Update 751 — Fed Set to Pause Past March;

When Does “Higher for Longer” Go Too Long?

This week’s meeting of the Federal Reserve was not considered “live” — as another pause in rates was universally expected. Indeed, the Fed held rates steady today at the 5.25 to 5.50 percent target level, the peak at which it arrived in July. With inflation moving down from three percent, chugging toward the Fed’s long-standing two percent goal, the question now is: when will the Fed go “live” and weigh lifting its foot off the break, having suggested last month that 2024 will end with cuts bringing rates to around 4.6 percent? Probably not at its next meeting in March, we learned today.

Democratic Senators Brown, Warren, Hickenlooper, Rosen, and Whitehouse sent letters this week to Fed chair Jerome Powell, urging expeditious cuts and citing in particular, the sensitivity of “our country’s housing ecosystem,” concluding that “Working families, already struggling with the cost of housing, need relief now.” We cover the Fed’s non-move today and forward policy considerations below.

Best,

Dana

The Federal Reserve has opted to hold interest rates steady at the 5.25 to 5.50 percent range for the fourth consecutive occasion. Recent economic data suggest that a soft landing has been all but achieved. Though we are in the midst of a final descent, the potential for turbulence in the form of economic risks and uncertainties remains. The Fed must be cautious of the lag and ripple effects of its ongoing cycle of interest rate hikes moving forward.

Fed Holds Rates Steady for Now

The Federal Open Market Committee (FOMC) announced the interest rate pause this afternoon following the conclusion of its first meeting of the year. The Fed has held the federal funds rate at this level since last July after raising the rate eleven times from near zero in early 2022 to a 23-year high in its most aggressive series of interest rate hikes since the 1980s.

The main question confronting the FOMC at this juncture is how long to keep interest rates elevated before finally beginning to cut. In December, FOMC officials projected that the Fed would cut rates roughly three times this year, bringing interest rates to 4.6 percent by the end of 2024. In their statement following the meeting, the FOMC indicated that it may not be ready to cut just yet.

Data Behind the Decision

In his press conference following the meeting, Fed Chair Jerome Powell said that though inflation data over the past six months has been strong, the Fed will need to see continued data showing that inflation is coming down sustainably before it begins to cut rates. Powell said that, while it is likely that trends of inflation moving towards the Fed’s two percent target over the past six months will persist, the FOMC would like to confirm that this trend is not due to factors that will wane over the coming months or that, as Powell suggested was a more likely risk, inflation does not flatten out above the two percent level. Notably, Powell stated that the Fed is not looking for weaker growth or labor market data.

Powell also indicated that the Fed is prepared to hold rates steady depending on new data but that an unexpected weakening in the labor market could push the Fed to cut rates sooner.

Powell’s remarks come after five Senators urged him to lower rates over the past few days. On Sunday, four Democratic Senators – Senators Elizabeth Warren (D-MA), John Hickenlooper (D-CO), Jacky Rosen (D-NV), and Sheldon Whitehouse (D-RI) – urged Powell to reverse the Fed’s recent interest rate hikes this year citing concerns that high interest rates have made housing even less affordable and accessible to American families. Yesterday, Chair of the Senate Committee on Banking, Housing, and Urban Affairs, Sherrod Brown (D-OH), joined his colleagues, calling on Powell to “ease monetary policy early this year.”

Economy’s Continued Strength — a Concern?

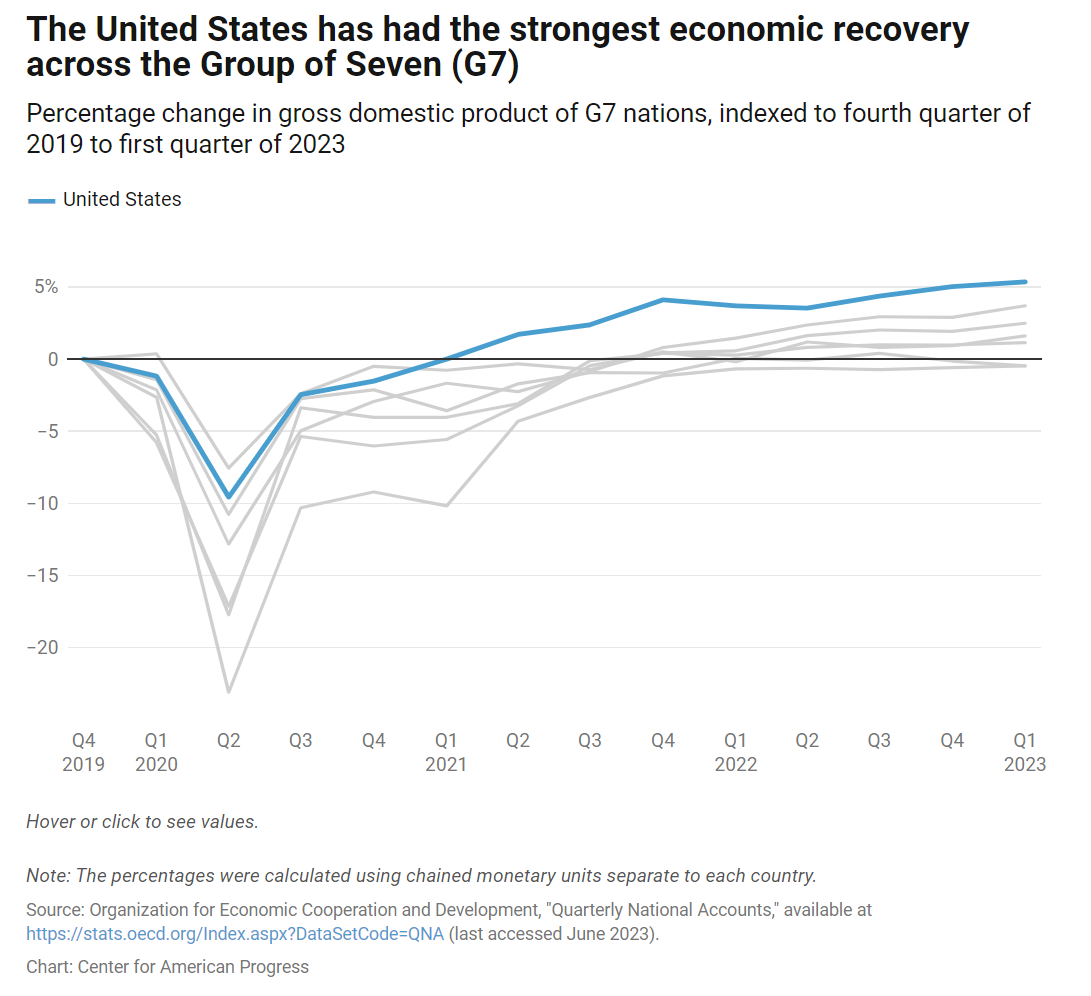

The U.S. economy has remained remarkably resilient in the face of the Fed’s aggressive rate hikes. In fact, the American economy’s post-pandemic recovery has been the strongest of the world’s large advanced economies.

Source: Center for American Progress

By the end of 2021, the U.S. economy had entirely reversed all pandemic-era decreases in GDP and has since returned to its pre-pandemic growth path. Last year, GDP rose by 3.1 percent, up from less than one percent in 2022 and above the average GDP growth during the five years before the pandemic began. The economy is expected to continue to grow in the first quarter of this year, though more slowly than in 2023. Last quarter’s GDP growth was primarily driven by an increase in consumer spending, enabled by a strong labor market. Consumption rose by 0.5 percent in December, representing the largest increase in consumer spending since January of last year.

The target of the Fed’s most recent cycle of interest rate hikes, inflation, has fallen significantly from its peak and is continuing to trend towards the Fed’s target level for price stability of two percent. The personal consumption expenditures (PCE) price index – the Fed’s preferred measure of inflation – has fallen after briefly reaching seven percent in mid-2022 to a 2.6 percent increase on a year-on-year basis. PCE rose by 1.7 percent – below the Fed’s target of two percent – over the fourth quarter of last year.

Approximately 2.7 million jobs were added to the U.S. economy last year, after extraordinary growth of roughly 4.8 million jobs in 2022. This moderation will allow current payroll growth to be sustainable as long as the labor force continues to grow. Unemployment has remained at historically low levels. The unemployment rate has remained below four percent over the past 23 months. Meanwhile, the prime-age labor force participation rate has held above its pre-pandemic peak for all of 2023 due to immigration and women reentering the workforce. Wage growth is above its pre-pandemic average. Average hourly earnings rose by 4.1 percent on an annualized basis in December. This rise in real wages can be non-inflationary if productivity remains strong as it has over the past few quarters. But if the economy’s robust recovery continues apace, the threat of inflation reignition persists.

In the Midst of a Soft Landing, Risks Remain

The continued strong growth and labor market trends paired with the downward trend in inflation show that the American economy is in the final descent to a once-tentative soft landing, in which inflation is reduced without a significant negative impact on the labor market. While the recession that many economists once predicted has yet failed to materialize, economic risks and uncertainties remain. Strong growth is no guarantee against the risk of recession. The Fed’s spate of interest rate hikes has continued to ripple across the economy.

- Consumer Spending: Elevated interest rates have put stress on credit markets. The consumer spending that has driven strong economic growth could lose steam. As Democratic Senators cited in their letter, the Fed’s interest rate hikes have already led to higher mortgage costs for home purchasers, higher rents, and reductions in new homes and apartment buildings, all leading to less spending power for consumers. The average 30-year fixed rate mortgage rose as high as eight percent in mid-October. Though mortgage rates have since fallen, they remain historically elevated. Sales of existing homes have also plummeted, falling 30 percent from 2021, as high rates discourage many who would like to move from selling.

Credit card debt hit a record high of $1.1 trillion in the third quarter with delinquencies, although still very low, at their highest level since 2011. Student loan payments, which were paused during the pandemic, have also resumed. These factors together may drive consumers to reduce their spending in the coming months.

- Commercial Real Estate: Rising interest rates have also put pressure on the U.S. commercial real estate market, where prices have fallen by 11 percent since the Fed began its current cycle of interest rate hikes. Those locked in lower interest rates earlier in the pandemic might struggle as that debt is refinanced at higher rates. An estimated $1.2 trillion in commercial real estate debt is set to mature in the next two years, roughly a quarter of which comprises loans to the office and retail segments the majority of which is held by banks and commercial mortgage-backed securities.

- Geopolitical Risk: The spike in inflation during 2022 was in part a result of supply-side shocks. Monetary policy was not the best tool to address this. Geopolitical risks, which have generally contributed only a small part to previous U.S. recessions, could result in new supply chain shocks. Additionally, geopolitical tensions could pose a significant threat to economic growth.

Over the course of the coming months, the Fed will have to weigh the risks of holding interest rates at an elevated level for too long against those of loosening monetary policy before the economic data reflects progress toward their target outcomes. Powell and other FOMC officials have repeatedly stated that they prefer to keep rates higher for longer than “prematurely” to cut interest rates and have to hike later in this cycle.

The FOMC will meet next on March 19 and 20 and is – barring unexpected economic data in the interim – expected to hold interest rates steady once again, as Powell hinted broadly today, with markets dipping across the board on the news.