Update 745 — Hope for Tax Package

Amid Unresolved FY24 Budget Issues

The congressional budget-making process for fiscal year 2024 (FY24), now in its fourth month with no plan in place, seems to have two gears: slow and reverse. This week, the GOP added a set of border security demands to the negotiations, complicating that process. The first of two government funding deadlines is two weeks away, the border demands raising the odds of a partial shutdown without agreement by January 19.

But out of the spotlight, a consensus has emerged on a tax package that has its own deadline of January 23 if the package’s provisions are to apply to 2023 tax filings. The roughly $100 billion package pairs corporate tax provisions with a three-year expansion of the current Child Tax Credit (CTC). Today, we look at the package and the ray of hope it represents for the nation’s neediest children if it can be adopted in the January 19 funding tranche.

Good weekends, all…

Best,

Dana

Against the odds, Congress appears to be nearing agreement on a tax package of corporate tax provisions and a three-year expansion of the Child Tax Credit (CTC). Efforts to address these priorities failed at the end of 2022 but have new life today, setting up the perfect opportunity for a strong bipartisan package.

While work on this package has been ongoing behind the scenes for the past few months, it still risks being crowded out by the funding issues challenging Congress’ bandwidth. Members are up against a tight timetable to pass a tax package that can be applied to 2023 tax returns, and so are looking to the January 19 CR deadline as a legislative vehicle. During these busy weeks of negotiation and action, funding resources for the millions of children and families struggling with the rising cost of living must remain a priority.

The Evolution of the Child Tax Credit

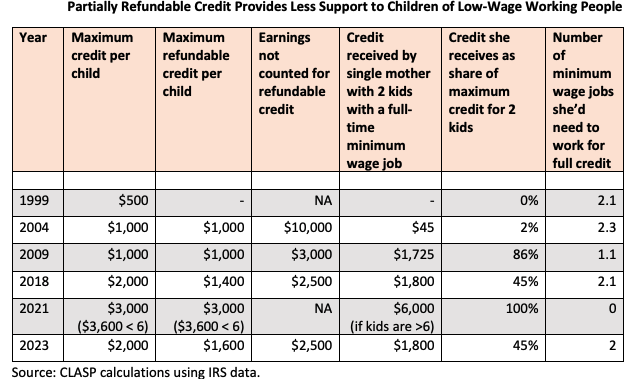

The Taxpayer Relief Act of 1997 first enacted the CTC with overwhelming bipartisan support. In the credit’s original form, families received $400, which increased to $500 in 1999 and was primarily non-refundable, meaning families could not claim the full amount if their federal tax liability was lower than the value of the credit. In the following decade, lawmakers adjusted the credit periodically to reach more families and children. In 2001, President George W. Bush passed legislation that made the credit partially refundable for the first time.

In response to the 2007-2009 financial crisis, the credit’s earnings threshold was lowered until 2012, falling to $3,000. Then, in 2017, the Tax Cuts and Jobs Act (TCJA) temporarily doubled the maximum credit to $2,000 and provided a non-refundable $500 for families who did not qualify for the $2,000 credit. These changes primarily benefited middle and upper-income families. The Center for Law and Social Policy (CLASP) used IRS data to summarize the evolution of the CTC in the figure below:

Source: CLASP

The Child Tax Credit received its most sweeping expansion in 2021 as a part of the American Rescue Plan Act. In response to the COVID-19 pandemic, the government announced the following changes to the CTC:

- The credit became fully refundable for the first time in its history.

- The maximum amount available increased to:

- $3,600 per child between 0-6

- $3,000 per child between 6-17.

- The credit expanded to include 17-year-olds.

- The credit was circulated on a monthly basis, instead of when families file their taxes.

This expansion, the largest in the credit’s history, resulted in record-breaking reductions in child poverty. The U.S. Census Bureau reported that child poverty, measured by the Supplemental Poverty Measure, fell to its lowest recorded level from 9.7 to 5.2 percent in 2021, lifting 2.9 million children out of poverty. While fully reinstating the CTC will require bipartisan compromise, data proves that expanding the CTC for families who need it most is the most effective way to reduce child poverty and help families cope with inflation.

Gaining Steam in the Push for a Package

Tax cuts are often only a short-term means of addressing a current need or avoiding heightened costs associated with permanent legislation. Lawmakers have traditionally renewed these expiring provisions through legislation collectively referred to as “tax extenders,” before breaking for the winter holiday recess.

Extenders have proliferated in recent years due to the sweeping effects of the 2017 TCJA championed by former President Trump. But efforts to pass tax extenders and associated changes to tax policy have failed the past two years, leaving key tax priorities on both sides of the aisle unaddressed.

In 2021, the tax extenders negotiation included additional efforts to ensure that two business tax provisions intended to offset the cost of the TCJA would not take effect in 2022:

- Limits on business deductions for interest expense

- Amortization requirements for the deduction of research and experimentation (R&E) costs

Failure to pass a tax package at the end of 2021 led to their implementation, increasing tax liabilities for many businesses. In 2022, the Build Back Better Act did not include legislation for business taxes or the CTC, and Congress also failed to pass tax extenders in December 2022. This was especially notable as a third major TCJA business provision, 100 percent bonus depreciation, began its phase-out at the beginning of 2023.

The inability to pass tax policy addressing interest deductions, amortization requirements, bonus depreciation, and the CTC in previous years has increased pressure surrounding a tax package that would take effect for the 2023 tax year. Conservatives are eager to further cut taxes for businesses, while progressives continue to fight for the benefits that an expanded CTC offers children and families.

Tax Package Pairs CTC with Business Provisions

Lawmakers have been working on a tax package to address business tax provisions in exchange for an expansion of the CTC – key priorities they have failed to pass for the last few years. The projected total cost is roughly $100 billion through 2025, split evenly between the CTC and business priorities. Although an official deal is still pending, the main components of the package likely stay the same (changes will extend through the end of 2025, in line with the expiration of other major TCJA provisions):

- Extension of 100 percent bonus depreciation ($3 billion cost)

The TCJA increased bonus depreciation from 50 percent to 100 percent, allowing businesses to deduct the full cost of property (usually equipment or software) in the first year of use. The 100 percent deduction began its phase-out in 2022 and will decrease by 20 percent each year until it reaches zero percent in 2027.

- Reinstatement of R&E expensing ($25 billion cost)

The TCJA changed tax policies that allow immediate expensing of research and experimentation (R&E) costs. As of 2022, firms must instead amortize expenses over a 5-year (domestic research) or 15-year (international research) period. This change marks the first time companies cannot immediately deduct R&E expenses since 1954.

- Delay of tighter interest deductibility limit ($19 billion)

The TCJA changed the calculation used to determine interest deductibility, which has resulted in increased tax liabilities for many businesses.

- Expansion of the CTC (~$50 billion, est.)

Money for the CTC will be 1:1 with the cost of the three business tax provisions above. Specifics of the CTC’s structure are not yet final, but CTC proponents are prioritizing changes to the refundability structure to ensure more families have access to the credit.

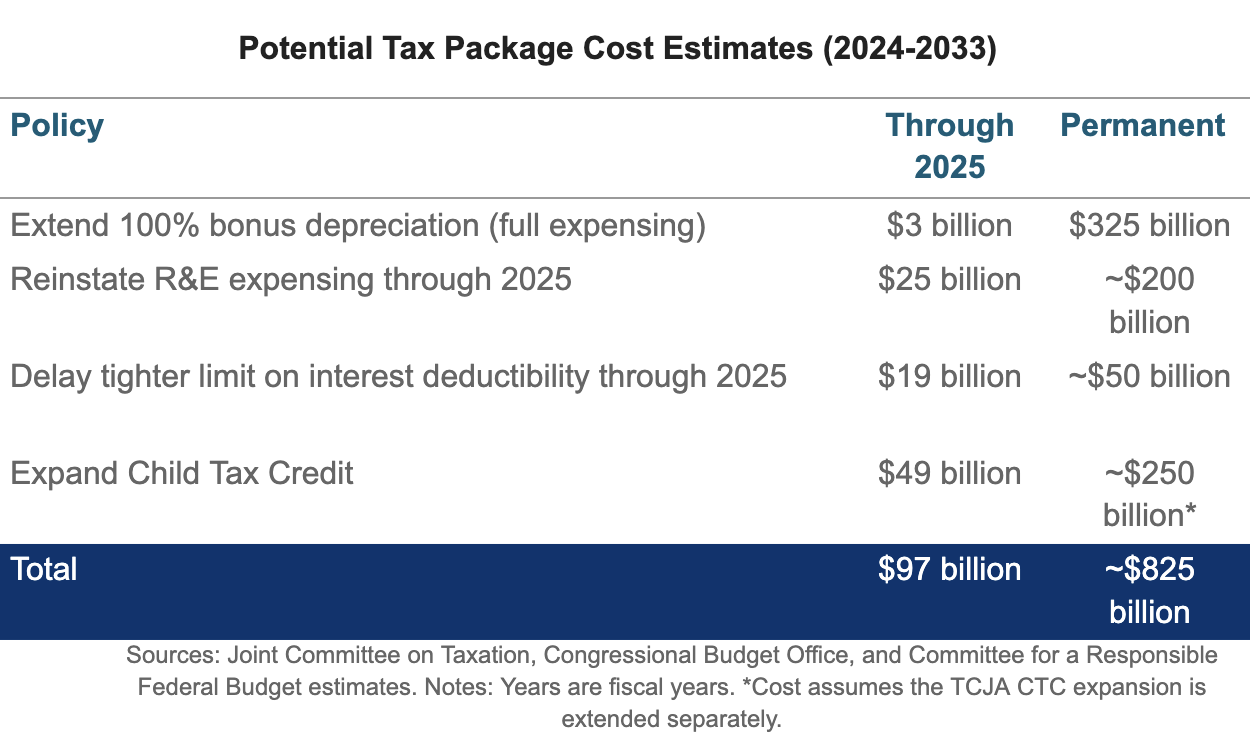

The Committee for a Responsible Federal Budget (CRFB) created a table showing full cost estimates of the tax package:

Source: CRFB

Despite its price tag of $100 billion through 2025, no offsets are expected to be included in the package. This omission has not seemingly impacted the deal’s political viability due to the relatively short time frame and careful bipartisan balance. It is important to note that if these policies are made permanent in 2025, the cost of the business provisions will be much greater than the CTC investment (depicted in the far right column above).

There is also broad bipartisan support for the inclusion of provisions related to the Low Income Housing Tax Credit (LIHTC), a priority that has been looking for a legislative vehicle. As the LIHTC provides funds to developers who create housing opportunities for low-income Americans as opposed to directly provisioning additional income to families in need, it will be crucial to ensure that any effort to extend the LIHTC does not upset the equal balance between the cost of business provisions and the CTC.

Available Vehicle: January 19 Appropriations Bill

While the components of the tax package may have been largely agreed upon, they need to be attached to must-pass legislation to receive timely consideration. Speaker Johnson has expressed support for the tax package but hasn’t committed to adding legislation to appropriations bills that are likely to be fragile given the complexity of the negotiation process thus far. It remains to be seen whether or not the tax package will be made a significant legislative priority in the coming weeks. It will likely need to be addressed under the January 19 CR deadline for changes to be reflected on 2023 tax returns.

The IRS has not released a final cutoff date for implementing policy changes on 2023 tax returns, though the 2023 filing season begins on January 23. To make matters more complicated, Republicans in the House and Senate have recently shifted their efforts to enact long-lasting immigration reform to the first tranche of appropriations bills for which the CR is expiring on January 19. Congress has yet to agree on a topline funding number, and the tax package may be in danger of being crowded out of the necessary vehicles that would allow changes to apply for the 2023 tax year.

Progressive Priorities for the CTC

The draft tax package aims to expand the CTC and reinstate business provisions with fiscal dollar parity to secure bipartisan support. But components of the CTC expansion must prioritize expanding the reach of funding to those families who would be most impacted.

Expanding the CTC to children at the lowest income levels could be ensured by an expansion in refundability. Making the credit fully available to all low-income children is the most efficient way for the deal to reach children who need it most. The Center on Budget and Policy Priorities estimates removing the refundability cap would lift around 1.5 million children out of poverty. It would finally provide the full $2,000 credit to the 19 million children who are left out of the full credit because their parents do not earn enough. While some have proposed raising the credit amount, without addressing the income requirements, such a move would help middle to upper-income families. The progressive priority must ensure those most in need are reached in this deal.

Adjusting phase-in requirements to reach more families could also expand the credit to include the lowest-income families. The current credit requires families to earn $2,500, and then the credit phases in at 15 percent for any earnings above this base. As it currently stands, ITEP reports that one in three children are left out of the credit. It disproportionately excludes Black and Hispanic children as well as children who live in rural areas.

20/20 Vision urges Congress to ensure that changes to the CTC address the needs of as many families and children in poverty as possible. The three business provisions expected in the tax package represent a considerable concession, and lawmakers must reject a deal if the benefits are primarily focused on middle and upper-income families as opposed to those with the most need.