Update 707 — Inflation Down to 2.97%:

June CPI Report Hints at Soft Landing

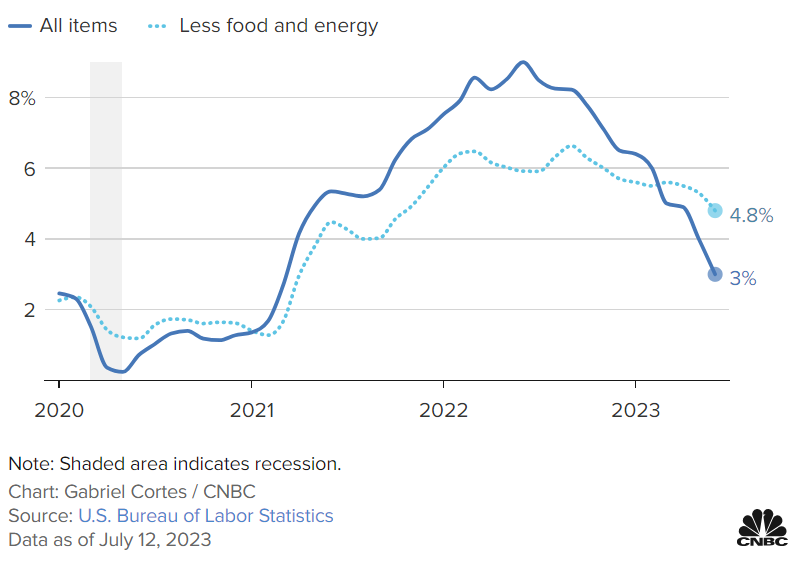

Today’s CPI report for June showed prices falling for the thirteenth month in a row, from 4.0 percent last month to a surprisingly low 3.0 percent, the lowest reading in 27 months. Prices for some items are proving stubbornly sticky, with core inflation — an inflation metric that includes services but omits food and energy price changes —down from 5.3 to 4.8 percent. The news has to be almost universally regarded among Americans as encouraging.

Happiest of all might be Federal Reserve chair Jerome Powell. Not many analysts forecast a soft landing — bringing inflation under two percent as quickly as possible without precipitating a recession — for the simple reason that it has never been achieved following such a steep and rapid set of rate hikes. Is the landing strip in sight for the crew piloting our monetary policy? See below…

Best,

Dana

Inflation Continues to Cool

Inflation continued to cool last month in a positive sign for the Federal Reserve before it decides the fate of interest rates at the end of this month. This morning’s Consumer Price Index (CPI) data showed that headline inflation rose by 0.2 percent in June, an annual increase of 3.0 percent. June’s CPI marks a significant decline from July 2022 when inflation reached a four-decade high of 9.1 percent year-on-year.

Year-Over-Year Percent Change in CPI

Source: CNBC

The increase in headline CPI was driven by an increase in shelter costs which rose by 0.4 percent over the month and contributed to over 70 percent of the overall increase. The energy index rose by 0.6 percent last month. Meanwhile food prices rose by 0.1 percent following a trend of small or no increase over the past few months.

Looking at headline inflation alone paints a comforting picture. Headline inflation has fallen since the year began, with the largest monthly increase coming in January at 0.5 percent. By May, the monthly increase had fallen to 0.1 percent and remained low at 0.2 percent in June. The year-on-year increase in CPI was about three percent in June, slightly above the Fed’s target of two percent. Core CPI, however, has remained more stubborn.

Each month this year, CPI has increased by 0.4 or 0.5 percent. Last month, that figure came in much lower, at 0.2 percent, representing a 4.8 percent increase year-on-year. This represents the smallest monthly increase in consumer prices since August 2021. Shelter costs have been a key factor keeping core CPI high. Core CPI has been slow to reflect the trends in real-world shelter costs which industry data has shown to be coming down. Shelter costs are therefore expected to fall in future CPI reports.

As the prices of goods have fallen and shelter costs are expected to continue declining, the Fed’s focus shifts to service costs. As service costs have traditionally been linked to wages, the ongoing rise in wages may incline the Fed toward additionally restrictive monetary policy.

While today’s CPI data offered welcome news for the Fed, it is unlikely to avert a widely expected 25 basis point interest rate hike at the FOMC’s meeting on July 25-26. Such a hike would take the federal funds rate to the 5.25 to 5.5 percent range.

Labor Market Remains Strong in June

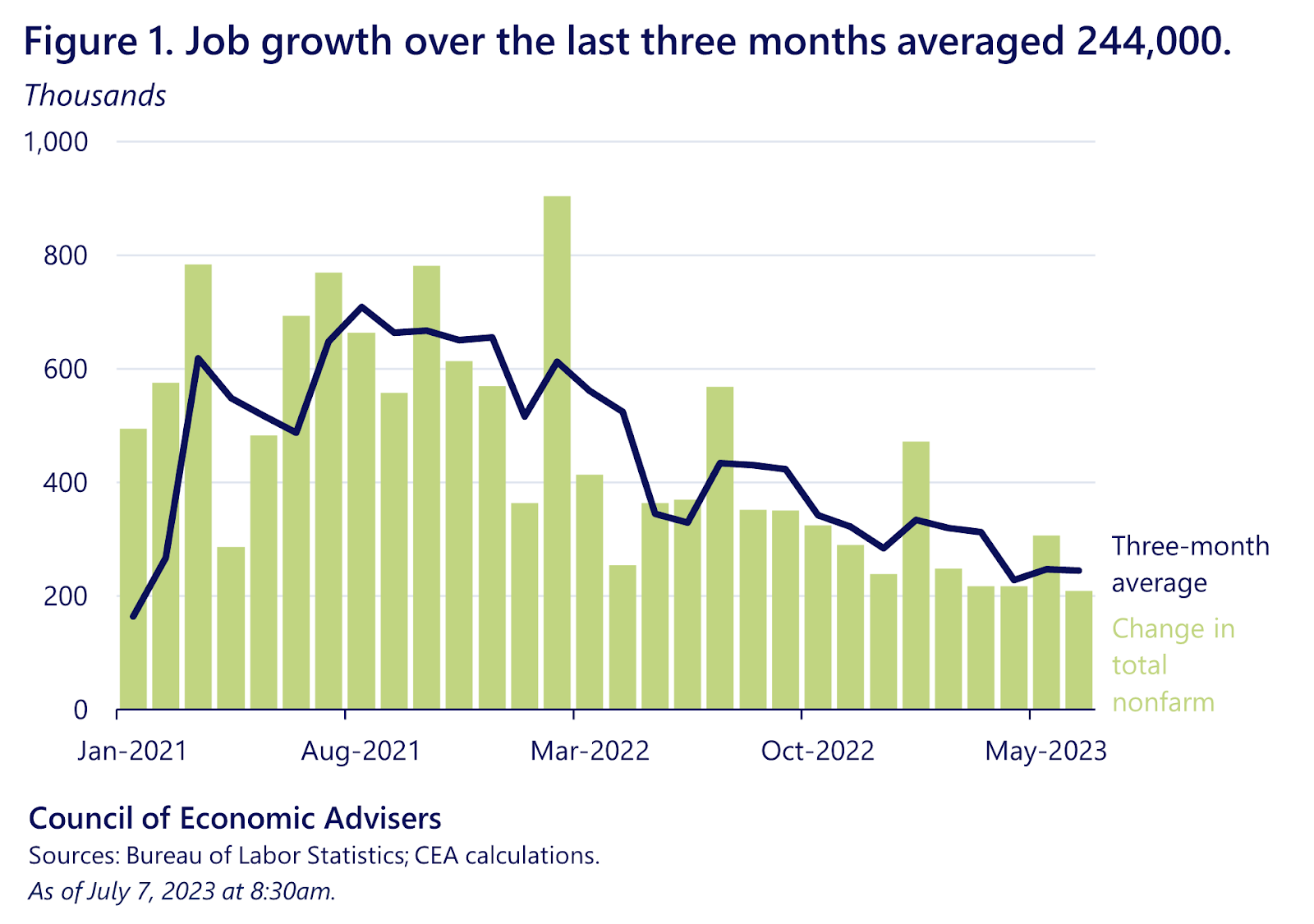

The Bureau Labor Statistics released jobs data for June 2023 last week. The report showed continued strength in the labor market despite some signs of a slowdown, as total nonfarm payroll employment rose by 209,000 over the month, and unemployment ticked down to 3.6 percent.

The labor market appears to be cooling down from the red-hot condition to which we have become accustomed. Payroll employment is increasing more slowly than it was last year, and the BLS made significant downward revisions to estimates from the last two months. Additionally, the number of people working part time due to economic reasons increased by 452,000 to 4.2 million.

Changes in Nonfarm Payroll Employment

That said, a cooldown of this degree should not spark fears of a recession. Unemployment has remained low. The prime-age employment-to-population ratio hit a new post-pandemic high last month, due in large part to rising labor force participation rates. The number of short-term unemployed and those working part-time for economic reasons are both still relatively low, despite the increases we saw last month.

Average hourly earnings for all employees rose 0.4 percent in June and 4.4 percent over the last year. Strong wage growth in June should not be a major concern for the Fed, however. Wage growth has been slowing, particularly in core non-housing services, which is the Fed’s primary concern. And, with inflation continuing to fall, the Fed may not need to aggressively crush demand in order to quell wage-driven inflation.

However, we expect the Fed to pursue additional rate increases in an attempt to loosen labor market conditions and reign in inflation. The Fed will want to see wage growth continue to slow and the ratio of vacancies to unemployed fall from its current 1.6 percent level, although it should be noted that vacancies data can be unreliable and may make the labor market appear tighter than it really is. As always, the Fed will need to be cautious not to reverse the gains that workers have seen since the pandemic began. Crush labor demand too aggressively, and the central bank risks missing the still-open window for a soft landing and triggering a recession.

Overall Economic Outlook and Impact

In non-emergency situations, the FOMC’s decisions don’t directly set short-term interest rates at their ideal levels. Instead, they determine the appropriate rate of interest rate adjustment based on their dual mandate of maintaining price stability and full employment. To achieve this, they consider three factors during each meeting: the gap between measured and target inflation, the gap between measured and potential output, and the gap between interest rates and the terminal interest rate, which is the theoretical rate at which the Fed’s mandates are fulfilled.

Based on the minutes from June’s meeting and the recent statements from San Francisco Fed President Daly, Vice Chair for Supervision Barr, and Cleveland Fed President Mester, it appears that the Fed’s decision to pause was driven by the conclusion that the optimal rate of change in the discount rate has fallen below 25 basis points per month.

The evidence of slower growth in wages, prices, and employment challenges our initial expectations. Considering Powell’s renewed commitment to the two percent inflation target, today’s data suggests that the FOMC may opt for a rate of change in interest rates below the rate of 12.5 basis points per month over its remaining meetings this year. This decision could be particularly difficult given that the Fed’s preferred inflation measure, PCE, will be released just two days after this month’s FOMC meeting, July 25-26.

Continued weakness in the banking sector could complicate the decision further. This week, bank earnings reports will be released, and in light of the confidence shock earlier this year, the FOMC will closely monitor a few key factors: the persistence of deposit flow towards too-big-to-fail institutions, the impact of emergency market-rate loans under the Lombard Street rule on net-interest income, and headcount as an indicator of future expectations from company executives.

What lies ahead is a paradox. The challenges in managing a soft landing get more difficult the closer you get to the two percent target. Ironically, the resilience of the American economy — our recovery has been among the strongest in the world — could make it more difficult. So far, working-class Americans have experienced positive change. For example, workers in the restaurant and hotel industry, often part of the working poor, witnessed a significant 28 percent increase in their wages from 2021 to 2022, surpassing inflation. Additionally, the income gap between the top 10 percent and the bottom 10 percent has narrowed by over a quarter of the increase observed since 1980 during these two years. The Wall Street Journal’s recent coverage of a “richcession” further exemplifies this trend, highlighting that the burden of economic weakness is now felt by those who are most financially capable.