It is safe to say the resilient U.S. consumer has kept the economy from flirting with recession. And again in June, consumer spending increased by 0.5 percent over May, and again, up faster than disposable income. During and shortly after the pandemic, consumers splurged on a range of discretionary items — home gym equipment, patio furniture and then travel and concerts. The level of overall spending has not decreased but rather shifted to discount retailers, in a sign, along with a rapid increase in credit card delinquencies, that savings may soon be depleted, some say.

Last Friday at the annual Jackson Hole symposium, Fed chair Jerome Powell, surveying this and other economic data points, said the Fed was in a position to “proceed carefully” on interest rates, which ordinarily bear directly on consumer appetites, especially for big-ticket items. A move from discretionary to discount spending might be a harbinger of a trend that could give the Fed pause before resuming rate increases that have not phased consumer spending, just yet. More on the role and state of the consumer in our economy below.

Best,

Dana

————————————————————————————————————————————————————

Consumers Bearing the Brunt Well

Consumer activity makes up the lion’s share of the American economy, true in good times and bad. This century, consumption as a share of the economy has only fluctuated by about two percent, between 66 and 68 percent. American consumption is such a powerful force that in 2022 it made up more than 10 percent of the global economy, which still understates the importance of the American consumer. Despite being battered by inflation, higher interest rates, and voracious corporate appetites, robust consumer spending has been able to keep the American economy out of a recession.

Still, things seem to be changing. In recent months, luxury brands like LVMH have reported slower American sales, but Walmart has raised expectations massively, suggesting that the price pressure has gotten to be too much for the American consumer, now cutting back on luxuries. Similarly, consumers spent more at companies like TJ Maxx and HomeGoods while more upmarket companies like Target saw their earnings decline. This spending trend is consistent with the fact that lower-income workers have seen their inflation-adjusted earnings increase, while higher-income workers have not. It could also be another sign of a “richcession,” which, while directly affecting fewer Americans, could have dangerous ripple effects.

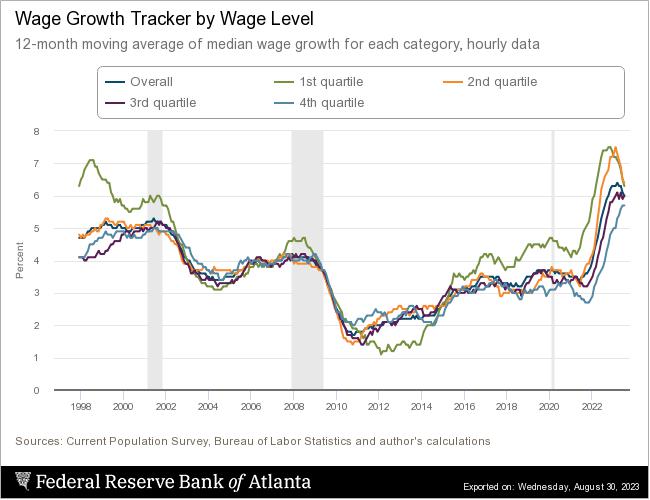

Counter to the trend in the years after the Great Recession, Wage Growth has been faster for workers in the lower two quartiles of income than for those in the top half

Still, consumers have been increasing their spending faster than wages have been going up. With inflation expectations, this makes sense. If consumers are afraid that prices will continue to increase, they would rather buy things today than wait for them to be more expensive tomorrow.

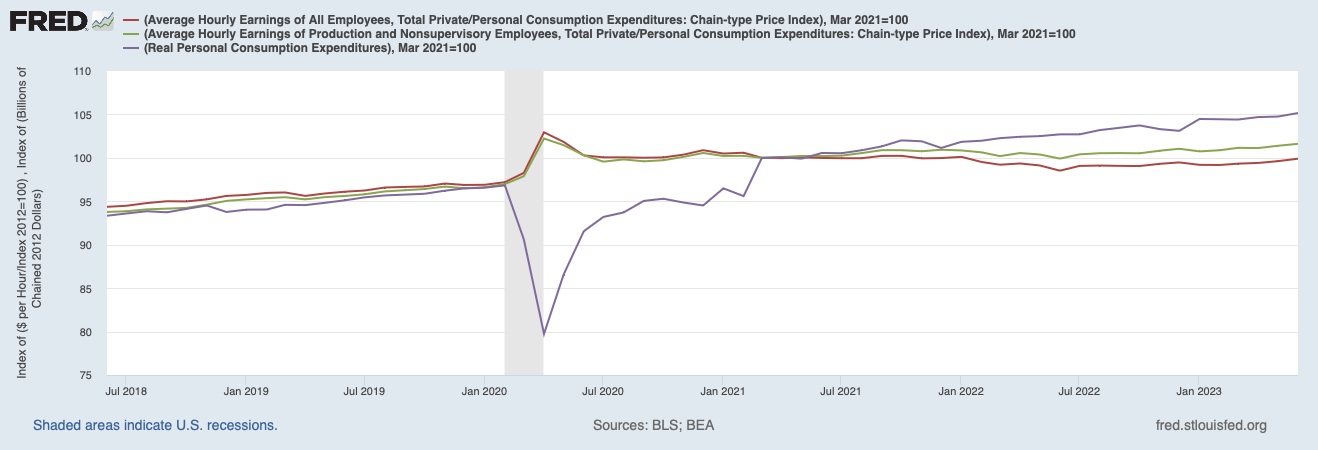

Despite the growth of some Americans’ wages, inflation-adjusted consumption spending has increased even faster

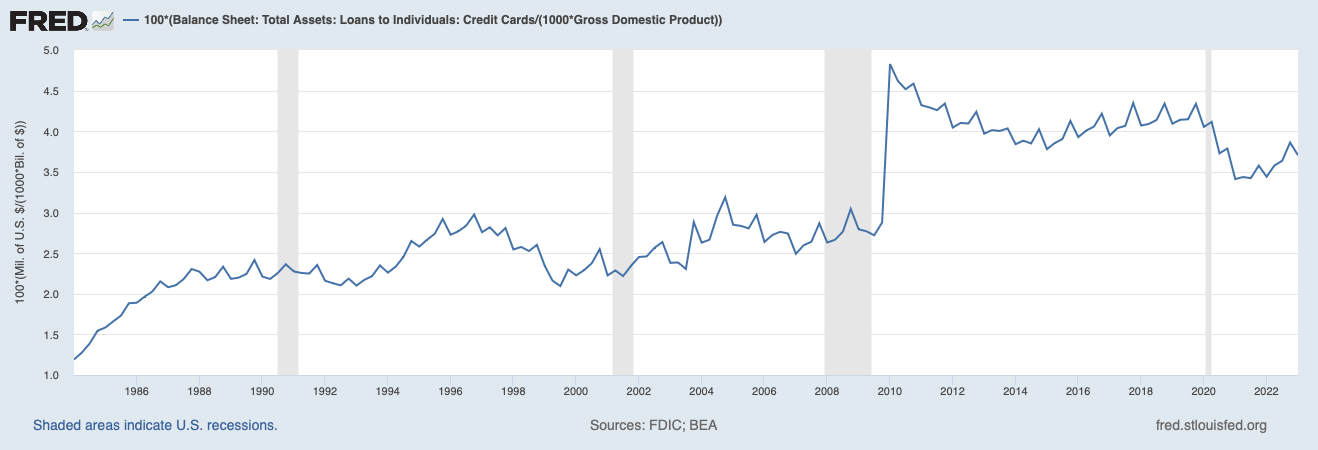

The persistent mismatch between consumption and wages could explain the increase in credit card debt, which recently reached $1 trillion for the first time ever. While the New York Fed characterizes this increase as a return to the pre-pandemic normal, it is another squeeze on the stronger balance sheets that existed after the pandemic. There is some debate over the persistence of this surplus, with the most dour forecasts showing it running out by the end of this quarter, and more hopeful ones showing that for the top two-thirds of the income spectrum, a plentiful pile of extra cash.

After it plummeted during the pandemic, Inflation and high consumption are driving American’s credit card borrowing back up

The American Consumer: Powerful but Beset

Last week, we sent out an update on the status of merger and competition policy. We noted how lax antitrust enforcement has led to an increase in corporate power relative to consumers. This has been apparent in efforts to block consumer repairs shortening the lifespan of goods they purchase, and mergers that increase profits while exacerbating food deserts. This expansion of corporate power has given consumers fewer choices and less power over the things they do end up buying. Adding to consumer’s stress is the unaffordability of housing we talked about two weeks ago. Since we wrote about it, mortgage rates have increased and prices have gone up.

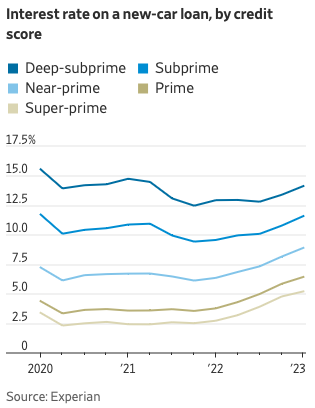

To see how things have changed, it makes sense to look at the automotive market. While most of the coverage of that market has had to do with the demise of new cars costing less than $20,000, we noticed another interesting data point. Looking at the changes in interest rates charged on new-car loans, they have not changed evenly, or even in the same direction across credit categories since the second quarter of 2020. According to Experian, deep-subprime (credit scores below 580) and subprime borrowers (580-619) have seen the interest rates they are charged barely change, prime borrowers (660-719) have seen their interest rates nearly double, while the super-prime (above 720) have seen their rates more than double.

For households with strong credit, car loans have gotten much more expensive, while for their low-credit peers have seen very little change

Compounding this disruption, many companies have raised prices during the current inflationary episode. While the idea of an increase in corporate greed relies strongly upon faulty intuition (after all, when have corporations not been greedy?) The ways in which companies have raised prices have been increasingly, arguably, stressful to consumers. With strong evidence that consumers make buying decisions based on sticker prices, the practice of increasing prices through additional fees rather than sticker price increases adds to sticker shock, and consumer stress.

These disruptions have strained economic conditions. Creditors and people on fixed incomes are hurt, while debtors and people whose incomes are automatically indexed are relatively better off. Combining this disruption with a sharp increase in interest rates that, for the first time in more than a decade, have fundamentally changed many markets.

No wonder consumer sentiment has fallen so far. In fact, in the more than seven decades that the University of Michigan’s Survey of Consumers has been going, the index of consumer sentiment it creates has never been lower than it was in June 2022. After a few months of sharp rises, last week’s release of consumer sentiment moved sideways. At a level of 69.5, it currently reads as closer to the end of the Great Recession, 70.8 in June 2009, than it does to the reading of 84.9 in March 2021, the last time inflation was this low.

What is to Follow for Consumers?

The next few months do not hold that much hope of relief for consumers. Inflation persists and will. The restart of student loan payments will put pressure on millions of households, further draining their dwindling pandemic savings. In addition, those who have historically taken advantage of consumers, (along with their Republican allies) are trying to make a bad situation worse. Payday lenders aided by conservative judges are currently attempting to defund, if not destroy, the Consumer Financial Protection Bureau, the only government agency mandated and dedicated to offering recourse to financial consumers. It is up to those of us with platforms and power to push back as vigorously as we can against these efforts and in support of consumers.

Luckily, the administration is taking action against these threats, such as fee-induced sticker shock, and have rolled out proposals and actions to reduce these fees in key areas of economic life. When the Supreme Court overturned the President’s proposal to forgive some student debt, the administration rolled out a series of proposals to mitigate the impact of the decision. One of those proposals, the SAVE plan, the most affordable income-driven repayment plan in American history, was officially launched last week. Yesterday, the administration announced a list of ten prescription drugs that Medicare will, for the first time in its history, be able to negotiate the price with. While ten drugs seems like a drop in the bucket, these ten made up 20 percent of Medicare’s drug spending last year. Unfortunately, these cost savings will only come into effect on January 1, 2026. Still, it is vitally important to give the administration the support it needs to continue these pro-consumer policies.