The GOP House effort to elect a Speaker concluded this afternoon when Rep. Mike Johnson (R-LA) prevailed in a 220-209 party-line vote. This means that Congress can return to fiscal policy — though already about half the time available to move past the current FY24 continuing resolution that is keeping the government open until November 17 has been wasted. With a functioning House of Representatives, the first order of business will be the administration’s $156 billion in two emergency supplemental requests. Then, Congress will return to the FY24 budget, facing fiscal facts made clear by news last month that the national debt now stands at $33 trillion.

But is it within the capacity of the current Congress to adopt a bipartisan solution to the problem? The main reason this seems unlikely in our divided government is the GOP’s insistence on unbalanced solutions: cutting spending without increasing revenues. Last week’s House Budget Committee hearing on creating a fiscal commission to address the national debt shows why solutions look as remote as the possibility of bipartisanship does.

Details below.

Best,

Dana

As the appropriations process for FY24 has been on hold amidst the House’s three-week struggle to elect a speaker, data released this week estimated that the federal government ran an almost $2 trillion budget deficit for FY23. Interest payments grew significantly while revenues decreased, leading to consternation about the future solvency of critical social insurance trust funds. Although solutions, like the creation of a bipartisan fiscal commission, have been proposed, Congress lacks a broad consensus about the best way to address current fiscal conditions.

Trendline in Debt and Deficit: Further Growth of Both

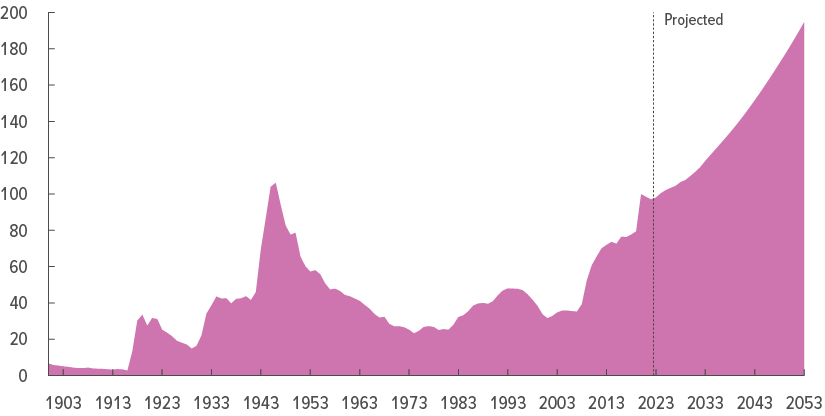

The U.S. national debt grew by $1 trillion over the final quarter of FY23 alone, driving total national debt past the $33 trillion mark last month. The $33 trillion in debt is equivalent to $99,000 per person or $252,000 per household in America. While this state of affairs is concerning, projections indicate a far more dire fiscal future. According to the Congressional Budget Office (CBO), gross federal debt is expected to exceed $50 trillion (118 percent of total GDP) by 2033 and 195 percent of GDP by 2053.

Federal Debt Held by the Public, 1900 to 2053

Percentage of Gross Domestic Product

Source: Congressional Budget Office

The growth in the national debt is due to a rapid increase in annual deficits over the past several years. This week, the U.S. Department of Treasury placed the final value of the deficit at $1.7 trillion for FY23. This marks a 23 percent growth from FY22 levels. This figure understates the situation, as the FY22 deficit was propped up by $379 billion in expenditures related to the Biden Administration’s student loan forgiveness plan last year. Since then, the Supreme Court has deemed this cancellation of student debt unconstitutional, shifting debt and deficit totals. With student debt cancellation removed from the equation, the deficits for FY22 and FY23 are roughly one and two trillion dollars respectively, a deficit growth rate of 100 percent.

Interest Payments Soar Along With Fed Rates

As the national debt has grown, so have interest rate payments required to finance it. Although the ratio of interest payments to GDP remains lower than it was during the 1990s, these payments have grown significantly in recent years. The main culprit is the Federal Reserve’s series of interest rate hikes which have lifted rates from near zero in early 2022 to 5.25-5.50 percent today, the highest level in 16 years.

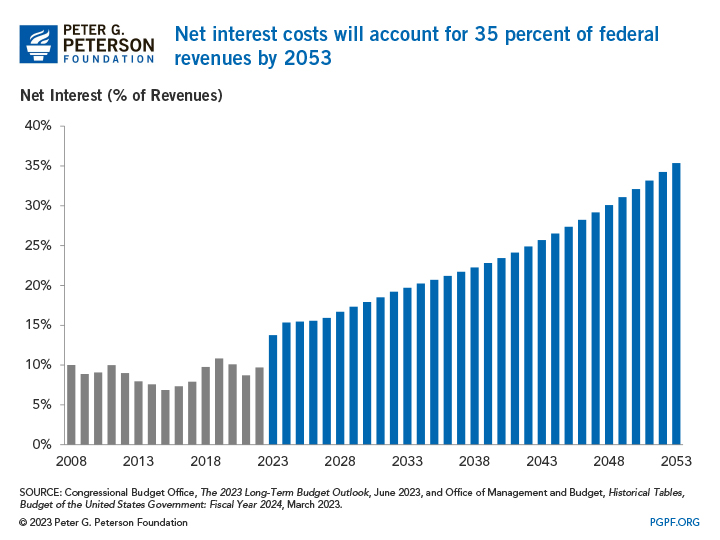

Recent figures from the Center for a Responsible Federal Budget (CRFB) show that interest on the national debt rose from $475 billion in FY22 to $659 billion in FY23, an increase of almost 40 percent. Annual interest costs are expected to increase to $1.4 trillion, equivalent to 20 percent of federal revenue, by 2033. This share would be greater than defense spending and is on its way to passing social insurance spending over the next 25 years. These projections are illustrated below:

Source: Peter G. Peterson Foundation

Interest rates are not expected to come down any time soon, according to Fed Chair Jerome Powell, which could add trillions to the national debt. If this trend continues as expected, the share of revenue from interest payments could pass that of defense spending and social insurance programs much sooner than expected.

Revenues Collapse in Fiscal Year 2023

The past year has also seen a dramatic decrease in revenue of $457 billion between FY22 and FY23. Most of this decline can be attributed to an eight percent decrease in individual income and payroll tax totals, accounting for $327 billion in lost revenue. Most likely, we are seeing the effects of provisions of the Trump-era Tax Cuts and Jobs Act (TCJA), much of which were hidden by higher-than-usual capital gains between 2017 and 2021. Although a 14 percent reduction in the corporate tax rate has not led to a notably large decrease in associated revenue, the U.S. still ranks low in corporate tax revenue compared to other OECD countries. The current tax rate for corporations is less than half the size it was in the 1950s and 60s.

The revenue picture points to a solution, or at least to a way to avoid aggravating the problem. As we look forward to the expiration of some provisions from the TCJA at the end of 2025, it will be important to prevent extensions that would further decrease tax revenue and worsen the debt crisis.

Another revenue-based solution lies in addressing the widening tax gap, a measure of tax liabilities owed versus the amount actually paid. For the 2021 fiscal year, the reported tax gap was the largest it’s ever been, $688 billion. This trend would only be made worse by recent successful GOP efforts to rescind funding for the IRS by $21 billion in funding during debt ceiling negotiations earlier this year. This and further GOP proposals to cut the $80 billion provided to assist IRS tax enforcement under the Inflation Reduction Act would reduce revenues by at least twice the amounts rescinded.

Social Insurance Trust Funds Nearing Insolvency

As the budget deficit continues to grow, urgent solutions are needed to save Social Security and Medicare benefits. Americans pay into the trust funds for these programs and have every right to expect the benefits. Social Security (old-age, survivors, and disability insurance) and Medicare spending were respectively $135 billion and $93 billion higher in FY23 than in FY22. Projections estimate that spending on these programs will increase by 1.5 percent of GDP over the next ten years.

Current estimates show that the Medicare Trust Fund will reach insolvency in the year 2031, and Social Security will shortly follow in 2033. Although “insolvency” will not come with a total loss in Social Security and Medicare benefits as the social insurance trust funds will continue to bring in revenue, a significant reduction of an expected 24 percent in the case of Social Security could prove devastating for millions of Americans precariously navigating retirement.

The fiscal condition of the social insurance trust funds puts a premium on trust fund revenues increases. For 2023, the maximum limit on earnings for withholding Social Security tax is $160,200, with a tax rate of 6.2 percent. The Medicare tax rate applies to all taxable wages and remains at 1.45 percent. The Federal Insurance Contributions Act, or FICA, tax rate, the combined Social Security rate of 6.2 percent and the Medicare rate of 1.45 percent, remains 7.65 percent for 2023 (or 8.55 percent for taxable wages paid in excess of the applicable threshold). Raising the Social Security threshold and increasing FICA taxes, perhaps even adding liability for capital gains, could go a long way to avoiding insolvency.

Promise and Perils of a Fiscal Commission

Current political circumstances evidenced by the inability of the House to function as a legislative body raise the question of appointing a bipartisan fiscal commission to consider and propose solutions to the national debt problem. Commissions have been used in the past to find solutions in times of economic uncertainty or political incapacity.

- The 2010 Simpson-Bowles Commission created policy proposals that went on to pass through Congress in later years. It also raised concern surrounding the U.S. fiscal outlook and helped lead to the Budget Control Act.

- The 1983 Greenspan Commission made recommendations that led to the 1983 Social Security Amendments, which helped stave off Social Security insolvency by 50 years.

Based on lessons from the Simpson-Bowles and Greenspan commission experiences, as well as other examples that have been used to address concerns in various policy areas, a successful bipartisan fiscal commission would need to include:

- A clear but reasonable and manageable timeline and set of goals in order to focus effort and measure success without forcing major mid-course corrections

- Enforcement mechanisms to encourage bipartisan concessions — an example of which would be the default provisions in June’s Fiscal Responsibility Act mandating across the board spending cuts or revenue increases all parties would want to avoid

- A consideration of both revenue and spending cuts that does not rely on reducing benefits that Americans have already paid for

Worth noting are the many problems with a fiscal commission, which have been outlined by the Center on Budget and Policy Priorities. Under current circumstances, a fiscal commission runs the risk of:

- being seen by the public as an abdication by elected representatives’ responsibility in favor of reposing hope in an unelected commission

- yielding to pressure to mandate a commission in a way takes revenue-based solutions off the table, such as one enabling extensions of TCJA cuts that have worked to reduce revenue

- placing too much emphasis on short-term fixes to the national debt that would invite Congress to revise or abandon long-term fiscal goals

It is an open question whether the necessary bipartisan will exists to authorize a similar commission. Democrats have adamantly opposed a fiscal commission that would consider cuts to social insurance programs, while Republicans have insisted on protecting TCJA tax cuts and defense spending. Although a commission could work in theory, non-negotiables on both sides could prevent any real progress from being made. These concerns were echoed in the hearing held by the House Budget Committee last week.

Given a House of Representatives led by a staunchly conservative conference, the better part of fiscal valor might call for action at a more politically propitious time, such as next Congress, when the House could be in Democratic hands. Now, however, it is unlikely that political conditions will allow for agreement that avoids the pitfalls of a commission and finds viable bipartisan strategies to address the growing national debt. But if interest expense or unexpected emergency spending continues to crowd out other spending, those circumstances might force a reckoning with the fiscal condition that only a commission can solve. Representative Jodey Arrington (R-TX), Chairman of the House Budget Committee, may soon choose to move beyond hearings and propose legislation.