Update 708 — Impact of Bank Mergers

On Consumers, Investors, the Economy

Major goods and services sectors across the economic landscape have come under increasing scrutiny in recent years for anti-competitive behavior, conditions restricting consumer access and choice, and raising costs. When banks merge, by and large, they will maintain fewer branches, provide fewer services, and do both at greater costs for retail customers and small businesses. Today we look at the competitive condition of the financial sector, trends, and consequences.

On Wednesday, the Economic Policy Subcommittee of Senate Banking heard from experts about bank merger policy. Circumstances following the collapse of SVB and Signature and the merger of JPM and First Republic make such a conversation timely, with far-reaching consequences for millions of American consumers and firms.

Good weekends all,

Dana

On Wednesday, the Senate Committee on Banking, Housing and Urban Affairs Subcommittee on Economic Policy convened for a hearing titled “Bank Mergers and the Economic Impacts of Consolidation.” The hearing follows recent turmoil in the nation’s banking sector and comes amidst an apparent shift by some of the administration’s economic leaders towards further consolidation in the sector. As witnesses and senators emphasized, further consolidation reinforces the underlying problem rather than presents a solution.

Decades of Consolidation

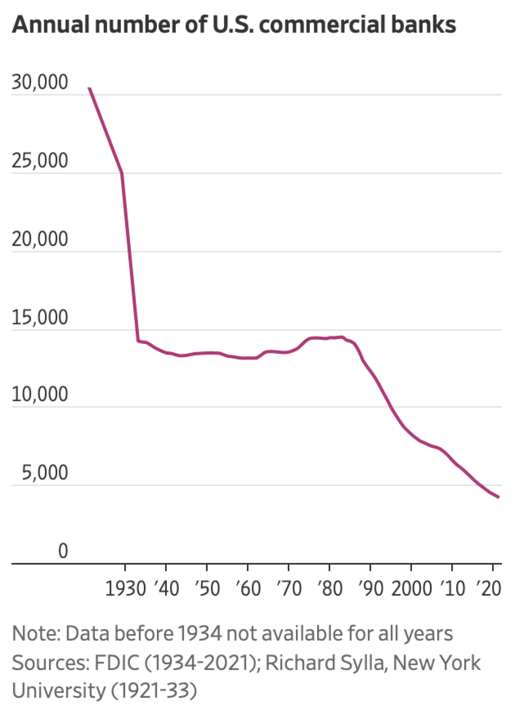

America’s banking sector was built on competition. As Subcommittee Chair Elizabeth Warren (D-MA), along with Director of Policy and Advocacy at the American Economic Liberties Project Morgan Harper and Senior Policy Analyst at Americans for Financial Reform Alexa Philo highlighted, there were 15,000 banks in the United States in 1990, but by 2022, the total number of banks chartered by the Federal Deposit Insurance Corporation had fallen to under 4,200. In 2021, three quarters of local banking markets were considered uncompetitive, having surpassed the Justice Department’s “high concentration” threshold. This wave of consolidation was driven by deregulation and a softening of merger enforcement.

Consolidation in the banking sector has led to harmful outcomes for consumers, small businesses, and communities. Community banks, geared towards “relationship banking” that understands the unique character and needs of their local communities, tailor their work to best serve their local clients. To illustrate this concept, Senator Warren described the case of a local bakery seeking to open a new branch. Despite financial struggles common to small businesses during the pandemic, a community bank is more likely to provide funding for such a venture than a larger bank whose provision of funding is geared towards larger commercial customers.

During the pandemic, community banks played a key role in helping small businesses access federal Paycheck Protection Program (PPP) loans. Community banks issued over 30 percent of all PPP loans made by banks, while the four largest American banks – JPMorgan Chase, Bank of America, Citibank, and Wells Fargo – issued just three percent of those loans combined.

As the banking sector shrank, incentives of larger institutions became geared toward larger commercial customers. Larger banks reject more mortgages, provide less funding to small businesses and charge higher so-called junk fees. Furthermore, bank consolidation often leads to branch closures in areas where predatory non-bank financial companies like payday lenders and check cashers jump in to fill the gap. The knock-on effects lead to more debt being sent to collections, and even more evictions in the community affected.

Bank mergers don’t just hurt consumers, communities and small businesses. They make already too-big-to-fail banks even bigger and too big to effectively regulate.

Concerning Comments from Economic Regulators

Following recent banking turmoil, several top Biden Administration regulators have suggested that further bank mergers may be necessary and that regulators may be more friendly to approving them. On May 13, Secretary Yellen gave an interview on the sidelines of the G7 Summit in Japan, in which she said, “This might be an environment in which we’re going to see more mergers, and you know, that’s something I think the regulators will be open to, if it occurs.” She also said, “The unfortunate dynamic is that once a bank’s stock is under pressure, it can trigger concern among uninsured depositors … even though the bank has adequate capital and liquidity.”

The next week, Yellen attended a meeting in Washington with over two dozen bank CEOs and executives, including JPMorgan Chase CEO Jamie Dimon. Reportedly, Secretary Yellen told executives that more bank mergers may be necessary.

The Secretary’s comments on bank mergers to executives of large banks came on the same day that Michael Hsu, the acting comptroller of the currency, testified before the Senate Banking Committee. Acting Comptroller Hsu discussed bank mergers in his testimony, stating that recent turmoil in the banking sector increased the urgency of the OCC’s efforts to update the analytical frameworks related to the bank merger guidelines that federal banking agencies and the DOJ must follow when considering bank mergers. Hsu also stressed that “The OCC is committed to being open-minded when considering merger proposals and to acting in a timely manner on applications, consistent with the requirements of the Bank Merger Act.” This is not the time for the OCC to be more “open-minded” in its approval of more merger applications, but rather a point at which the agency should commit to pause its approval of additional bank mergers until the guidelines are updated.

Reform Needed

Reform has long been needed to adjust the process through which regulators approve bank mergers, specifically to mitigate the potential risk to the broader financial system. As Senator Reed (D-RI) noted, when drafting Dodd-Frank following the 2008 financial crisis, legislators required merger calculations to consider financial stability. This has been unevenly applied by agencies. Steps towards the necessary reforms are in progress:

Biden’s Call for Updated Bank Merger Guidelines

Reform is necessary. President Biden recognized this early into his presidency. In his July 2021 executive order on promoting competition in the American economy, the President called for updated guidelines on banking mergers to provide more robust scrutiny of mergers before they are approved. Two years later, stronger guidelines are in the works but have yet to be published by the relevant agencies.

Stronger Action by the Justice Department

Last month, Assistant Attorney General Jonathan Kanter delivered remarks at the Brookings Institution suggesting that the DOJ may be willing to consider a broad range of factors – beyond two dimensions of competition, deposit concentration and the geographic concentration of bank branches – in its own assessment of mergers and ultimately exercise its authority in blocking mergers as it sees fit moving forward.

His remarks came at the 60th anniversary of a landmark Supreme Court decision – United States vs. Philadelphia National Bank (PNB) – which upheld the Department of Justice’s authority to block bank mergers even after those mergers have been approved by the banks’ primary regulators.

The Bank Merger Review Modernization Act

At Wednesday’s hearing, Senator Warren announced her intention to reintroduce The Bank Merger Review Modernization Act to strengthen the statutory framework under which bank and savings and loan holding company mergers are evaluated. It would seek to:

- Guarantee that any bank merger approved must be in the public interest

- Give the CFPB oversight of mergers between consumer-facing banks

- Require clear risk metrics to assess the systemic risks of bank mergers

- Require that merger process discussions are made public

- Require banking regulators to make clear assessments of individual anticompetitive risks

- Allow only banks with strong risk management records to merge

Last Congress, the bill’s house companion was led by Representative Jesús “Chuy” García (D-IL).

A Holistic Approach to Bank Mergers

As we move forward, systemic changes in bank merger review will be necessary, particularly to safeguard consumers, communities, small businesses, and the stability of the financial system from the mounting threats of bank consolidation. It will take a holistic review approach and a united effort from the administration, its leaders, Congress, and regulators, particularly as the sector recovers from this moment of turbulence.

—————————————————————————

A Look Ahead:

Next week, both the House and Senate will be in session. See the relevant hearings to watch for below.

Tuesday, July 18th:

- House Financial Services hearing “Oversight of the SEC’s Division of Corporation Finance” @ 10:00 am

- House Appropriations Markup “Fiscal Year 2024 Transportation, Housing and Urban Development” @ 10:30 am

Wednesday, July 19th:

- Senate Appropriations “Hearings to examine the FY 2024 budget for the Securities and Exchange Commission” @ 2:45 pm

- Senate Judiciary “Hearings to examine trends in vertical merger enforcement” @ 2:45 pm