Update 446 — PPP Poked, Probed, Prodded:

How Many Paychecks Have Been Protected?

The administration’s $700 billion Paycheck Protection Program (PPP) represents the only federal effort to protect wages threatened by the Corona crisis. Congress enacted some tweaks to PPP last week that will save some small businesses but protect fewer paychecks. PPP can help some workers but offers no paycheck guarantees. Their firms must choose to apply for and succeed in securing loans.

Today’s Senate Small Business Committee hearing today affords a mid-course evaluation of the program: is it working? Is it too soon to tell? Are more fixes in order? Is any money left? Are there better ways to protect paychecks? Answers below…

Best,

Dana

—————-

Title I of the CARES Act created the Paycheck Protection Program (PPP) to provide short-term economic relief to small businesses. Immediately, the program was beset with challenges and waste. The original PPP funding — $349 billion — dried up in under two weeks. Congress has now poured nearly $700 billion into PPP in total.

Earlier today, the Senate Small Business Committee held a hearing on implementation of Title I of the CARES Act. Chair Rubio painted the program as a success, claiming that PPP supports the employment of about 50 million workers — more than 75 percent of the small business payroll in all 50 states — and has so far distributed $530 billion to 4.5 million companies (93 percent of all applicants).

But because detailed PPP data has not been released, Rubio’s claim is unverifiable and likely based on cherry-picked data. Numerous independent analyses show that funds are generally not flowing to the neediest businesses or those hardest hit by COVID-19. Per John Lettieri, president of the Economic Innovation Group, PPP “works better for least-affected employers and worse for the most affected, which is perverse.”

Below, we examine the problems surrounding the PPP and ways to fix them.

Numerous Program Design Flaws…

Before the program went into effect, the Treasury announced that lenders would be held liable for not thoroughly vetting applicants. As a result, much of the PPP funds went to established and thriving businesses with pre-existing relationships with their banks. PPP guidelines were designed to provide for flexibility: any business with fewer than 500 employees (per location) became eligible, and consequently, big companies like national restaurant chains could qualify. In total, publicly-traded firms have received more than $1 billion in funding.

Such large companies included Shake Shack and the Los Angeles Lakers, who both initially received PPP funds but returned their loans after a barrage of negative media. Some scandal-plagued companies received funds after settling suits with the Department of Justice. Others received funds after paying senior executives millions of dollars in compensation as they were laying off employees. Large companies with connections to Donald Trump received millions in government loans. And some firms, after receiving PPP funds, turned around and acquired rival firms. These companies were not the intended targets for PPP.

Meanwhile, struggling small businesses in need of loans were largely shut out. While firms with political connections received funds quickly, most small businesses had to wade through red tape and wait at the back of the first-come, first-serve queue.

…Coupled with Administration Malpractice

The Trump Administration’s ad hoc management of PPP has been borderline farcical. Trump and Secretary Mnuchin have issued (and backtracked on) unofficial guidelines and have threatened prosecutions, prompting confusion among loan recipients.

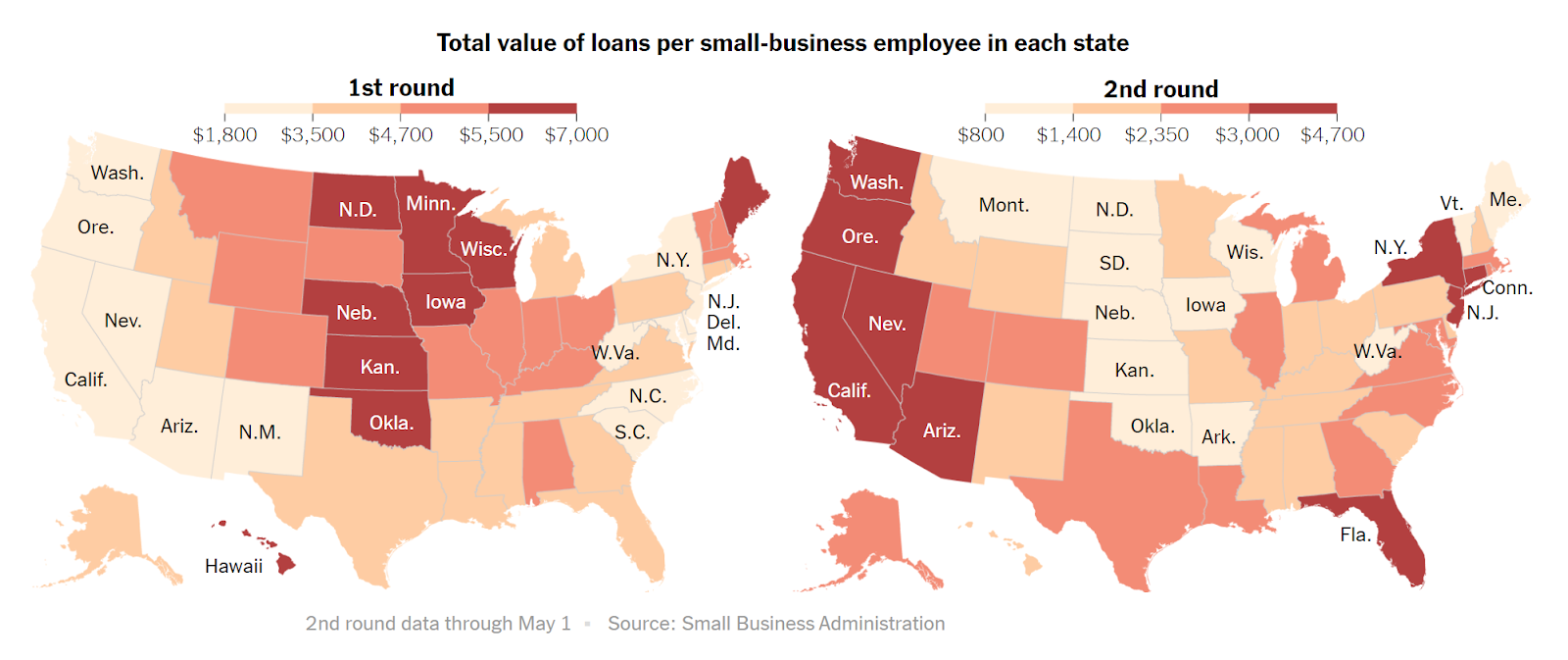

PPP loans are regionally discriminatory. Small businesses in central states like North Dakota, Colorado, Nebraska, and Kansas received much higher relief compared to those in harder hit states like New York and New Jersey. These regional disparities are even more evident when PPP loans are separated by tranche. During the first round of funds, small businesses in midwestern states received the greatest loans relative to the number of small business employees.

Source: New York Times

PPP Program Repairs to Date

Two PPP-related pieces of legislation have been enacted post-CARES Act:

- The Paycheck Protection Program and Health Care Enhancement Act authorized an additional $310 billion for PPP loans, including a $60 billion set-aside for smaller lenders, bringing the total to $659 billion.

- The Paycheck Protection Program Flexibility Act of 2020, which President Trump signed last Friday, gives PPP loan recipients more flexibility on the use of PPP funds and extends the life of the loan program through the end of the year. Before the law’s passage, employers could only use 25 percent on non-payroll expenses like rent and utilities and expect the loan to be forgiven; now that figure is 40 percent. Recipients of loans after June 5th now have five years to pay off non-forgivable loans, extended from the original two year requirement.

What Remains to Be Done?

The following fixes were under discussion and did not make the cut in the last round of PPP reforms:

- a carve out of funds for loans exclusively for businesses with less than $1 million in annual revenue;

- a carve out of funds for loans exclusively for businesses with fewer than 50 employees; and

- streamlining the application process for small businesses that do not have resources

A bipartisan group of legislators have pushed for additional funding to community development financial institutions (CDFIs). On May 28, Treasury announced a set aside of $30 billion for CDFIs along with Minority Depository Institutions and certified development companies. The HEROES Act, passed by the House almost a month ago, allocates an additional $1 billion to CDFIs. However, the CDFI Fund services relatively few lenders in niche, underserved markets, so it is unclear how many paychecks this adjustment would actually protect.

No matter how many fixes, set asides, and carve outs Democrats are able to incorporate into PPP, there will always be gaps and paychecks left unprotected.

A More Optimal Solution

Congress could transition from its current piecemeal, scattered approach to a more simple wage and credit continuity program. Under a comprehensive continuity approach to paychecks and firms, the SBA would no longer need to administer the loan application process because businesses would have their credit agreements restored to their status before the beginning of the crisis.

Wage continuity bills are gaining steam in both chambers of Congress.

- Although not included in the HEROES Act, Speaker Pelosi has praised Rep. Jayapal’s Paycheck Recovery Act, which would subsidize wages below $90,000 according to a company’s percentage of revenue lost and provide an additional sum to cover operating expenses.

- In the Senate, Sens. Sanders, Warner, Jones, and Blumenthal introduced the Paycheck Security Act, which similarly subsidizes wages and provides funds for other businesses expenses.

- Sens. Van Hollen, Warner, and Merkley introduced the Rebuilding Main Street Act, which would expand state workshare programs and allocate grants to businesses to cover a portion of operating costs.

Such an approach is administratively feasible and would drastically lower unemployment. Germany’s much-lauded Kurzarbeit wage subsidy program obviated the need for standing up PPP variants, and their unemployment rose less than 1 percent from March to April. Other European countries have adopted wage continuity programs, and the U.S. would do well to follow suit.

https://ponlinecialisk.com/ – generic cialis

Wonderful beat ! I wish to apprentice at the same time as you

amend your site, how can i subscribe for a weblog site?

The account helped me a appropriate deal. I have been tiny bit acquainted of this

your broadcast offered vibrant transparent idea 0mniartist asmr

I just could not go away your web site prior to suggesting

that I really loved the usual info an individual supply on your visitors?

Is gonna be back frequently to inspect new posts asmr 0mniartist

I constantly spent my half an hour to read this website’s articles or reviews daily along with a cup of coffee.

0mniartist asmr

What’s Taking place i’m new to this, I stumbled upon this I’ve found

It absolutely helpful and it has aided me out loads.

I am hoping to contribute & assist other users like its helped me.

Good job. 0mniartist asmr

It’s amazing for me to have a web site, which is good in support of my knowledge.

thanks admin asmr 0mniartist

local women dates

dating online

Hello, I think your site might be having browser compatibility issues.

When I look at your blog site in Opera, it looks fine but when opening in Internet Explorer,

it has some overlapping. I just wanted to give you a quick

heads up! Other then that, awesome blog!

This piece of writing will help the internet people

for setting up new web site or even a weblog from start to end.

I’ve been exploring for a little for any high-quality articles

or blog posts in this kind of area . Exploring in Yahoo I eventually stumbled upon this site.

Studying this information So i am happy to express that I’ve a very just right

uncanny feeling I found out just what I needed.

I most surely will make sure to do not disregard this web site and give it a look regularly.

Greetings! Very helpful advice in this particular article!

It is the little changes that produce the biggest changes.

Many thanks for sharing!

Nice post. I used to be checking constantly this weblog and I am

impressed! Extremely useful information particularly the

closing part 🙂 I handle such info much. I used to be looking

for this particular information for a very long time. Thank you

and best of luck.

Hey! I could have sworn I’ve been to this website before but after

browsing through some of the post I realized it’s new to me.

Anyways, I’m definitely delighted I found it and I’ll be bookmarking and checking back frequently!

hello there and thank you for your information – I’ve certainly picked up something new

from right here. I did however expertise some technical points using this site, as I experienced

to reload the web site many times previous to I could get

it to load correctly. I had been wondering if your web hosting is OK?

Not that I’m complaining, but sluggish loading instances times

will sometimes affect your placement in google and can damage

your high quality score if ads and marketing with Adwords.

Well I am adding this RSS to my e-mail and could look out for a lot more of your respective intriguing content.

Make sure you update this again soon.

Greate post. Keep writing such kind of information on your blog.

Im really impressed by your blog.

Hey there, You have performed an incredible job. I’ll definitely digg it

and for my part suggest to my friends. I am confident they will be benefited from this website.

Hi there very nice blog!! Man .. Excellent ..

Amazing .. I will bookmark your website and take the feeds also?

I am satisfied to seek out numerous useful information here in the publish, we’d like

work out extra techniques in this regard, thank you for sharing.

. . . . .

scoliosis

I am sure this post has touched all the internet people, its really really good

piece of writing on building up new web site.

scoliosis

scoliosis

It’s very trouble-free to find out any matter on net as compared to textbooks, as

I found this post at this website. scoliosis

scoliosis

Greetings from Los angeles! I’m bored at work so I decided

to browse your website on my iphone during lunch break. I enjoy the information you present here and can’t wait to take a look when I get

home. I’m amazed at how quick your blog loaded on my phone

.. I’m not even using WIFI, just 3G .. Anyhow, very good site!

scoliosis

free dating sites

Howdy! Do you know if they make any plugins to

safeguard against hackers? I’m kinda paranoid about losing

everything I’ve worked hard on. Any tips? https://785days.tumblr.com/ free dating sites

dating sites

It is the best time to make some plans for the long run and it is time

to be happy. I’ve read this put up and if I may I desire to suggest you few attention-grabbing things

or tips. Perhaps you could write next articles

referring to this article. I desire to read more things about it!

dating sites

I quite like reading through an article that can make men and

women think. Also, thanks for allowing me to comment!

Hey there this is somewhat of off topic but I was wondering if blogs use WYSIWYG editors or if you have to manually code with HTML. I’m starting a blog soon but have no coding experience so I wanted to get advice from someone with experience. Any help would be enormously appreciated!

Greetings from Carolina! I’m bored at work so I decided to check out your website on my iphone during lunch break.

I love the information you present here and can’t wait to take a look

when I get home. I’m amazed at how quick your blog loaded on my phone ..

I’m not even using WIFI, just 3G .. Anyhow, very good site!

Link exchange is nothing else but it is only placing the other person’s

web site link on your page at suitable place and other person will also

do similar for you.

What’s Taking place i am new to this, I stumbled upon this I have discovered It absolutely helpful and it has helped me out loads.

I hope to contribute & aid other users like its helped me.

Good job.

Wow, that’s what I was searching for, what a material!

present here at this weblog, thanks admin of this web page.

Hello there! This post could not be written any better!

Going through this post reminds me of my previous roommate!

He continually kept preaching about this. I am going to forward

this information to him. Fairly certain he’s going to have

a good read. Thank you for sharing!

Great beat ! I would like to apprentice at the same time

as you amend your web site, how can i subscribe for a blog site?

The account aided me a acceptable deal. I were

a little bit familiar of this your broadcast offered brilliant transparent idea

Howdy just wanted to give you a brief heads up and let you

know a few of the pictures aren’t loading properly.

I’m not sure why but I think its a linking issue.

I’ve tried it in two different web browsers and both show

the same results.

Hi there to all, the contents existing at this web site are in fact amazing for people knowledge, well, keep up the nice

work fellows.

Having read this I believed it was really enlightening.

I appreciate you taking the time and effort to put this short article together.

I once again find myself personally spending a significant

amount of time both reading and commenting. But so what, it was still worth it!

best price for generic cialis

cialis from india

Hi there, I read your blog daily. Your story-telling style

is witty, keep up the good work!

I cannot thank you enough for the article. Great.

I blog frequently and I genuinely appreciate your content.

This great article has really peaked my interest. I will book mark your website and keep checking for new details

about once a week. I subscribed to your RSS feed as well.

senior dating site

best online dating sites 2021

gay millionaire dating

older gay men dating sites

gay married men dating

It is not my first time to pay a quick visit this website, i am visiting this

web page dailly and obtain good data from here

all the time.

Pingback: how to calculate macros for keto diet

viagra connect walmart viagra single packs commercial ViagraCND100Mg – viagra users comments

Appreciate this post. Will try it out.

gay dating vancouver

snapchat gay dating site ads

married and gay dating

Wow, this post is good, my sister is analyzing such things,

thus I am going to convey her.

gay older dating

“sereen” “gay dating”

gaywatch gay dating site