Fed Monetary Policy Coming Home to Roost

The news yesterday that rates on the average 30-year mortgage hit 7.09%, a level not seen in 22 years, was a shock but not a surprise. As a byproduct of the Fed’s set of steep interest rate hikes to combat inflation, the mortgage rate news was foreseeable. But it does not help a housing market beset by more structural, long-term problems.

Declining supply is pushing homeownership further beyond affordability for an increasing number — a phenomenon that began long before the Fed’s recent rate hikes. Available homes for sale fell by 1.1 million units from a year ago, aggravating a national shortage in housing stock. Today, we look at the housing market and discuss ways localities have succeeded in overcoming costs and supply constraints in housing.

Good Weekends all,

Dana

————————————————————————————————————————————————————

How Housing Has Fared Against Fed Hikes

Declining Affordability

Yesterday it was reported that the interest rate for the average 30-year fixed rate mortgage reached 7.09 percent, the highest level since April 2002. To homebuyers, this increase is staggering. On a $600,000 mortgage, monthly payments have increased from $2,601 per month before the Fed started hiking to $4,028 per month. If a household wanted to keep to the guidance to spend 30 percent of monthly income on housing, it would now require an annual income of $161,000, compared to $104,000 in early 2022 when the Fed began raising rates. Using 2021 numbers, that is the difference between half of married households being able to afford this hypothetical house, and only the top twenty percent of households by income being able to afford it.

Despite these higher rates, housing prices reversed their moderate decline in the second half of 2022, recouping $3 trillion in value to reach a record of $47 trillion. This combination led housing affordability to its worst point since 1984. Supporting this crisis is the fact that most homeowners have much lower costs, with a mere one percent of homes having changed hands over the last year. The lack of inventory has gotten so bad that Mark Hamrick, senior economic analyst with Bankrate said it was “emerging as something akin to a structural problem.”

To the good: housing starts fell by 25.7 percent from April of last year to January of this year, but have since rebounded by 8.4 percent. In the year ending last month, housing starts increased by 3.9 percent, beating economists’ expectations. Furthermore, the stock of multi-family housing under construction hit its highest recorded level.

Harder to Become A Homeowner

The aggregate homeownership statistics paint an encouraging picture. Ignoring the pandemic-induced spike in the middle of 2020, homeownership has increased notably since the beginning of 2020, and while the rate of increase has slowed since the Fed started hiking, an additional 0.6 percent of households own the home they occupy.

But a granular look shows worrying trends. From 2021 to 2022, the share of first-time home buyers declined from 34 to 26 percent. This data will likely continue, as the National Association of Realtors’s First-Time Homebuyer Affordability Index showed a ten percent decline in affordability from 2022 to the second quarter of 2023.

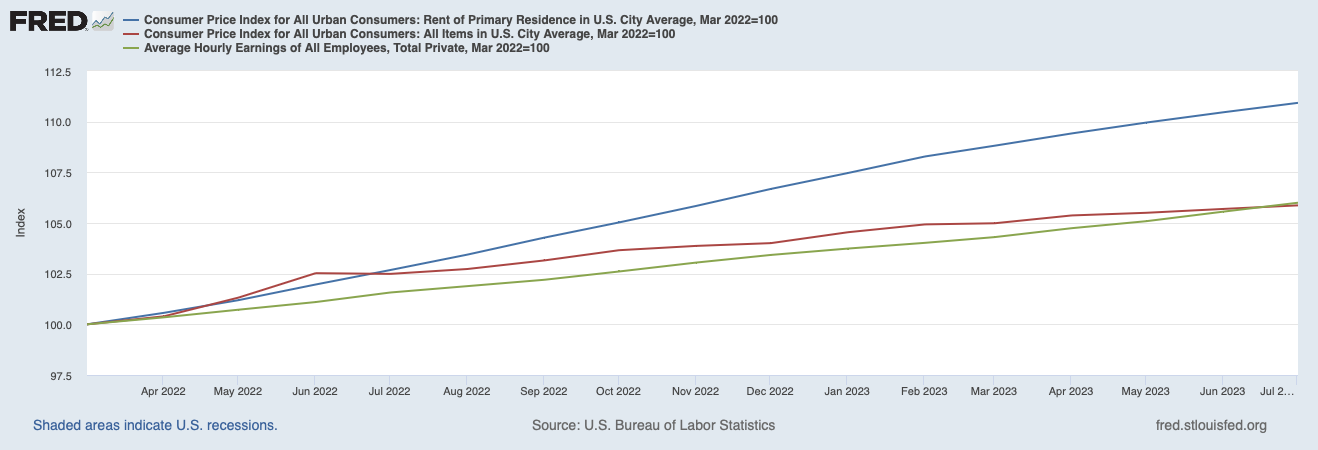

These young people who cannot afford to buy are being pushed further from the transition to homeownership by high rental prices. The typical renter now pays more than the standard 30 percent of income in rent, an increase from 25.7 percent in 2020. During this current bout of inflation, rent has increased at an above-average rate, and much faster than wages.

Rent Has Increased Faster Than Prices and Wages

The Fed and the Housing Market

Prices have increased a lot over the last two years. While rent and mortgage rates may seem similar to other price increases, they are different in one key way: the key role of debt in the housing market means that interest rate hikes can raise housing prices. The easiest way to see this is in mortgage rates. Per the graph below, mortgage rates tend to move in the same direction as changes in short-term interest rates. It is no wonder that the fastest series of rate hikes in decades has been accompanied by a similarly fast increase in rates.

Mortgage Rates Tend to Move with Short Term Fed Rates

To compound these cost increases, home builders are being hurt in two directions by interest rate increases: their borrowing costs increase, while the cost of the housing units they build increases for commercial or residential buyers. They create supply constraints and reduced demand. For home builders, the extreme supply constraints have provided something of a buffer to these forces.

Still, even as housing prices are driven higher by higher interest rates, increasing housing prices provide much of the justification for higher interest rates. In fact, 90 percent of the most recent release of price increases could be attributed to housing.

A Crisis Holding Us Back

Since the 1980s, high-wage areas have exported cost-of-living refugees to regions with cheap housing. Home prices have increased faster than construction costs as artificial barriers to construction caused them to fall relative to the population. To cope with the rapid increase in the number of commuters coming in from the suburbs, urban areas were forced to remove midrise multifamily housing that lacks the economic dynamism of high-density urban cores, but is difficult to plan high-volume traffic through. This process peaked from 1955 to 1980, the peak of interstate construction.

These changes facilitated what has been called “sprawl without growth.” This involved households migrating from urban to suburban areas, leading to the demolition of urban housing to create more convenient commuting routes. Consequently, the same number of people ended up occupying a significantly larger urban area.

A 2019 analysis in the American Economic Journal found that from 1964 to 2009, the restrictions on growth in just New York, San Jose, and San Francisco cut growth by 36 percent. To put that finding into perspective, 2009 GDP per capita would have been 3.7 percent higher. Contextualizing that number, in 2009, the depths of the Great Recession, GDP per capita fell an average of 2.5 percent.

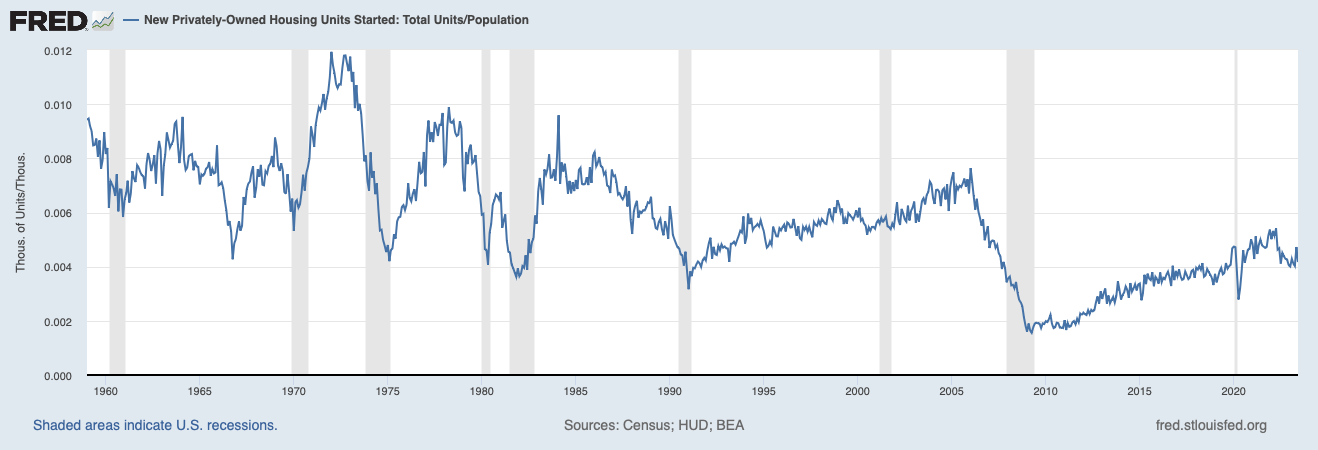

It is unlikely that the dampening of growth slowed after 2009. The graph below shows the number of housing units started in each month per person from January 1959 until June 2023. What is evident is that the production of housing has not kept pace with population growth and has yet to recover from the decline it experienced in the aftermath of the Great Recession.

The Rate of Housing Production per Person has Declined

Policy Landscape

To exemplify how supply and demand interact in the housing market, one good case study is Minneapolis, the first major metropolitan area to see its annual inflation fall below the Fed’s target of two percent. From 2010 to 2018, Minneapolis’ population grew by 12 percent, while housing costs increased by 40 percent. In 2018, the city passed a plan banning single-family zoning and allowing for large housing developments around transit hubs. To counter the fear of nothing but luxury housing being built, the city council adopted a temporary measure requiring at least a tenth of the units in new buildings be earmarked for residents making as much as 60 percent of the area’s median income. Since then, the city has provided $320 million in rental assistance and subsidies, unleashing a boom in construction which has led to local rent growth of just one percent since 2017, far from the 31 percent nationwide figure.

The fight to pass the abolition of single-family zoning in Minneapolis reveals the economic interests at the heart of the housing crisis: local homeowners. Housing has historically been the largest component of household wealth, and as a result, there has always been a large and motivated population interested in keeping prices high. So, when the issue is decided in local government, where engagement is generally the lowest, these homeowners have been the most successful in blocking reforms that would increase supply.

An interesting approach to this problem comes from New Jersey. In 1983, the State Supreme Court ruled against exclusionary zoning that prevented the construction of affordable housing. In 2015, after local groups had successfully blocked regulations that would have updated affordable housing rules, the State Supreme Court created a new solution: the builder’s remedy lawsuit. If towns do not negotiate plans to build affordable housing, developers can avoid all municipal processes so long as at least 20 percent of their housing units are affordable.

Meanwhile, in California, a report shows that only 16 percent of households in the state could qualify to purchase the median-priced single-family home. Those households would need to earn an annual income of $208,000 to qualify for a 30-year mortgage. While a full explanation of the state’s housing woes would be too long for this forum, Proposition 13, an initiative passed in 1978, is worth singling out. It caps property taxes at one percent of assessed value, which can only increase by two percent per year unless the property is sold. In the expensive California real estate markets, this has led to massive subsidies that increase lock-in and delay the transition from renting to buying.

Next National Steps

The federal government takes a leadership role in pressing for actions that will increase the housing supply. President Biden has taken a good first step with his Housing Supply Action Plan, which would reward jurisdictions that have reformed zoning and land-use policies, deploy financing mechanisms to improve funding, and, most notably, allow government-secured agencies to insure loans to purchase cheaper, manufactured homes. These policies by themselves are good, but the White House should learn from the example of New Jersey, and add a stick to their carrot. Explicit and implicit subsidies to existing homeowners should be threatened in areas that restrict construction.