideas for your blog you might be interested in hearing.

Either way, great website and I look forward to seeing

it expand over time.

Look at my blog: Vale Skin Cream Reviews – forum.yawfle.com –

I absolutely love your blog and find almost all of your post’s to be just what I’m looking

for. Would you offer guest writers to write content for you personally?

I wouldn’t mind producing a post or elaborating on many of the subjects

you write concerning here. Again, awesome web log!

I’ve learn a few good stuff here. Definitely worth bookmarking for

revisiting. I surprise how much attempt you set to create any such excellent informative website.

My web-site … mega888 company

An intriguing discussion is definitely worth comment.

I do think that you ought to write more on this subject matter, it may not be a taboo

matter but typically people don’t speak about such subjects.

To the next! All the best!!

Take a look at my web page – mega888 (http://www.44706648-90-20190827182230.webstarterz.com/viewtopic.php?id=136724)

Have you ever thought about including a little bit more than just your

articles? I mean, what you say is fundamental and everything.

However imagine if you added some great photos

or videos to give your posts more, “pop”! Your

content is excellent but with images and videos, this

blog could undeniably be one of the most beneficial in its niche.

Terrific blog!

Also visit my site :: xe88 windows

Hey there! This is my 1st comment here so I just wanted to

give a quick shout out and tell you I really enjoy reading

through your articles. Can you suggest any other blogs/websites/forums that cover the same topics?

Many thanks!

Here is my page – mega888apk – Lillian,

It’s nearly impossible to find experienced people in this particular topic, however,

you seem like you know what you’re talking about! Thanks

Here is my web page Mega888Apk Download

If some one wishes to be updated with latest technologies after

that he must be go to see this web page and be up to date everyday.

Take a look at my web page … game online mega888

This info is invaluable. When can I find out more?

Feel free to visit my web site pussy888 pc

Hi, yeah this article is genuinely good and I have learned lot of things from it on the topic of blogging.

thanks.

my web blog – xe88; Betsy,

Hey there! Would you mind if I share your blog with my myspace group?

There’s a lot of folks that I think would really enjoy your content.

Please let me know. Many thanks

My website: xe88 online (develop.wiki.decimalchain.com)

Quality content is the secret to invite the visitors to go to see the

website, that’s what this web site is providing.

Review my website mega888 online (wiki.darkcoin.eu)

I was recommended this web site by my cousin. I’m not sure whether this post is written by him as nobody else know

such detailed about my problem. You’re incredible! Thanks!

Feel free to surf to my web site :: mega888 download (https://wiki.arp.gg/wiki/index.php?title=Ways_To_Acquire_Your_Own_Free_I-phone_Or_IPad_To_Down_Load_Mega888)

Awesome! Its actually awesome article, I have got much clear idea on the topic of from this piece of writing.

my page; game mega888 download

An outstanding share! I’ve just forwarded this onto a colleague who had been doing a little homework

on this. And he in fact bought me breakfast because I stumbled upon it for

him… lol. So let me reword this…. Thank YOU for the

meal!! But yeah, thanx for spending the time to talk about

this subject here on your internet site.

My webpage … scr918 (https://indiwiki.udata.id/mediawiki/index.php?title=User:LadonnaBurk267)

Pretty nice post. I just stumbled upon your blog and wished to say

that I have truly enjoyed surfing around your blog posts.

In any case I’ll be subscribing to your rss feed

and I hope you write again soon!

Visit my site download 918kiss (http://www.profoundbond.net)

It’s in point of fact a great and helpful piece of information. I am happy that you just shared this useful information with us.

Please keep us up to date like this. Thanks for sharing.

my webpage – mega888 company

Pretty great post. I simply stumbled upon your blog and wished to say that

I have truly enjoyed browsing your blog posts.

After all I will be subscribing in your rss feed and

I hope you write again soon!

Look into my web-site – 918kiss bonus

I’m truly enjoying the design and layout of your site.

It’s a very easy on the eyes which makes it much more pleasant for me to come here and visit more often. Did you

hire out a developer to create your theme? Superb work!

Also visit my homepage … agen mega888

great put up, very informative. I’m wondering why the other specialists of

this sector do not realize this. You should continue your writing.

I am confident, you’ve a great readers’ base already!

Here is my web-site: AlphaGorge XL, kebe.top,

With havin so much content and articles do you ever

run into any problems of plagorism or copyright infringement?

My blog has a lot of unique content I’ve either authored myself or outsourced but it seems a lot of it is popping it up all over

the web without my authorization. Do you know any techniques to help reduce content from being ripped off?

I’d certainly appreciate it.

Feel free to surf to my website :: 918kaya logo

Hey, I think your blog might be having browser compatibility issues.

When I look at your website in Opera, it looks fine but when opening in Internet

Explorer, it has some overlapping. I just wanted to give you a

quick heads up! Other then that, very good blog!

Here is my web blog: 918kaya agent (nightingaleffxiv.org)

Great article.

My website Download Mega88

You need to be a part of a contest for one of the best websites on the web.

I’m going to highly recommend this website!

my web site – xe888 game (http://nsato.org/cgi-def/admin/C-100/icon/yybbs.cgi?list=thread)

I’d like to find out more? I’d want to find out some additional information.

My webpage mega888 download (Foster)

We’re a bunch of volunteers and starting a brand new scheme in our community.

Your site offered us with useful information to work on. You’ve done a formidable process

and our entire community can be thankful to you.

My website – Xe888 apk

Hello there! I could have sworn I’ve been to your blog before but after going through many of the posts I realized it’s new to me.

Anyhow, I’m certainly pleased I discovered it and I’ll

be bookmarking it and checking back regularly!

My homepage … download kis918 – blakeottinger.com,

It is truly a nice and helpful piece of information. I am satisfied that you simply shared this useful information with

us. Please stay us informed like this. Thank you for sharing.

Check out my website – Free download game mega888

Attractive section of content. I simply stumbled upon your blog and in accession capital to say that I get in fact enjoyed account your blog posts.

Anyway I’ll be subscribing in your augment or even I fulfillment you get right of entry to consistently rapidly.

My web-site – download mega888 ios

Awesome article.

My blog post – 918kiss Bonus

Howdy! This is kind of off topic but I need some help from

an established blog. Is it difficult to set up your own blog?

I’m not very techincal but I can figure things out pretty fast.

I’m thinking about making my own but I’m not sure where to begin. Do you have any ideas or suggestions?

Thank you

my website – EreXegen Review; allevarecaniforum.pcwebmanager.com,

Hello there! This is my first comment here so I just wanted to

give a quick shout out and say I truly enjoy reading through

your posts. Can you suggest any other blogs/websites/forums that

cover the same subjects? Thanks for your time!

My web-site: 918kiss 1

Have you ever considered writing an ebook or guest authoring on other sites?

I have a blog based on the same information you discuss and would love to have

you share some stories/information. I know my viewers would

appreciate your work. If you’re even remotely interested, feel free

to shoot me an email.

Stop by my web blog – cara main game xe88

Thank you for another informative site. The place else could I

get that type of information written in such an ideal way?

I’ve a mission that I am simply now running on,

and I have been at the glance out for such information.

I was just searching for this info for some time.

After 6 hours of continuous Googleing, finally I got it in your web site.

I wonder what is the lack of Google strategy that do not rank this

kind of informative websites in top of the list.

Generally the top websites are full of garbage.

Feel free to visit my website; mercedesturkey.com

It’s an amazing piece of writing designed for all the web users;

they will get advantage from it I am sure.

my webpage … xe88 (https://kebe.top/viewtopic.php?id=350279)

I pay a visit daily some blogs and blogs to read content, but this

web site presents feature based writing.

my site: xe88 game apk

You will also uncover out how to calculate the odds ratio working

with the odds equation.

Excellent web site you have here.. It’s hard to find high quality

writing like yours nowadays. I really appreciate people like you!

Take care!!

Feel free to surf to my page; cara masuk id test mega888

Hey there would you mind letting me know which webhost you’re

using? I’ve loaded your blog in 3 completely different web

browsers and I must say this blog loads a lot faster then most.

Can you recommend a good hosting provider at a fair price?

Thank you, I appreciate it!

Also visit my web blog :: Regen Keto Review (http://www.edgeclothing.com)

Informative article, exactly what I wanted to find.

My blog; 918Kaya Kiss

Highly descriptive article, I enjoyed that a lot. Will there

be a part 2?

Also visit my website – 918kaya game

It’s very trouble-free to find out any matter on net

as compared to textbooks, as I found this piece of writing at this website.

Also visit my web site :: Scr Mega888

Hey very cool web site!! Guy .. Beautiful .. Amazing ..

I will bookmark your blog and take the feeds also?

I am glad to find a lot of helpful information here in the publish, we need work out extra techniques in this regard,

thanks for sharing. . . . . .

my blog post; kiss 918kaya apk

Hmm it appears like your site ate my first comment (it was super long) so

I guess I’ll just sum it up what I wrote and say, I’m thoroughly enjoying your blog.

I too am an aspiring blog writer but I’m still new to everything.

Do you have any suggestions for rookie blog writers?

I’d certainly appreciate it.

Also visit my website :: 918kaya

I’ll right away grab your rss feed as I can not to find your e-mail subscription hyperlink or newsletter service.

Do you’ve any? Please permit me realize so that I may subscribe.

Thanks.

Here is my web page – xe88 download, Dustin,

I am sure this paragraph has touched all the internet visitors, its really

really nice post on building up new web site.

Feel free to visit my web-site :: slot pussy 888

The other day, while I was at work, my sister stole my iPad and tested to see if it can survive a

twenty five foot drop, just so she can be a youtube sensation. My apple ipad is now broken and she has 83 views.

I know this is totally off topic but I had to

share it with someone!

Here is my page; mega888 singapore (http://nightingaleffxiv.org/)

I have been browsing online greater than three hours today, but I never found any interesting article like yours.

It is lovely price sufficient for me. In my opinion, if all

site owners and bloggers made good content as you probably did,

the internet will likely be a lot more helpful than ever before.

Feel free to visit my site :: pusyy888

What i do not realize is if truth be told how you’re no longer actually much

more smartly-appreciated than you may be now. You’re very intelligent.

You already know therefore significantly in relation to this topic, produced me

in my view believe it from so many varied angles. Its like men and

women are not involved until it is something to accomplish with Girl

gaga! Your own stuffs excellent. At all times care for it up!

Here is my site; pusyy888

wonderful post, very informative. I ponder why the opposite specialists of this

sector don’t notice this. You must proceed your writing.

I’m sure, you have a great readers’ base already!

Here is my web-site 918kaya download for android

Have you ever thought about including a little bit more than just your articles?

I mean, what you say is valuable and all. Nevertheless just

imagine if you added some great images or video clips to give your posts more, “pop”!

Your content is excellent but with images and

clips, this site could certainly be one of the best in its field.

Superb blog!

My blog post 918kaya (Wiki.cordoba.gob.ar)

Very quickly this site will be famous amid all blogging and site-building people,

due to it’s fastidious articles

Here is my blog post … kiss916 free download

My programmer is trying to persuade me to move to .net from PHP.

I have always disliked the idea because of the expenses.

But he’s tryiong none the less. I’ve been using Movable-type on numerous websites

for about a year and am concerned about switching to

another platform. I have heard excellent things about blogengine.net.

Is there a way I can import all my wordpress

posts into it? Any help would be really appreciated!

Look into my web blog … download game 918kaya apk

This excellent website certainly has all the information and facts I wanted about this subject and didn’t know who

to ask.

Also visit my website: scr918kiss

Right here is the perfect blog for everyone who wants to

understand this topic. You know so much its almost hard to

argue with you (not that I actually would want

to?HaHa). You definitely put a fresh spin on a subject that has been written about for decades.

Wonderful stuff, just wonderful!

Feel free to visit my webpage … eliminate yeast infection

This is my first time pay a quick visit at here and i am actually pleassant

to read all at single place.

Also visit my web page: Mega888Apk

When I initially left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and from now on every time a comment is

added I recieve 4 emails with the exact same comment.

There has to be an easy method you are able to remove me from that service?

Thank you!

Feel free to surf to my blog :: nerverlearn.com

Saya akan segera rebut rss Anda karena saya tidak bisa

Saya yakin tulisan ini telah menyentuh semua pengunjung internet, benar-benar rewel

pos tentang membangun web site baru.

Here is my page :: Slot joker123 bonus New member (gameaco.com)

You are a very capable person!

Visit my blog; sex technique

Keep this going please, great job!

Feel free to visit my page – 79.96.178.225

I think this is one of the most vital information for me.

And i’m glad reading your article. But wanna remark on some general

things, The site style is perfect, the articles is really nice : D.

Good job, cheers

Also visit my page: Xe88 game list

I simply couldn’t depart your site prior to

suggesting that I really enjoyed the standard information a person supply in your

guests? Is going to be again continuously to check up on new posts

Feel free to visit my site – 918kaya online

What’s up to every one, since I am really eager of reading this webpage’s post to be updated on a regular basis.

It consists of fastidious data.

Here is my homepage mega888 website

you’re actually a excellent webmaster. The website loading

velocity is incredible. It seems that you are doing any distinctive

trick. Also, The contents are masterwork.

you have done a fantastic activity on this subject!

Have a look at my page :: mega888apk download

My family members all the time say that I am

wasting my time here at web, but I know I am

getting familiarity every day by reading thes fastidious articles or reviews.

Here is my blog post: mega888 download – http://24friends.co.kr,

Hello there, I do think your website might be having

internet browser compatibility problems. When I look at your web site in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping issues.

I simply wanted to provide you with a quick heads up!

Other than that, wonderful site!

Here is my blog post … bussy888

Howdy would you mind stating which blog platform you’re using?

I’m looking to start my own blog soon but I’m having a tough time selecting

between BlogEngine/Wordpress/B2evolution and Drupal.

The reason I ask is because your design and style seems different then most blogs and I’m looking for something completely unique.

P.S My apologies for being off-topic but I had to ask!

Feel free to surf to my homepage … Xe88Hack

I’m really loving the theme/design of your

weblog. Do you ever run into any web browser compatibility issues?

A handful of my blog visitors have complained about

my website not working correctly in Explorer but

looks great in Opera. Do you have any advice to help fix this problem?

Check out my homepage :: returnorbit.net

Hey very interesting blog!

Review my web-site; kiss918 scr

I have been surfing on-line greater than 3 hours today, but

I never discovered any interesting article like yours.

It is beautiful value sufficient for me. Personally, if

all web owners and bloggers made excellent content material as you probably did, the

net will be much more helpful than ever before.

my web blog :: popaholics.net

Nice weblog here! Also your website loads up fast!

What web host are you using? Can I get your affiliate hyperlink on your host?

I want my website loaded up as quickly as yours lol.

Also visit my web-site: 79.96.178.225

Every weekend i used to pay a quick visit this web page, for

the reason that i want enjoyment, for the reason that this

this site conations genuinely fastidious funny

data too.

Also visit my blog Alpha Gorge XL, Adelaide,

Good blog! I really love how it is easy on my eyes and the data are well written. I’m wondering how I could be notified when a new post has been made.

I’ve subscribed to your RSS feed which must do the trick!

Have a nice day!

my website PrimaFreshia Keto Reviews (freeholmes.com)

Thanks for a marvelous posting! I seriously enjoyed reading it,

you happen to be a great author.I will be sure to bookmark your blog and will come back someday.

I want to encourage you to definitely continue your great job, have

a nice day!

Feel free to surf to my web blog … mega888apk

What i do not understood is actually how you’re no longer actually

much more well-appreciated than you may be right now.

You’re so intelligent. You already know thus significantly relating

to this topic, produced me for my part imagine it from numerous various angles.

Its like men and women aren’t fascinated until it’s one thing to do with

Woman gaga! Your personal stuffs nice. Always maintain it up!

my webpage; xe88app

I’m not that much of a internet reader to be honest but your sites

really nice, keep it up! I’ll go ahead and bookmark your site to come back later on. Cheers

my web-site: downloadxe88

Wow, awesome weblog format! How long have you ever been running a blog for?

you made blogging glance easy. The overall glance of your web site

is excellent, as smartly as the content!

Here is my blog post ex88 apk

Nice post. I was checking continuously this blog and I am impressed!

Extremely helpful info particularly the last part 🙂 I care for such info much.

I was looking for this certain information for a very long time.

Thank you and best of luck.

Here is my page 918kaya apk

You have made some really good points there. I looked on the internet for more info about the issue and found most people will go along with your views on this site.

Feel free to surf to my site: pussy888 dow

bookmarked!!, I like your site!

my homepage … pussy888 apk download [https://wiki.darkcoin.eu/index.php?title=Are_You_Embarrassed_By_Your_Pussy888_Download_Skills_Here%C3%82%C3%A2%E2%82%AC%E2%84%A2s_What_To_Do]

I visited many blogs but the audio quality for audio songs present at this

website is actually superb.

Review my blog; mega888

Hey there! This post couldn’t be written any

better! Reading this post reminds me of my old room mate! He always kept chatting about this.

I will forward this page to him. Fairly certain he will have a

good read. Many thanks for sharing!

Feel free to surf to my page … mega888 [Philipp]

Hello There. I found your weblog using msn. That is a very well written article.

I will be sure to bookmark it and come back to learn extra of your

useful information. Thank you for the post. I’ll certainly comeback.

Feel free to surf to my web-site :: xe88 online

What i do not realize is if truth be told how you are no longer actually

a lot more well-appreciated than you may be right now.

You’re very intelligent. You already know thus considerably in the case of this

subject, made me in my view believe it from so many various angles.

Its like men and women don’t seem to be interested except it is something to do

with Girl gaga! Your personal stuffs excellent.

Always handle it up!

Here is my webpage :: pussy888Apk

What’s up to every single one, it’s really a pleasant for me to

pay a quick visit this website, it contains helpful

Information.

My site :: Keto Fast Burn Review

I always was interested in this topic and still

am, regards for posting.

Here is my web-site; Rhino Max Reviews

Thank you for sharing excellent informations. Your web-site is very cool.

I am impressed by the details that you have on this website.

It reveals how nicely you perceive this subject.

Bookmarked this website page, will come back for extra articles.

You, my friend, ROCK! I found simply the info I already

searched everywhere and just couldn’t come across. What a great web-site.

Feel free to visit my web page – http://www.haksizlik.com

Just desire to say your article is as surprising.

The clearness in your post is just excellent and i can assume you’re an expert on this subject.

Well with your permission let me to grab your RSS

feed to keep updated with forthcoming post.

Thanks a million and please carry on the enjoyable

work.

my web-site: mega888 11

Hey! Someone in my Myspace group shared this website with us so I came to take a look.

I’m definitely enjoying the information. I’m bookmarking and will be tweeting this to

my followers! Wonderful blog and excellent style and design.

Also visit my website :: download mega888

I’m amazed, I must say. Seldom do I come across a blog that’s both equally educative and interesting, and let me tell

you, you have hit the nail on the head. The issue is something that too few folks

are speaking intelligently about. I’m very happy I came across this in my hunt for something concerning this.

Have a look at my website – mega888 download pc

Nice blog here! Also your website loads up very fast!

What host are you using? Can I get your affiliate link to your host?

I wish my web site loaded up as fast as yours lol

my blog; mega888 download (http://mediawiki.hslsoft.com/)

It is not my first time to visit this site, i am visiting this web site dailly

and obtain nice data from here daily.

My webpage – http://www.p2plists.info

I feel that is among the such a lot significant information for me.

And i am happy reading your article. However want to statement on some normal things, The web site taste is great, the articles is really great : D.

Excellent task, cheers

Feel free to surf to my page: xe88 slot

I just could not leave your web site prior to suggesting that I actually loved the usual information an individual

supply to your guests? Is going to be again ceaselessly in order to

investigate cross-check new posts

Also visit my web blog … mega88 download

Hello there! Do you use Twitter? I’d like to follow you if

that would be okay. I’m definitely enjoying your blog and look forward to new posts.

My web site: download mega888, http://www.sekasao.go.th,

Having read this I believed it was extremely informative.

I appreciate you taking the time and energy to

put this information together. I once again find myself spending way too much time

both reading and commenting. But so what, it was still worth it!

Also visit my site … download mega888 for android

Why people still make use of to read news papers when in this

technological globe all is accessible on web?

Here is my webpage; xe88 online

This is the perfect site for anybody who wishes to find out about this topic.

You understand so much its almost hard to argue with you

(not that I really will need to…HaHa). You certainly put a fresh spin on a topic that has been discussed for ages.

Excellent stuff, just wonderful!

Look into my blog: Body Accord Keto Ketogenic Formula, https://www.bashklip.ru,

First off I would like to say superb blog! I had a quick question which

I’d like to ask if you don’t mind. I was curious to know how you center yourself and clear your thoughts before writing.

I’ve had difficulty clearing my thoughts in getting my thoughts out.

I do enjoy writing but it just seems like the first

10 to 15 minutes are lost simply just trying to figure out how to begin. Any ideas or tips?

Appreciate it!

Feel free to visit my page; 918kaya link