Update 514 – Housing Shortage in the US:

Problems, Solutions, and Odds of Reform

The pandemic and its ensuing economic crisis have brought manifold housing challenges to the fore for both renters and owners. The rent remains too high and homeownership still beyond the means of too many people. The consensus view: the housing stock of the nation needs to be increased as it serves as a cornerstone for the economy at-large.

Generally, the federal government isn’t looked to for solutions to housing issues — the programs that do exist are a mere speck on the overall budget. And while most of the programs that do exist are aimed at low-income Americans, other options, like the mortgage interest deduction, aim to help those that are already financially stable. The Federal Government’s housing priorities are off-kilter but we now have an opportunity to do something about it.

Below we examine the current housing crisis and policy to address the crisis in the short- and long-term.

Best,

Dana

————–

Yesterday, the Senate Banking Committee hosted its first hearing on the state of housing in almost nine years. The hearing focused on a range of issues but homed in on addressing the current affordability crisis, rooted in a chronic supply issue. Restrictive zoning laws at the state and local level, underfunding of public housing at the federal level, and market factors have reduced the supply of affordable homes, especially for low-income families.

The Affordability Crisis

The housing market has led the ongoing economic recovery, as record-low mortgage rates and a desire for more space pushed more Americans to buy homes. Between 2020 and 2021, home prices increased by roughly 10 percent, with prices increasing most for the market’s lower-end. But while the housing market reaches new heights during the pandemic, renters and homeowners are in a perilous position. Nearly one in five renters is behind on rent and over 10 million homeowners are behind on mortgage payments.

Even before the pandemic, the country faced an affordable housing crisis, impacting every community in the country. The roots of this crisis date back to 2008, when many homebuilders went out of business. Those that survived shifted focus to higher-cost housing, where more money could be made. This shift has resulted in a shrinking stock of affordable housing. Lack of supply means higher prices for renters and home-buyers alike, widening the gap between what most people earn and current housing costs.

The effects of the affordability crisis are seen most clearly in homeownership levels and the price of rent.

- Homeownership: Homeownership remains the most common avenue for low- and moderate-income families to build wealth, but rates among adults below 50 are five percentage points lower today than in the early 1990s. At yesterday’s hearing, Sen. Smith (MN) noted the persistent and increasing disparities in homeownership opportunities for people of color. The Pew Research Center found that 75 percent of white Americans owned a home, compared to 50 percent of Hispanic Americans, 46 percent of black Americans, and 61 percent of Asian Americans.

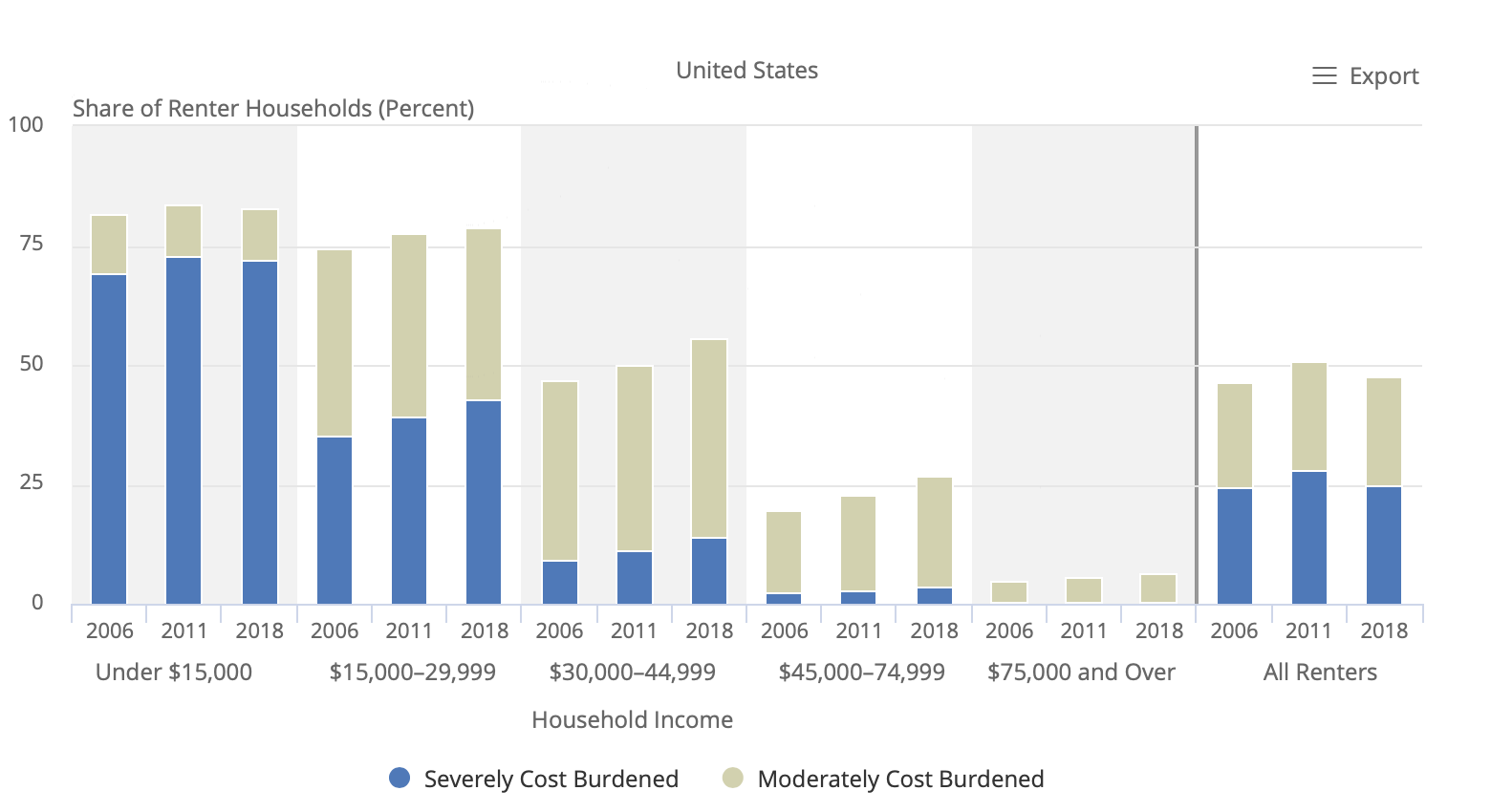

- Rent: Rent prices increased by roughly 20 percent between 2000 and 2019. Higher prices and a lack of new, affordable homes have resulted in a growing share of renters who are cost-burdened or spending more than 30 percent of their household incomes on housing. In 2019, roughly 46 percent of all renters were cost-burdened, while 24 percent were severely cost-burdened (spending more than 50 percent on housing) per the Joint Center for Housing Studies. While this is particularly impactful for renters making less than the federal poverty rate, affordability issues are not just unique to low-income renters.

Rent Cost Burden by Household Income from 2006–2018

Source: JCHS tabulations of US Census Bureau, American Community Survey 1-Year Estimates.

Pandemic Issues/Short-Term Solutions

A series of executive actions and the recently-passed American Rescue Plan (ARP) go a long way toward supporting renters and homeowners. At the start of his presidency, Biden issued executive actions to extend the federal eviction moratorium, the foreclosure moratorium for homeowners, and the mortgage payment forbearance program. These actions temporarily prevented millions from potentially losing their homes.

The ARP contains billions in housing-related aid. Unlike past relief packages that contained only housing protections with indirect assistance, the ARP provides direct homeowner and rent relief. Some notable provisions include, in order of amount of assistance:

- $21.6 billion for emergency rental aid

- $9.9 billion to the Homeowners Assistance Fund, which helps homeowners in need pay overdue mortgage bills, taxes, insurance, and HOA dues

- $5 billion for fighting homelessness (through the HOME Investment Partnerships Program)

- $5 billion for emergency housing vouchers

- $4.5 billion for homeowners and renters to pay for heating and cooling costs

- $750 million for housing needs in Native American communities

- $139 million for rural housing

- $120 million for housing counseling

ARP assistance is well-targeted, taking into account household income and employment status. But Sen. Menendez observed yesterday that these actions alone may not prevent struggling families from losing their homes. The CARES Act, coupled with actions taken by FHA, FHFA, and Fannie and Freddie Mac, has provided many homeowners a lifeline, yet an estimated 1.8 million mortgages will be seriously delinquent when foreclosure moratoriums on government-backed loans finally begin to lift. The ARP’s Homeowner Assistance Fund was set up to help those in this situation, but the $9.9 billion fund may not be enough.

Affordability Crisis/Long-term Solutions

Beyond the pandemic, the administration faces a much longer-term affordability crisis rooted in a shortage of affordable housing stock. Sen. Warren focused on the supply-side issue at the hearing yesterday. Responding to Sen. Warren, Diane Yentel of the National Low Income Housing Coalition (NLIHC) noted that for every ten low-income households, there are fewer than four available and affordable units. Per Yentel, the current shortage of affordable homes, especially rental homes, is caused by persistent market failure, outdated zoning laws, and chronic underfunding of solutions.

The private market alone cannot solve the crisis, and government intervention is necessary to ensure decent homes are available and affordable for lower-income individuals. Yesterday, witnesses and lawmakers discussed legislative solutions to the current crisis that directly address supply, including:

- Housing Trust Fund (HTF): Congress consistently underfunds housing subsidies, resulting in only one in four households eligible for and in need of assistance receiving any. To expand the affordable housing stock, Congress could increase funding to the national HTF, which provides affordable housing construction, preservation, and operation grants to states. Warren’s Housing and Economic Mobility Act, introduced in the 116th Congress, would fully fund the HTF at $44.5 billion, allowing states and cities to invest in affordable housing for low-income renters.

- Existing Public Housing: The NLIHC estimates that roughly 10-15 thousand public housing apartments are lost each year due to obsolescence or decay. The total funding needed to address capital repairs in public housing is around $70 billion today. Rep. Velazquez’s Public Housing Emergency Response Act from the 116th Congress provides a path to preserving existing public housing by investing $70 billion to eliminate the public housing capital needs backlog and ensure public housing is safe and affordable.

- Low Income Housing Tax Credit (LIHTC): Expanding the LIHTC is another way to empower states and territorial governments to expand affordable housing by subsidizing the construction, rehabilitation, and acquisition of affordable rental housing through tax credits. Last year, Sens. Wyden and Cantwell put forward legislation to strengthen LIHTC and support construction of 500,000 additional affordable housing units.

- Local and State Housing Regulations: While deregulation alone is not a successful strategy for increasing affordable housing, a significant barrier is local restrictions. For any new federal investments and grants, states and localities must be required to eliminate some local restrictions that reduce affordable housing availability.

On the campaign trail, President Biden developed a $600 billion housing plan that focused, in part, on increasing the overall supply of affordable housing. With the $1.9 trillion COVID relief package finally passed, Biden has the opportunity to enact this plan in the anticipated infrastructure bill later this year. In this next package, Democrats have indicated that they will prioritize non-traditional infrastructure such as affordable housing in addition to traditional infrastructure. Proposals that address affordable housing stock such as the ones above will be critical “building back better” at the end of this crisis.

http://fcialisj.com/ – buy generic cialis online

http://vsdoxycyclinev.com/ – doxycycline 100mg acne

well post, i like it

Good web site! I really love how it is easy on my eyes and the data are well written. I am wondering how I could be notified when a new post has been made. I’ve subscribed to your RSS which must do the trick! Have a nice day!

This is a great tip particularly to those new to the blogosphere.

Brief but very accurate info… Thank you for sharing this one.

A must read article! asmr 0mniartist

whoah this weblog is fantastic i like studying your articles. Keep up the great work! You know, lots of people are looking round for this information, you could help them greatly.

Outstanding post, you have pointed out some good details , I as well conceive this s a very good website.

This article presents clear idea designed for the new visitors of blogging,

that actually how to do blogging. asmr 0mniartist

I constantly spent my half an hour to read this weblog’s posts all the time along with a cup of coffee.

asmr 0mniartist

Hi, I check your blog regularly. Your story-telling style is witty, keep doing what you’re doing!

asmr 0mniartist

meet singles online

chat websites to meet people

milfs dating.com

senior women for sex

greate website~Hello, Neat post. There is a problem together with your web site in internet explorer, could test this¡K IE still is the marketplace chief and a big portion of people will omit your magnificent writing due to this problem.

Hello good luck~The site and data is excellent and enlightening in addition

Hello fantastic luck~You might have built some actually great factors there..

Asking questions are actually good thing

if you are not understanding anything entirely, however this post provides good understanding even.

Nice blog here! Additionally your web site rather a lot up very fast!

What host are you the usage of? Can I get your associate hyperlink for your host?

I desire my site loaded up as fast as yours lol

Thanks for finally talking about > Housing Shortage

in the US < Loved it!

Paragraph writing is also a excitement, if you be acquainted with afterward you can write if not

it is difficult to write.

tider , tinder date

tinder online

tinder sign up , tinder dating app

tinder online

Having read this I believed it was very

enlightening. I appreciate you finding the time and effort to put

this short article together. I once again find myself spending a

significant amount of time both reading and leaving comments.

But so what, it was still worth it!

Hi, just wanted to mention, I liked this blog post. It was helpful.

Keep on posting!

Hello superior luck~I’m nonetheless learning from you, when I’m enhancing myself. I undoubtedly take pleasure in looking at all the things that is written on your internet site.Continue to keep the posts coming. I beloved it!

I would really like you to become a guest poster on my blog

hellow~ you good post~Excellent blog here! Additionally your website quite a bit up fast! What host are you the use of? Can I am getting your affiliate hyperlink on your host? I desire my website loaded up as quickly as yours lol

Fantastic website you have here but I was curious

about if you knew of any forums that cover the same topics discussed in this

article? I’d really love to be a part of group where I can get feed-back from other experienced people that share the same interest.

If you have any suggestions, please let me know. Many thanks!

I just could not leave your site prior to suggesting that I actually loved the

standard info an individual supply on your guests? Is going to be back incessantly to inspect new posts

It’s really a great and useful piece of information. I’m glad that you shared this useful info with us. Please keep us up to date like this. Thanks for sharing.

My brother suggested I may like this blog.

He was once entirely right. This submit truly made my day.

You cann’t consider just how much time I had spent for this

info! Thank you!

how to use tinder , browse tinder for free

what is tinder

how to use tinder , what is tinder

tinder app

cheapest cialis

generic name for cialis

tinder date , tindr

http://tinderentrar.com/

scoliosis

Hi there, I log on to your blog regularly. Your writing style is awesome,

keep doing what you’re doing! scoliosis

I got what you intend,saved to favorites, very nice site.

scoliosis

Good day I am so thrilled I found your site, I really found you by accident, while I was browsing on Google for

something else, Nonetheless I am here now and would just like to say

cheers for a remarkable post and a all round thrilling blog (I

also love the theme/design), I don’t have time to

read it all at the minute but I have saved it and also added your RSS

feeds, so when I have time I will be back to read a great

deal more, Please do keep up the great job. scoliosis

scoliosis

No matter if some one searches for his essential thing,

thus he/she wishes to be available that in detail, therefore that thing is maintained

over here. scoliosis

free dating sites

I’m not sure why but this website is loading very slow for me.

Is anyone else having this problem or is it a issue on my end?

I’ll check back later on and see if the problem still exists.

https://785days.tumblr.com/ free dating sites

dating sites

Does your website have a contact page? I’m having a tough time locating

it but, I’d like to shoot you an e-mail. I’ve got some ideas for your blog

you might be interested in hearing. Either way, great blog

and I look forward to seeing it expand over time. free dating sites

Hmm it seems like your website ate my first comment

(it was super long) so I guess I’ll just sum it up what I had

written and say, I’m thoroughly enjoying your blog. I as well am an aspiring blog writer but I’m still new to the whole thing.

Do you have any recommendations for rookie blog writers?

I’d genuinely appreciate it.

Howdy! Do you know if they make any plugins to protect against hackers? I’m kinda paranoid about losing everything I’ve worked hard on. Any suggestions?

you have got a excellent weblog here! should you develop invite posts on my own

http://abiturient.ru/bitrix/rk.php?id=76&goto=https://www.mt-tapa114.com/

Appreciating the time and energy you put into your website and detailed information you present.

It’s awesome to come across a blog every once in a while that isn’t the same out of date rehashed material.

Excellent read! I’ve saved your site and I’m adding

your RSS feeds to my Google account.

Its not my first time to go to see this website, i am browsing this

website dailly and obtain good data from here everyday.

Everything is very open with a very clear description of the challenges.

It was really informative. Your website is very helpful.

Thank you for sharing!

It’s perfect time to make a few plans for the longer term and it’s time to be happy.

I’ve learn this publish and if I may just I want

to recommend you some fascinating issues or suggestions.

Maybe you could write subsequent articles referring to this article.

I desire to learn even more issues about it!

My spouse and I stumbled over here different web address and thought I might check things out.

I like what I see so now i’m following you. Look forward to checking out

your web page again.

Very nice post. I just stumbled upon your blog and wished to

say that I have really enjoyed surfing around your blog posts.

After all I’ll be subscribing to your feed and I hope you write again soon!

It’s awesome in support of me to have a site, which is valuable designed for my

knowledge. thanks admin

Hi there! This is my first visit to your blog! We are a group of volunteers and starting a new initiative in a community in the same niche.

Your blog provided us useful information to work on. You have done a outstanding

job!

It’s going to be ending of mine day, however before end I am reading this great piece

of writing to improve my know-how.

generic viagra website reviews

generic kamagra

buy cialis 5mg online

cialis tablets for sale

prednisone over counter in costa rica

on line kamagra

free samples viagra

This website online can be a stroll-by way of for all the info you needed about this and didn’t know who to ask. Glimpse right here, and also you’ll definitely uncover it.

cheapest place to buy cialis

tadalafil and dapoxetine

comprare cialis online

finasteride

Im thankful for the blog post.Really looking forward to read more. Cool.

Eksqqt – erectile dysfunction exercises Afefzk

Hmm it seems like your blog ate my first comment (it was extremely long) so I guess I’ll just sum it up what I submitted and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog writer but I’m still new to

the whole thing. Do you have any suggestions for inexperienced blog writers?

I’d genuinely appreciate it.

Fascinating blog! Is your theme custom made or did you download it from somewhere?

A design like yours with a few simple adjustements would really make my blog shine.

Please let me know where you got your design. Many thanks

I think this is among the most important info for me. And i am glad reading your article.

But want to remark on few general things, The website style

is ideal, the articles is really nice : D.

Good job, cheers

It’s actually a great and useful piece of information. I

am satisfied that you shared this helpful info with us. Please stay us up to date like this.

Thank you for sharing.

Saved as a favorite, I like your web site!

I will right away clutch your rss as I can not find your email subscription link or newsletter service.

Do you have any? Kindly allow me recognize so that

I may just subscribe. Thanks.

Can you tell us more about this? I’d love to find out

more details.

excellent points altogether, you just won a new reader.

What could you suggest about your post that you made some days in the

past? Any positive?

You could certainly see your enthusiasm in the work

you write. The sector hopes for more passionate writers like you who are not afraid to say how they believe.

All the time go after your heart.

This web site really has all of the information and facts I wanted concerning this subject and didn’t know who

to ask.

You really make it seem so easy with your presentation but I find this topic to be really something which I think I would never understand.

It seems too complicated and extremely broad for me.

I am looking forward for your next post,

I’ll try to get the hang of it!

You completed certain fine points there. I did a search on the theme and found mainly people will agree with your blog.

yogasana marathi book pdf Cpasbien Torrent book of circus serie en francais

Hi there, I found your blog via Google at the same time as searching for a related subject, your

site came up, it appears good. I’ve bookmarked it in my google bookmarks.

Hi there, just became aware of your blog thru Google, and found that it’s truly informative.

I’m going to watch out for brussels. I will be grateful if you proceed this in future.

Numerous people will be benefited from your writing. Cheers!

Everyone loves what you guys are up too. This type of clever work

and coverage! Keep up the excellent works guys I’ve included you guys to my own blogroll.

Excellent article. Keep writing such kind of information on your site.

Im really impressed by it.

Hey there, You have done a great job. I will definitely digg it and individually recommend to my friends.

I’m confident they’ll be benefited from this website.

hey there and thank you for your information – I’ve definitely

picked up anything new from right here. I did however expertise a few technical points using this site, since I experienced

to reload the site many times previous to I could get it

to load correctly. I had been wondering if your web host is OK?

Not that I’m complaining, but slow loading instances times will very frequently affect

your placement in google and could damage your quality score if ads and marketing with Adwords.

Well I’m adding this RSS to my e-mail and could look out for much more of your respective intriguing content.

Ensure that you update this again very soon.

Sony Xperia M2 Sim Slot Repair Objet Cach Sur Casino Max Casino C R Ale Merveille Chocolat

Very energetic post, I loved that bit. Will there be a part 2?

Etkileşimi Arttırmak İçin Takipçi ve Beğeni Satın Almalısınız

Özellikle yeni açılan sosyal medya hesaplarının en büyük sorunları arasında takipçi sayısının düşüklüğü ve paylaşımlarda etkileşim olmamasıdır.

Beğeni ve yorumların gelmesi sosyal medya hesaplarının gelişimine katkı sağlamaktadır.

Özellikle çok takipçisi bulunan ve paylaşımları beğenilerek yorum yapılan hesaplar

ilgi çekmektedir. Takipçi Satın Al işlemleri sayesinde hızlı bir etkileşim sağlanabilmektedir.

Ancak tüm hizmetlerde olduğu gibi bu hizmetlerinde

farklı seçenekleri bulunmaktadır.

https://rebrand.ly/takipci-satin-al

I am regular visitor, how are you everybody? This paragraph posted

at this web page is actually good.

Jackpot Euromillions My Million Happesmoke Casino Jas De Bouffan Casino Vic Sur Cere The Dansant Le 20 10 2019

Thank you a bunch for sharing this with all of us you

actually recognise what you are speaking about! Bookmarked.

Please also discuss with my site =). We will have a hyperlink

exchange arrangement between us

I was extremely pleased to uncover this web site. I want to to thank you for

ones time for this particularly fantastic read!! I definitely appreciated

every part of it and I have you bookmarked to look at new stuff on your blog.

You are my aspiration, I possess few web logs and infrequently run out from to post .

buy real cialis online

mustang viagra viagra with dapoxetine overnight delivery ViagraCND100Mg – generic viagra supplier india

over the counter viagra for sale in ireland how long does it take viagra to work rzwjtai – lowcost viagra

Wow, amazing blog layout! How long have you been blogging for?

you make blogging look easy. The overall look of your site is excellent, as well as the content!

When someone writes an article he/she retains the idea of a user in his/her brain that how a user can know it.

So that’s why this paragraph is perfect. Thanks!