Update 711 — Don’t Believe in More Hikes?

Fed Ready to Run Lag Risk while Prices Drop

The effectiveness of Fed monetary policy — hikes totaling 525 basis points over the last 16 months that have brought inflation down 6.09 percentage points since its June 2022 peak — raises the question: how do we know when it’s time to stop? The question has both economic and political consequences. The macroeconomy has demonstrated resilience in the face of steep and rapid rate increases, but that policy has a broad contractionary political impact that has persisted for a year and a half. The nation goes to the polls in just 16 months …

The lag effect did not give the Fed cause to pause again, and today’s 25 bp rate increase is not expected to be the last hike this year. What will inform Fed policy going forward? Below, we review the factors the Fed is considering, in the belief that one hike too many may not only have diminishing returns in the fight against inflation, but could imperil the soft landing objective and weigh down the post-inflation macroeconomic growth during an election year.

Best,

Dana

Fed Raises Interest Rates by 25 Basis Points

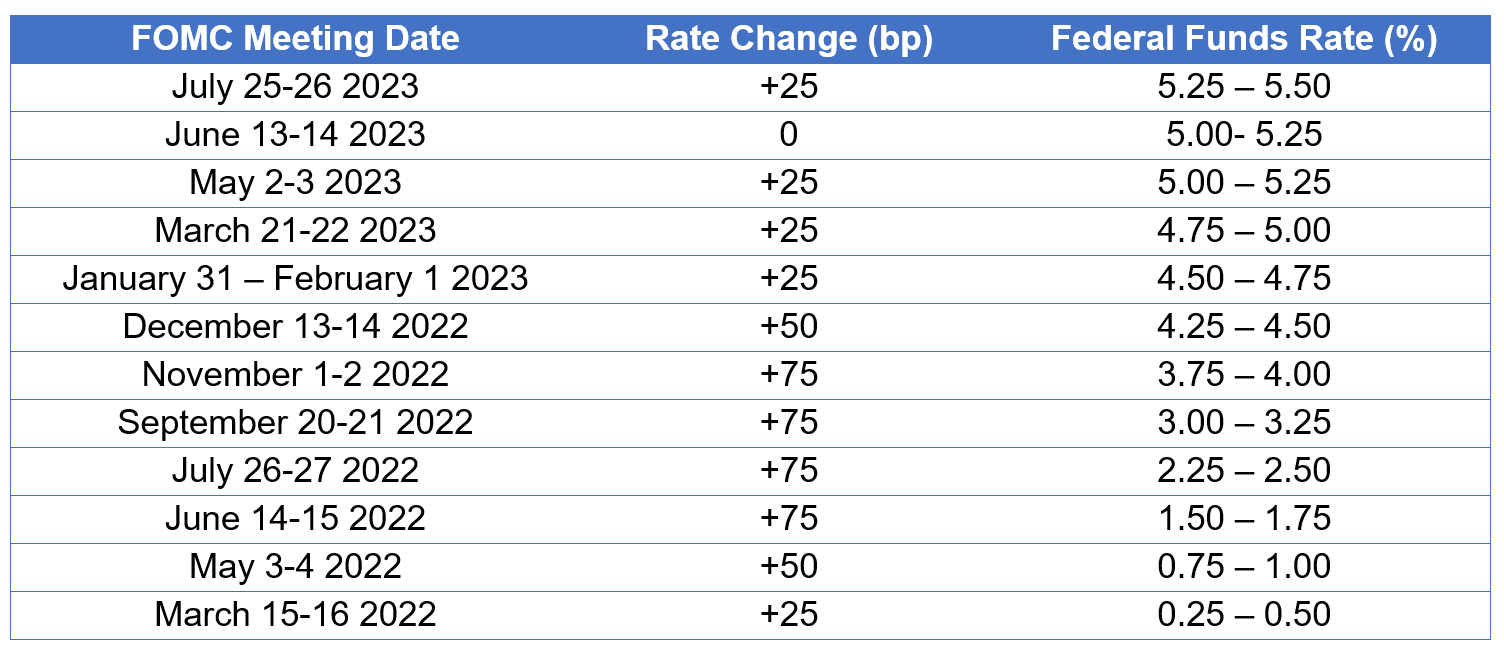

This afternoon, the Federal Open Market Committee (FOMC) raised the federal funds rate by a quarter of a percentage point, bringing it to a 22-year high of 5.25 – 5.50 percent. The FOMC’s July meeting comes at a critical point in the Fed’s cycle of rate hikes, in which it has raised rates from near zero in early 2022.

The additional hike comes as headline inflation continues its fall, steadily approaching the Fed’s target level of two percent. The personal consumption expenditures index (PCE) – the Fed’s preferred measure of inflation – fell to 3.8 percent in May, down from almost seven percent in June of last year. Last year, the consumer price index (CPI) reached a 40-year high of 9.1 percent.

- Headline inflation has come down as the impact of factors that do not stem from monetary policy – like the war in Ukraine which brought on the largest energy crisis since the 1970s and the worst avian flu outbreak in U.S. history which drove the price of eggs up to an average of $4.25 per dozen in December – has eased

- Core inflation, which excludes food and energy prices, remains stubbornly higher than the Fed would prefer, remaining steady at 4.6 – 4.7 percent this year

One aspect of core inflation, goods inflation, has come down as supply chains improve post-pandemic and consumption moves from goods back to services.

Housing services, another input to core inflation, has been key in keeping core inflation high. Core CPI data has been slow to reflect the trends in real-world shelter costs which industry data has shown to be coming down. Shelter costs are therefore expected to fall in future CPI reports.

Non-housing services (NHS), another component of the PCE index, has been more stubborn and remains above pre-pandemic levels. It is largely determined by the labor market, and the Fed will look for further softening in the persistently strong labor market in hopes that this inflation will begin subsiding. Monthly job growth remains robust but has moderated in recent months compared to blowout levels earlier this year. Fed Chair Jerome Powell noted in his remarks following the meeting, that the labor force has been growing. This may help ease the labor shortage within the “overheated” labor market without driving up unemployment.

The Monetary Policy Impact Lag

At this stage in its interest rate hike cycle, the Fed must be mindful that the speed and extent of its increases have been substantial: an overall increase of 500 basis points in under two years.

Such extensive monetary policy tightening takes time to set in, a fact that the Fed has recognized in moving to a heavily data-dependent approach in assessing the extent to which it will inflict further hikes on the economy. The full effects of rate hikes have traditionally lagged by long and variable amounts, currently thought to be anywhere from 12 to 24 months. The period of time the Fed’s restrictive monetary policy will take to fully set in is difficult to predict and poses a major challenge for the central bank. The Fed must be cautious to avoid overcorrecting and pushing the economy into a recession.

This set of rapid interest rate hikes can also cause unintended ripple effects. We saw this earlier this year as banks that failed to adequately manage their interest rate risk – Silicon Valley Bank, Signature Bank, and First Republic Bank – collapsed. Turmoil in the banking sector led to tightening in the lending market, which remains an ongoing concern. How well the overall economy will weather the Fed’s most aggressive spate of interest rate hikes since the 1980’s is yet to be seen.

Slow Descent into Soft Landing

The Fed ended its period of expansionary monetary policy by hiking rates gradually, then raised the federal funds rate by 75 basis points following each of four consecutive FOMC meetings in the second half of 2022. Last December, the Fed moved down to a 50 bp hike before implementing three consecutive 25 bp hikes early this year and deciding to hold rates steady at the last FOMC meeting in June.

The Fed only began tightening monetary policy in March of last year. As headline inflation continues to approach the Fed’s target rate of two percent, the risk of too much tightening becomes increasingly important. At this stage, the Fed must be focused more than ever on balancing its dual mandate of full employment and price stability.

In a tentatively positive development, Powell noted during his press conference that the Fed is no longer internally forecasting a recession as it had been over the past several meetings. He did, however, also note that he did not think that inflation would return to the two percent target rate until 2025.

The Fed’s statement following the meeting and Powell’s remarks following this week’s meeting suggest that we can expect more restraint from the Fed moving forward. Another 25 basis point hike may be coming over the remaining three FOMC meetings this year, with more time in between subsequent hikes. The Fed’s statement discussed “determining the extent of additional policy firming that will be appropriate” rather than reverting to language in prior statements which highlighted that the Fed would determine “the extent to which additional policy firming may be appropriate.”

Ahead for the Fed

Come September, the Fed is likely to hike again, then pause later on or to pause and leave the possibility of an additional hike in November or December open. Powell also noted that several FOMC members had indicated that they are inclined towards additional hikes next year. Powell also explicitly noted that the Fed would not be cutting rates this year.

Data on the labor market and prices will be paramount moving forward as the Fed determines the peak of interest rates this cycle. This includes the latest PCE data to be released on Friday, which is expected to show that inflation continued to cool in June, along with the two jobs reports and CPI reports set to be released ahead of the FOMC’s September meeting. If the labor market remains tentatively resilient while inflation falls, the possibility of the Fed successfully engineering a soft landing becomes significantly clearer.