Update 538 — Corporate Tax Reform:

ProPublica Analysis Applied to Firms

ProPublica’s explosive report this month detailed nonpayment of federal taxes by high-profile, high-net worth figures such Jeff Bezos, Elon Musk, and Michael Bloomberg. But the revenue loss from their nonpayment due to legal evasions is a drop in the bucket compared to the loss when big firms pay no taxes. The report leaves in its wake increasing demands and political support in Congress for both individual and corporate tax reform.

Democrats are pressing the White House to stick with its corporate tax reforms to finance spending. The G7 has come to an agreement on overhauling international tax laws. President Biden has the opportunity to reform corporate taxation in the U.S but first must prevail through the difficult Congressional negotiations ahead.

Below, we discuss the salient and viable options for reform, focusing on the Biden administration’s proposals.

Best,

Dana

————–

Current State of Corporate Taxes

Until recently, cutting corporate taxes has been a bipartisan affair. Both parties sought to reduce reliance on corporate tax revenue and attract investment from multinational companies. The 2017 Tax Cuts and Jobs Act (TCJA), passed along partisan lines, cut corporate taxes significantly. To understand the fiscal impact, magnitude, and revenue potential of President Biden’s corporate tax proposals, modern history provides useful context.

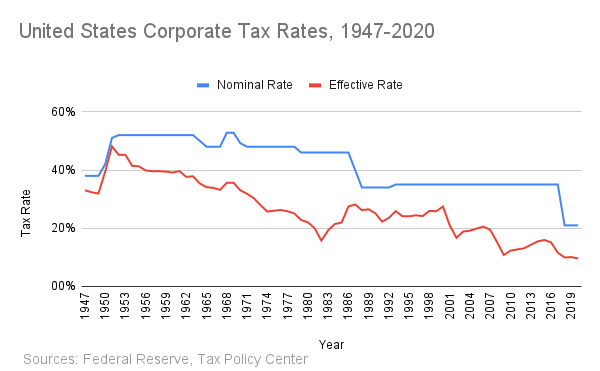

Corporate tax rates have declined since their post-war highs in the 1950s and ‘60s. In 1968, the top statutory rate on corporate income was 52.8 percent. As of 2018, the rate is 21 percent. The effective corporate rate peaked at 48.14 percent in 1951 and has now fallen to 9.6 percent.

U.S. Corporate Tax Rates, 1947-2020

Sources: Federal Reserve, Tax Policy Center

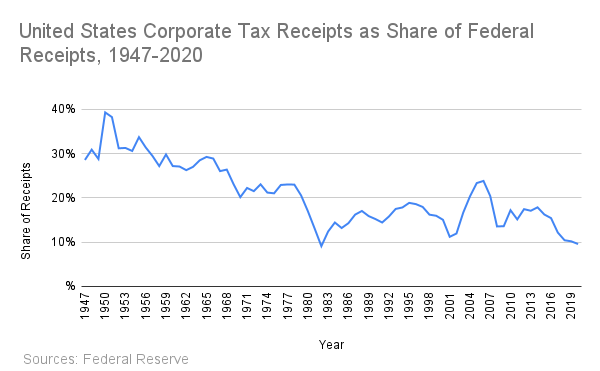

Corporate taxes also used to represent a larger share of federal revenue. From 1947 to 1960, corporate tax receipts made up an average of 31.27 percent of all federal receipts, peaking at 38.26 percent in 1950. Since then, corporate tax receipts as a share of federal receipts have fallen to 9.58 percent.

U.S. Corporate Tax Receipts as Share of Federal Receipts, 1947-2020

Source: Federal Reserve

Much of the reduction in effective corporate tax rates and receipts can be attributed to the rise of pass-through entities (sole proprietorships, partnerships, and S-corporations) and large tax expenditures that have lowered tax burdens for many corporations.

Pass-throughs do not pay corporate taxes and are taxed less heavily than C corporations. As a result, the number of pass-through businesses has been increasing and is now 20 times greater than the number of C corporations. However, C corporations still provide more revenue per entity than pass-throughs and are a significant source of revenue if taxed properly.

Tax expenditures for businesses surpass corporate tax revenue. The expenditures cost over $250 billion annually, while corporate tax receipts totaled only $217 billion. Following the TCJA, numerous companies reported little to no federal tax payments as new expenditures and nominal rate cuts drove burdens to the floor.

Biden Corporate Tax Proposals

The White House is taking advantage of public sentiment in favor of corporate tax reform to push for a revolution in corporate taxation. The administration wants to use these reforms as pay-fors in a broader infrastructure package. The reforms would fundamentally rewrite the rules and expectations of corporate taxation.

- 28 Percent Corporate Tax Rate ($858 billion): In 2017, Republicans slashed the marginal corporate tax rate from 35 percent to 21 percent, leading to a significant drop in corporate tax revenue and further consolidation of wealth by multinational corporations. President Biden has proposed a seven percent increase in the marginal rate, but Republicans and some moderate Democrats labor under the misconception that a slightly higher rate will make American business less competitive. A CRS analysis finds that these concerns are not supported by evidence.

- 15 Percent Minimum Book Tax ($148 billion): While the marginal corporate tax rate is 21 percent, the largest 1,600 firms only paid an average effective federal tax of 7.8 percent, with dozens paying nothing. In Biden’s plan, any corporation operating in the U.S. with income above $2 billion would have to pay a 15 percent minimum on its worldwide book income. Corporations would be allowed to claim a book tax credit (generated by a positive book tax liability) against regular tax in future years, though this credit could not reduce tax liability below the 15 percent minimum rate. Per Treasury, 180 corporations would meet the $2 billion threshold, though only around 45 pay so little in taxes that they would be hit under minimum book.

- 21 Percent Global Minimum Tax ($533 billion): Biden seeks to reform the 10.5 percent global intangible low-taxed income (GILTI), enacted as part of the TCJA to dissuade profit-shifting overseas, with a more comprehensive 21 percent global minimum tax (GMT). Biden’s proposal would change how corporate global tax liability is calculated to a country-by-country basis, reducing the likelihood of avoidance. The G7’s tentative international corporate tax agreement is a major step forward, though the effective rate is lower than Biden’s proposal.

- Rolling Back Corporate Deductions ($124 billion): As part of the TCJA, Republicans gave corporations a 37.5 percent deduction for Foreign Derived Intangible Income (FDII) to encourage companies to repatriate. But this deduction has largely functioned as a windfall for multinationals with high export sales and creates a perverse incentive to move tangible assets overseas. Biden has proposed to fully repeal this deduction and put the savings towards encouraging domestic research and development.

Additional Source of Corporate Revenue to Consider:

- Eliminating Pass-Through Deduction: The 2017 TCJA allowed owners of pass-through entities to deduct up to 20 percent of their business income through 2025. Almost half of this preferential tax treatment went to the top one percent of earners while having no discernible economic benefit. Biden ran on closing the pass-through deduction for incomes over $400,000, which would have raised $200 billion over five years and removed it as a bargaining chip when most TCJA provisions expire. This campaign promise was absent from the White House’s revenue package.

Can We Get There?

While some Republicans have participated in infrastructure talks, Biden’s call for paring back or altering provisions of the 2017 tax law — most notably increasing the corporate tax rate — has drawn intense opposition from Republicans. Minority Leader McConnell stated last month that any changes to the Trump tax bill are a “red line” for his caucus. Sen. Capito, the one-time principal GOP negotiator on infrastructure, called a corporate tax increase “a non-negotiable red line.”

On the international side, Republicans are likewise intransigent. Arguing it would undermine the country’s economic competitiveness abroad and cede a level of sovereignty to foreign governments and regulators, Sen. Toomey slammed the Yellen/G7 plan to enact a GMT as “terrible policy.” And GMT faces a long road ahead overseas. The G20, which meets next month in Italy, must approve the pillars of the agreement, and from there it would go to an OECD-led group on taxes. Finally, assuming the GMT passes those hurdles, individual countries must enact it into legislation, where Toomey and Senate Republicans will likely step in and block passage.

What Lies Ahead

President Biden is in a position to rewrite the United States’ corporate tax laws. He can only do so if he decides to confront procedural and political headwinds in the Senate. But Democrats have the sunsetting TCJA provisions in 2025 in their pockets. When provisions reducing individual income tax rates, increasing estate tax exemptions, and establishing the pass-through deduction are at risk, Republicans will have no choice but to come to the negotiating table.

Right away I am going away to do my breakfast, after

having my breakfast coming again to read further news.

Wow, this post is fastidious, my sister is analyzing these

things, therefore I am going to tell her.

An impressive share! I’ve just forwarded this onto

a coworker who has been doing a little research on this. And

he in fact bought me lunch simply because I stumbled upon it for him…

lol. So allow me to reword this…. Thank YOU for the

meal!! But yeah, thanx for spending time to talk about this topic here on your blog.

What i don’t realize is in truth how you are no longer really a lot more

smartly-liked than you might be now. You are very

intelligent. You realize thus significantly in terms of this subject,

produced me in my opinion imagine it from numerous varied angles.

Its like women and men aren’t interested except it’s one thing to do with

Woman gaga! Your own stuffs great. All the time care for it up!

The other day, while I was at work, my cousin stole

my apple ipad and tested to see if it can survive a 25 foot drop,

just so she can be a youtube sensation. My apple ipad is now broken and she has 83 views.

I know this is entirely off topic but I had to share it with someone!

After looking into a few of the blog articles on your web page,

I really like your technique of blogging. I book-marked it to

my bookmark site list and will be checking back soon. Please

visit my web site too and tell me what you think.

I am extremely impressed with your writing skills and also with the

layout on your blog. Is this a paid theme or did you customize it yourself?

Either way keep up the excellent quality writing, it is rare to see

a nice blog like this one these days.

Hi! I know this is somewhat off-topic however I needed to ask.

Does managing a well-established blog like yours take a

lot of work? I am completely new to operating a blog but I do write in my

journal daily. I’d like to start a blog so I can share my

personal experience and feelings online.

Please let me know if you have any suggestions or tips

for brand new aspiring blog owners. Thankyou!

Hi my family member! I want to say that this post is amazing, great written and come with almost all vital infos.

I would like to peer extra posts like this .

SamuelTNSanta Ana

AlexanderCOVictorville

odia story book janha mamu Truefrench Torrent aliciadevoucoux book.com

Luxury Vip Casino Cigarette Electronique Casino La Croix Rouge R Sidence Du Casino Menton

Casino Larmor Plage Projet Restaurant Senso Casino Slain Branchement Carte Pci 16x Sur Slot Pci X1

stromectol 3 mg tablet price

levitra medication

cialis online cheap

ivermectin 2

stromectol without prescription

ivermectin 1 topical cream

stromectol buy

stromectol ivermectin tablets

stromectol 3 mg tablet

stromectol 3mg

ivermectin canada

price of ivermectin

ivermectin 3 mg tablet dosage

buy ivermectin cream

buy liquid ivermectin

cost of ivermectin

ivermectin

kamagra 100mg oral jelly in uae

generic cialis 2017

stromectol

cheap prednisone online

kamagra gel uk

viagra price in mexico

buy kamagra soft tabs

buy cialis 5mg

tadalafil generic usa

sildenafil free shipping

viagra 100mg price

viagra dubai online viagra logo – next day viagra delivery

generic viagra without prescription cheap chinese viagra paying with paypal – viagra for men free samples

viagra over the counter

sildenafil online cheap

viagra generic online pharmacy

gay dating sites reddit

gay mature men dating sites

romeo gay dating site

cialis online drugstore

buy tadalafil usa

kamagra 500mg

tadalafil capsules 7mg

sildenafil generic canada

can you buy disulfiram over the counter

android site for gay dating

gay furry dating game

gay chubby dating tumblr

[url=http://nvpills.com/]lexapro 20 mg[/url]

[url=http://ogrmeds.com/]motilium online[/url]

viagra pharmacy usa

female viagra tablet

gay christian dating site free

gay bondage dating sites

totally free gay dating

tetracycline antibiotics

viagra gel for sale uk

stromectol 3 mg