Update 752 — A Moderate Tax Triumph:

House OKs Bill; Senate a Speed Bump?

In a rare display of “regular order,” the House voted Wednesday on the $79 billion tax package that partially restores the Child Tax Credit and three corporate tax breaks, following an actual Ways & Means markup last week, passing the bill by an overwhelming 357-70 margin. But it will hit a speed bump in the Senate, where a vote may not come until the end of the month after the foreign assistance supplemental request is considered there.

Today’s jobs report showed the U.S. economy adding a whopping 353,000 jobs in January, a way more than “neutral” number (if the economy were neither growing nor shrinking), well above expectations. Wages increased over the month by the most since March 2022. The report signals a Groundhog Day’s forecast of warmer economic weather ahead.

Good weekends, all…

Best,

Dana

Headline

Bipartisan Tax Package Passes in the House

On Wednesday, the House of Representatives passed the Tax Relief for American Families and Workers Act in a bipartisan 357-70 vote. The $79 billion tax package offers much-needed assistance to low-income families by partially expanding the Child Tax Credit (CTC).

The $33 billion cost of the expanded CTC would be equal to that of three business provisions that lower corporate tax liabilities. An additional $13 billion would extend the Low Income Housing Tax Credit (LIHTC), provide tax relief for disaster victims, and create a special carve-out agreement with Taiwan. This package will be largely offset by changes to the COVID-era Employee Retention Tax Credit.

While this bill enjoyed broad bipartisan support, 23 Democratic Representatives voted against the package. Though the CTC expansion is expected to help 16 million children in low-income families and pull as many as 400,000 children out of poverty, the legislation doesn’t go far enough for key advocates like House Appropriations Committee Ranking Member Rosa DeLauro (D-CT), who stated that the deal “lopsidedly benefits big corporations while failing to ensure a substantial tax cut to middle- and working-class families.” In other words, progressives would receive a broader expansion of the CTC by agreeing to high-value corporate tax cuts. However, many Democrats supported this bill with hopes that this expansion would set the stage for further beneficial reform in 2025.

Republicans in high-tax states, such as New York and California, also voted no on the bill after threatening to block floor procedure earlier this week unless provisions to increase the cap on State and Local Tax (SALT) deductions were added to the tax deal. To avoid any further delay, House leadership committed to a separate vote on the SALT cap as early as next week.

Republicans, especially members of the House Freedom Caucus (HFC), voiced additional concerns about the ability of undocumented immigrants to receive CTC benefits. House Ways and Means Chairman Jason Smith (R-MO) quickly dismissed the objection, noting that the tax package contains language consistent with Trump-era CTC legislation and requires valid SSNs for the children of recipients.

The tax package is now in the hands of the Senate, where it faces Republican opposition and a congested agenda. Senate Republicans are principally concerned that the proposal’s “lookback” provision, which allows beneficiaries to choose between their past two years’ income to calculate the value of their credit, will disincentivize workforce participation. However, beneficiaries are unlikely to leave the workforce and give up a source of income solely because they have “locked in” a higher-value credit based on earned income in a previous year.

The package must also compete with a long list of priorities for the Senate as they prepare to take up the National Security Supplemental and continue work on the array of appropriations bills. The tax package is likely to be brought to the Senate floor at the end of the month. While it does have a chance to move as a standalone bill, the most viable vehicle may be in the first set of appropriations bills set for March 1.

Appropriators Agree on 302(b) FY24 Allocations

Late last week, Appropriations Committee Chairs Representative Kay Granger (R-TX) and Senator Patty Murray (D-WA) struck an agreement on funding levels for each of the 12 appropriations bills for Fiscal Year (FY) 2024, otherwise known as 302(b) allocations.

Though the exact levels will not be released before text of individual appropriations bills, they likely look similar to bipartisan funding bills proposed by the Senate before the end of FY23. In one necessary change, funding for the Department of Homeland Security (DHS) will be higher than originally thought to make up for $2 billion in emergency funding for DHS that was eliminated during the top-line negotiation.

Work on allocating funding within each of the 12 appropriations bills has continued as subcommittee chairs can now negotiate and draft bills consistent with 302(b) targets. House Republicans remain adamant about including extreme policy riders, otherwise referred to as “poison pill provisions.” But Democrats have signaled that they will only support clean legislation that is also reflective of the top-line funding agreement struck between Majority Leader Chuck Schumer (D-NY) and Speaker of the House Mike Johnson (R-LA) earlier this year.

The three potential endgame outcomes to avoid partial government shutdowns on March 1 and March 8:

- Full passage of appropriations bills

- Another set of short-term CRs

- A full-year CR (which would likely lead to a ~9 percent cut in NDD spending)

Congress could use a combination of these measures if they agree on some appropriations bills and not others, but members will strive to avoid the use of another short- or long-term CR by ironing out and voting on legislation before the March 1 and March 8 funding deadlines.

Other Developments

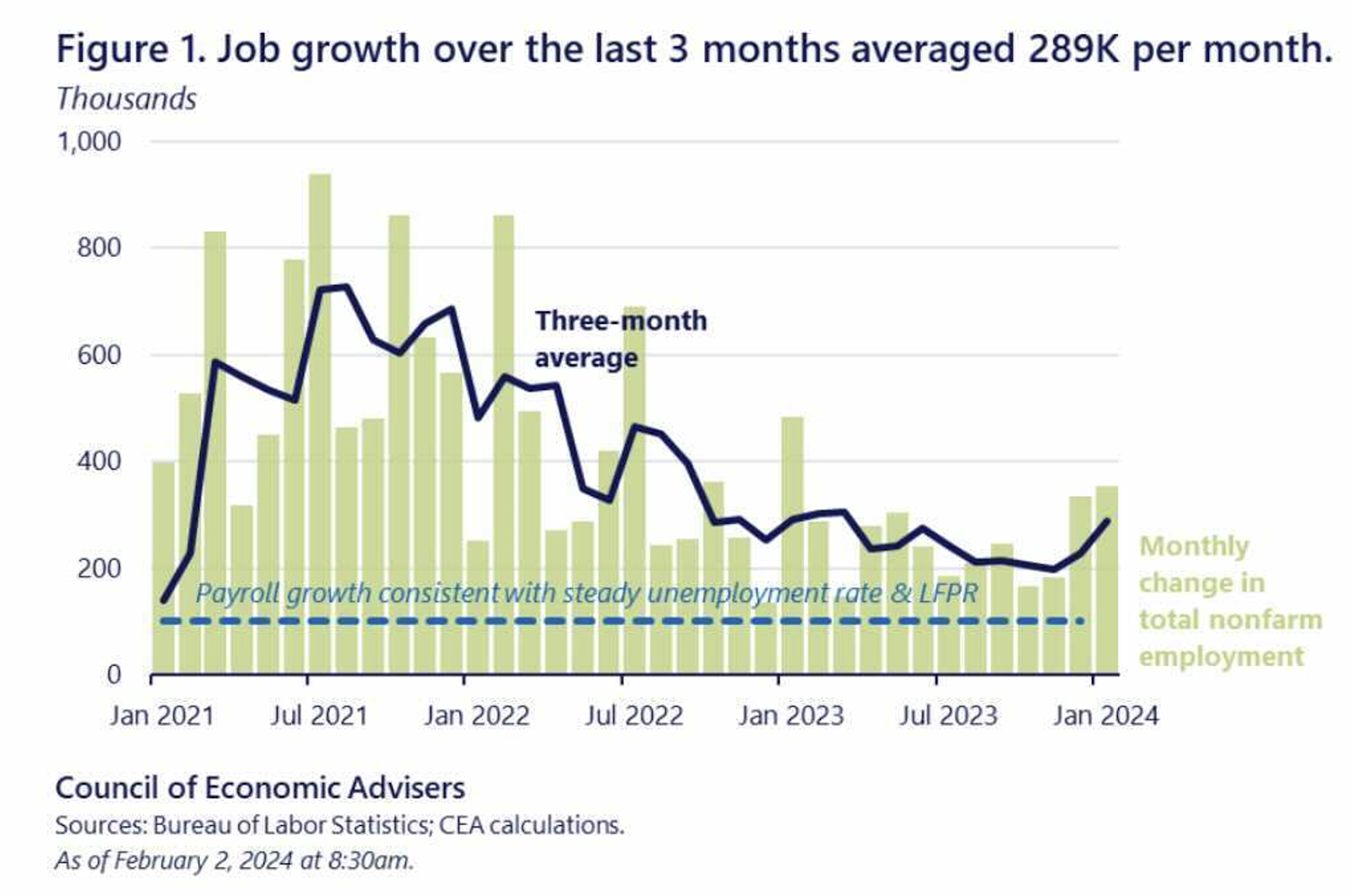

Economy Adds a Blowout 353,000 Jobs in January

A remarkable 353,000 jobs were added to the U.S. economy in January, far exceeding expectations, according to the January jobs report released this morning. In a further sign of the labor market’s continued resilience, total nonfarm payroll employment for November was revised up by 9,000, from 173,000 to 182,000 and the change for December was revised up by 117,000, from 216,000 to 333,000. These revisions bring the monthly average job gain in 2023 to 255,000.

Source: Council of Economic Advisors

The largest gains in January came in professional and business services, which added 74,000 jobs, health care, which added 70,000 jobs, retail trade, which added 45,000 jobs, and social assistance, which added 30,000 jobs. Employment declined in the mining, quarrying, and the oil and gas industry.

The unemployment rate remained unchanged at 3.7 percent. The rate continues to hold at historically low levels and has remained below four percent for 24 months. The labor force participation rate fell slightly from 62.6 percent in December to 62.5 percent last month. Prime-age labor force participation rate ticked up to 83.3 percent. Average hourly earnings rose by 0.6 percent last month and by 4.5 percent over the past 12 months.

The surprisingly strong labor market data may reinforce the Federal Reserve’s inclination to be patient in considering cuts to interest rates which they’ve held steady at the 5.25 to 5.5 percent range since July. In December, Federal Open Market Committee (FOMC) officials projected three rate cuts in 2024, bringing interest rates to about 4.6 percent by the end of the year. This morning’s data is likely to confirm officials that another pause is appropriate when they meet next in March.

OCC’s Hsu Offers Change to Bank Merger Review Policy

Office of the Comptroller of Currency (OCC) Acting Chair Michael Hsu announced that the OCC would be adjusting its process for approving bank mergers in remarks at the University of Michigan School of Business on Monday.

Hsu announced that the OCC would issue a notice of proposed rulemaking to make two substantive changes to its business combination regulation:

- Removal of the automatic approval of bank mergers following the comment period – The proposed rule would remove the expedited review procedures which allow qualifying filings to be automatically approved 15 days after the close of the comment period unless the OCC notifies the applicant that the filing is not eligible for expedited review, or the expedited review process is extended.

- “Chalk lines” – The proposed rule would effectively provide chalk lines demarcating three groups of merger applications based on factors including the acquiring bank’s safety and soundness and the extent to which it has earned the trust of its supervisors and the communities it serves.

The proposed changes are small steps toward addressing long-standing issues in the process through which regulators approve bank mergers.

The OCC approves mergers involving nationally chartered banks. Completing an update to the analytical frameworks on bank merger guidelines that federal banking agencies and the Department of Justice follow when considering bank mergers, and including a consideration of the systemic risk individual mergers could pose, could provide more meaningful reform.

Hearings

HFSC Subcommittee Considers Banking Reg. Proposals

The House Committee on Financial Services Subcommittee on Financial Institutions and Monetary Policy convened on Wednesday morning for a hearing examining recent proposals by federal banking regulators.

While the hearing discussed numerous regulatory proposals put forward over the past year – including the long-term debt requirements proposal, the resolution planning requirements proposal, and the G-SIB surcharge proposal – members on both sides of the aisle focused on the Fed, FDIC and OCC’s joint Basel III Endgame proposal. The Basel Endgame proposal would enhance the financial system’s ability to withstand periods of stress by implementing stricter capital requirements on banking firms with $100 billion or more in total assets and firms that engage in significant trading activities.

Subcommittee Ranking Member Bill Foster (D-IL) highlighted the importance of strong capital requirements in ensuring that banks can continue lending in times of stress without putting taxpayers at risk of funding another bailout but also acknowledged the need for calibration to minimize the negative impact of unintended consequences. Foster noted that Federal Reserve Vice Chair of Supervision Michael Barr has estimated that the cost of capital for the largest banks would increase by three basis points. While other estimates may be higher, the increased costs to banks would be a small fraction of a percent. Congressman Foster raised concerns about how this increase will trickle through the economy.

Representative Brad Sherman (D-CA) raised the importance of tailoring and stated that the proposal gives no credit for private mortgage insurance which may hurt first-time homebuyers and people of color.

Subcommittee Chair Andy Barr (R-KY) once again called on regulators to scrap the proposal and to “reevaluate what, if anything, may need to be done.”

Senate Budget Examines Housing Affordability

On Wednesday, the Senate Committee on the Budget held a hearing on housing affordability. Committee Chair Sheldon Whitehouse (D-RI) began by outlining the impact the current lack of affordable housing has on the broader economy, costing an estimated $2 trillion in GDP every year.

Whitehouse praised the effort that the Biden administration has put into addressing the affordable housing crisis – highlighting the American Rescue Plan and the Housing Supply Action Plan in particular– while expressing his hopes that Congress can pass legislation on affordable housing in 2024. Republican committee members, especially Senators Ron Johnson (R-WI) and Mike Braun (R-IN) focused on what they saw as a problem of reckless government spending. In addition to denouncing inefficiencies in federal housing programs, they also spoke about how the national debt puts upward pressure on mortgage rates as higher levels of debt may indirectly make the Fed more inclined to raise interest rates.

Senate Banking re Financial Fraud on Consumers

On Thursday, the Senate Committee on Banking, Housing, and Urban Affairs held a hearing to examine scams and fraud in the banking system and their impact on consumers.

The most popular way people send money today is through peer-to-peer apps like Paypal, Venmo, and CashApp. But according to the FTC, the dollar volume of losses by payment apps or services increased 25 percent from 2021 to 2022. Carla Sanchez-Adams, Senior Attorney at National Consumer Law Center, explained that payment fraud falls into two categories:

- Unauthorized transactions – transactions initiated by the fraudster without the consumer’s authority

- Fraudulently induced transactions – transactions initiated by the consumer as the result of a fraudulent scheme involving deception and manipulation by the fraudster

Sanchez-Adams noted that victims of payment fraud which occurs during an unauthorized electronic funds transfer have hope of getting their money back because of strong protections under the Electronic Funds Transfer Act (EFTA). Victims of unauthorized transactions involving bank-to-bank wire transfers, check fraud, forgery, or alteration, or the theft of an electronic benefits transfer card, however, face an uphill battle. Those who fall victim to fraudulently induced transactions have no clear protections under federal or state law.

Sanchez-Adams highlighted that other forms of payment fraud involving unauthorized transactions – including those involving wire transfers and EBT cards – as well as payment fraud involving fraudulently induced transactions should be covered under the EFTA. She also called for receiving institutions to bear more responsibility.

Look Ahead

Tuesday, February 6

- House Financial Services Committee hearing: The Annual Report of the Financial Stability Oversight Council

Thursday, February 8

- Senate Committee on Banking, Housing, and Urban Affairs: The Financial Stability Oversight Council Annual Report to Congress