A tumultuous week in Washington and the industrial Midwest hints at a set of short-term challenges that threaten the nation’s rapid recovery from the post-Covid recession. Failure this week, particularly by House Republicans bent on impeachment, to make meaningful budget making progress and avoid a government shutdown and by Detroit automakers to avert the UAW strike starting today suggest an autumn of economic uncertainty ahead.

An upward reversal in the August CPI, led by a 10 percent increase in gas prices, points to a likely resumption of the Fed’s interest rate hikes this fall. And we saw robust debate this week on financial regulation from capital requirements proposals to new SEC rules. We cover these and other major economic policy developments below.

Good weekends, all…

Best,

Dana

Highlights of the Week

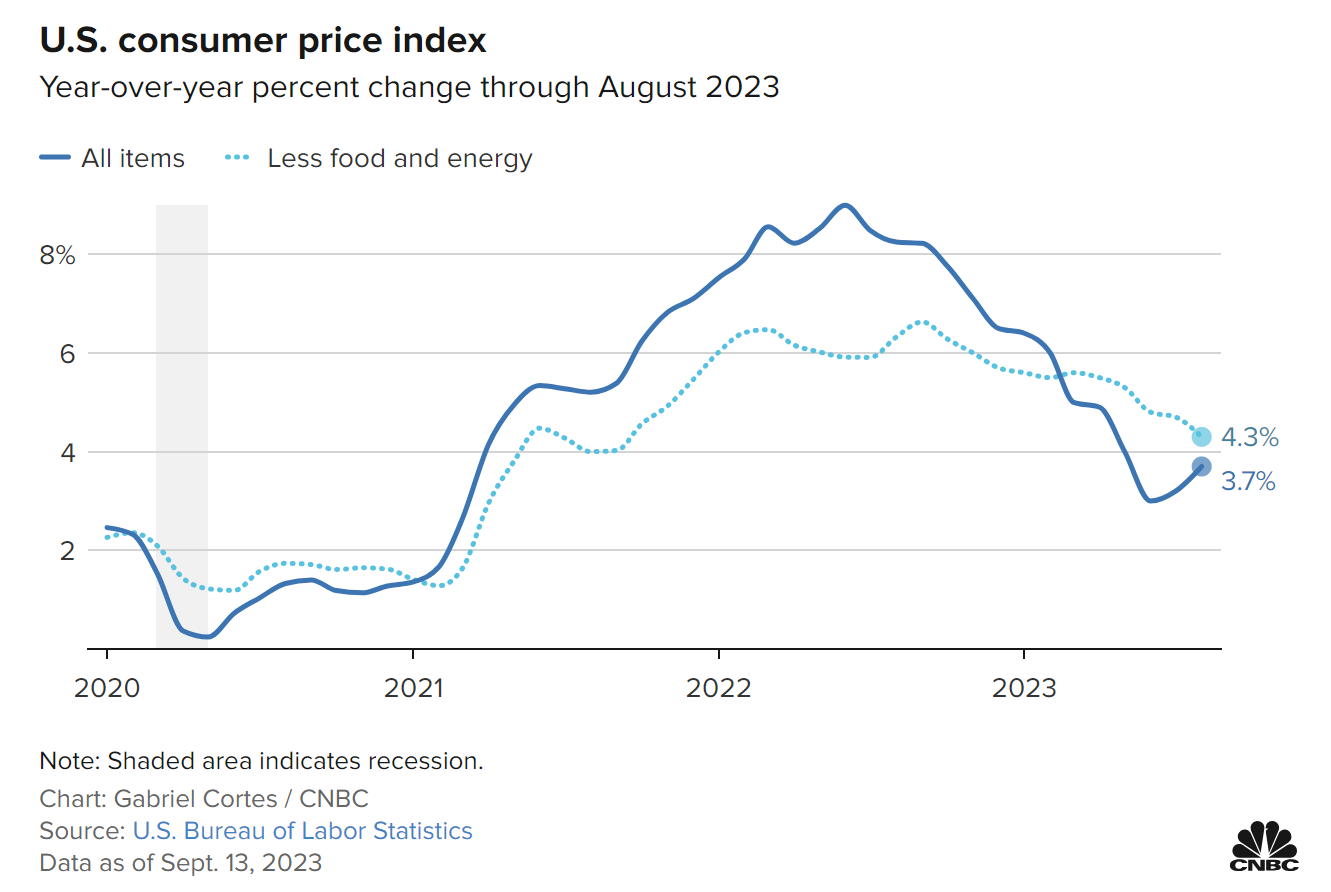

Core CPI Continued to Cool in August

Prices rose faster in August than over any other month this year. Consumer Price Index (CPI) data released Wednesday morning showed that headline inflation rose by 0.6 percent in August, an annual increase of 3.7 percent, a marked increase from the monthly increase of 0.2 percent in July, when prices rose 3.2 percent over the year prior.

The increase in headline CPI stemmed mainly from a 5.6 percent increase in energy prices over the month, including a 10.6 percent increase in the price of retail gasoline. The rise in gas prices was responsible for 34 percent of the overall increase in prices last month.

Source: CNBC

Core CPI, which excludes the more volatile food and energy prices, rose 0.3 percent during August. This increase in core CPI shows a slight increase from the 0.2 increases in core CPI seen in June and July. On an annual basis, core CPI rose by 4.3 percent, the smallest year-on-year increase since October 2021. Energy prices have been quite volatile over the course of the year and as core CPI, which continues to fall, may be a more reliable reflection of the path ahead for inflation, especially in the eyes of the Fed.

The August CPI figure is the final major data point on inflation to be released ahead of the Federal Open Market Committee (FOMC) meeting next Tuesday and Wednesday. The Federal Reserve again says that it will take a data-dependent approach in deciding its interest rate policy at this point in its lengthy effort to bring inflation down. The federal funds rate currently stands at 5.25-5.5 percent, following a 25 basis point increase at the Fed’s last meeting in July. Next week, the FOMC may pause on rate increases as it did in June; few expect an increase of the interest rate by 25 basis points, despite the increase in headline inflation in August.

Averting a Shutdown Faces Lengthening Odds

With the end of the 2022 fiscal year approaching quickly, Congress is making worryingly little progress toward averting a shutdown of the U.S. government on October 1. The fate of federal government funding lies in the hands of House GOP members, who spent three days quarreling this week in Washington and depends on their willingness to negotiate in the few remaining days of this fiscal year.

Intra-party negotiations nonetheless still continue in round-the-clock fashion, with House Republicans working to draft and pass a 30- to 60-day stopgap spending bill to avert a shutdown.

On the Senate side this week, Senate Republicans took a page from their House colleagues’ playbook. Senator Ron Johnson (R-WI) refused to allow a vote on amendments to the three-part bipartisan “minibus” legislation that got 85 votes to proceed. That bill would fund military construction and the Department of Veterans Affairs, the Department of Agriculture, the Department of Transportation and the Department of Housing and Urban Development. Senator Johnson insisted that the legislation be separated into three separate bills instead — a slower process than Congress has time to engage in to avoid a shutdown. The Senate adjourned yesterday and will return on Monday to continue its consideration of the minibus.

UAW Spot Strike Begins

At midnight, the United Auto Workers (UAW) union officially went on strike. Yesterday, the contracts of about 150,000 autoworkers at Ford Motors, General Motors, and Stellantis expired and negotiations on new labor contracts have yet to be resolved. The union has therefore decided to strike at one plant owned by each of the three companies for the first time in its history, instructing 13,000 workers to walk out:

- The G.M. plant in Wentzville, MO that makes the GMC Canyon and the Colorado

- The Stellantis complex in Toledo, OH that makes the Jeep Gladiator and Wrangler

- The Ford assembly plant in Wayne, MI, that makes the Bronco and the Ranger pickup

The length and extent of the strike could have broad effects on the U.S. auto market and the broader economy. While availability of new cars manufactured by the Big Three will not be immediately affected, a prolonged strike could lead to soaring car prices which could be reflected in inflation data.

Striking UAW members join thousands of workers in the entertainment industry who have been on the picket line since this summer. Writers belonging to the Writers Guild of America (WGA) have been on strike since May, and actors who belong to the SAG-AFTRA union joined them in July.

Hearings this Week

House Financial Services Discusses Basel Endgame Proposal

The House Financial Services Subcommittee on Financial Institutions and Monetary Policy convened on Thursday morning to discuss new capital rules proposed by federal regulators to govern the banking sector.

The subcommittee considered the 1,000-plus page proposal to implement stricter capital requirements on banks with $100 billion or more in assets to bring U.S. banks into compliance with Basel III requirements which was released by the Federal Reserve, Federal Deposit Insurance Corporation (FDIC), and Office of the Comptroller of Currency (OCC) in late July. Regulators’ proposal would update U.S. capital standards to better reflect:

- Credit risk

- Trading risk

- Operational risk

- Derivative risk

Additionally, the hearing discussed a separate proposal by the Fed to adjust the risk-based capital surcharges for globally systemically important bank holding companies (G-SIBs).

The hearing is timely, coming during the week of the 15th anniversary of the failure of Lehman Brothers, and just months after the failures of Silicon Valley Bank, Signature Bank, and First Republic Bank. The recent turmoil in the banking sector serves as a stark reminder that regulation must evolve to safeguard financial stability effectively. As Senior Policy Analyst at Americans for Financial Reform Alexa Philo stressed in her opening statement, “these proposals are essential to strengthening the banking industry’s ability to withstand stresses and shocks that can imperil banks’ financial viability, create uncertainty for depositors and customers, and negatively affect the economy.”

The hearing comes amid strong opposition to the proposals from banking industry groups and their Republican allies. On Tuesday, six banking industry groups sent a letter to the Fed, FDIC and OCC accusing them of violating the Administrative Procedure Act by not providing enough information to the public about their reasoning in determining details included in the final proposal regarding capital requirements. Republicans on the House Financial Services Committee sent their own letter to regulators on Tuesday, echoing the industry with a call for regulators to withdraw the proposal.

Subcommittee Ranking Member Bill Foster (D-IL) joined Subcommittee Andy Barr (R-KY) in highlighting the Fed’s less-than-forthcoming response to their letter. In early July, they wrote to Fed Vice Chair of Supervision Michael Barr requesting details of the Fed’s analysis and supporting data used in finalizing the proposed rule.

Comment periods for both proposals remain open until November 30.

Gensler Defends SEC Rules in Senate Banking

Securities and Exchange Commission (SEC) Chair Gary Gensler testified before the Senate Committee on Banking, Housing and Urban Affairs on Tuesday morning in a hearing largely focused on rules proposed by his agency.

Committee Republicans used the opportunity to continue their criticism of the agency, characterized by Committee Chair Sherrod Brown (D-OH) in his opening statement as “too many rules, too fast, too hard to comply with.”

The Committee’s questions focused on the rules proposed as well as those being finalized by the SEC, including the recently finalized private funds rule, which would require private equity firms to disclose:

- Certain fees and expenses

- Comparable performance data

- Independent audits

- Conflicts of interest by fund managers

The private funds rule is particularly important as the portion of the economy controlled by private equity continues to grow. Particularly concerning is increasing amounts of money state and local retirement systems commit to private-equity managers. From 2015 to 2022, North American pension fund private-equity allocation grew from 6.6 to 10.3 percent.

Republicans on the Committee also targeted the SEC’s delayed rule to require climate-related disclosures for public companies, grilling Gensler on the possibility that the rule would lead to an onerous compliance burden for farmers and small businesses. Gensler would not provide a timeline for the proposal of the final rule.

When faced with questions on digital assets, Gensler renewed his call for crypto-compliance and stressed that the cryptocurrency market is currently plagued by “wide-ranging noncompliance.” Gensler went as far as to say that the state of the current cryptocurrency industry is “reminiscent of what we had in the 1920s before the federal securities laws were put in place.”

Senate Banking Discusses Housing Supply

On Tuesday afternoon, the Senate Banking, Housing, and Urban Affairs Subcommittee on Housing and Community Development held a hearing on the nation’s housing shortage and innovations by communities and businesses that may be able to help alleviate the serious and worsening circumstances.

Subcommittee Chair Tina Smith (D-MN) described the extent of America’s housing shortage, highlighting that while 15.6 million households were formed from 2012 to 2022, only about 11.9 million housing units were created. While much of the regulation and legislation that impact the housing market are at the state and local levels, the hearing considered potential changes to federal policy. Dr. Jenny Schuetz, Senior Fellow at the Brookings Institution, highlighted that the federal government can provide essential support to state and local pro-housing innovations. These include directing the Department of Housing and Urban Development (HUD) to serve as a connector and facilitator between state and local policymakers and other stakeholders experimenting with pro-housing policies.

Subcommittee Ranking Member Cynthia Lummis (R-WY) discussed the innovative solutions private companies in her home state are using to stem the housing shortage that is increasingly creeping into rural areas.

Look Ahead

Tuesday, September 19th

- Federal Open Market Committee meeting (day 1)

- House Financial Services Committee Subcommittee on Capital Markets Hearing: Oversight of the SEC’s Division of Investment Management

- House Financial Services Committee Subcommittee on Financial Institutions and Monetary Policy Hearing: A Holistic Review of Regulators: Regulatory Overreach and Economic Consequences

Wednesday, September 20th

- Federal Open Market Committee meeting (day 2)

- Senate Committee on Banking, Housing, and Urban Affairs Subcommittee on Economic Policy Hearing: Child Care Since the Pandemic: Macroeconomic Impacts of Public Policy Measures