Update 753 — Focus on Consumer Credit:

Can the Goose Keep Laying Golden Eggs?

The American consumer stands at the heart of the nation’s powerful post-COVID economic recovery that has not just staved off recession amid steep Fed interest rate hikes but produced growth that leads the industrialized world. A combination of critical pandemic-era federal assistance, real wage gains, and savings amassed during COVID has enabled a surge in consumer spending that lifted GDP growth to 3.1 percent in 2023.

The question now is whether the massive consumer spending trends are sustainable. Today, we look at the consumer credit landscape and assess the impact of Fed policy, phased-out assistance and clouds on the horizon in the form of credit card delinquencies and reduced mortgage applications. Are these harbingers of a reversal of the spending patterns lifting the economy, or circumstantial patterns we can expect to pass? More below.

Best,

Dana

———————————————————————————

In the fourth quarter of 2023, consumer spending, as measured by personal consumption expenditures, continued its recent surge, increasing by 2.8 percent, driven, in part, by real wage gains and high retail spending during the holiday season. Much of that spending was fueled by consumer credit, which includes any way that consumers take on personal debt to buy goods and services, such as credit cards. Consumer credit increased by 2.4 percent in 2023 according to the Federal Reserve; it is less than the 4.6 percent increase seen in 2019 before the pandemic, but represents a significant growth in borrowing to support spending.

In total, American household debt increased by $604 billion in 2023 to reach a total of $17.5 trillion by the end of the year. At the same time that Americans borrowed more to fuel their spending, borrowing itself became more difficult for consumers due to high interest rates and the tightening of lending standards by banks, a trend that started early in 2023. The spending has continued unabated, but can it be sustained?

Credit Card Debt is Up, but so are Delinquencies

The area of consumer debt that saw the sharpest increase was credit card debt. Credit card debt rose in 2023 as Americans burned through pandemic-era savings in the face of inflation, with the rise in prices sapping 40 percent of Americans of said savings as of December 2023. As inflation depleted Americans’ finances in 2022, many turned to spending on credit to maintain their standards of living.

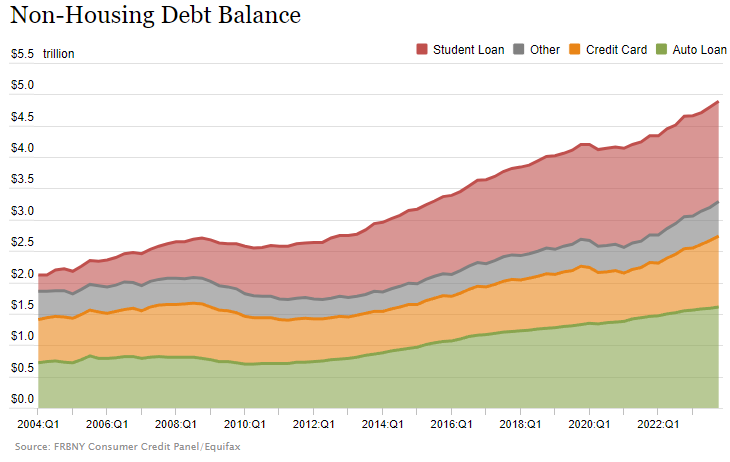

According to the Federal Reserve Bank of New York, credit card debt held by Americans rose $50 billion in the fourth quarter of 2023, a 4.6 percent jump from the previous quarter. This increase brought the total credit card debt in the United States to a record high of $1.13 trillion, representing 23 percent of non-housing debt. About 10 percent of credit-card borrowers now have an account balance that exceeds $5,000, as compared to 7 percent in Q4 of 2019. This rise in household debt is compounded by the average interest on bank credit cards reaching 21.5 percent, the highest since the Federal Reserve started tracking the data in 1994.

Source: Federal Reserve Bank of New York

As credit card debt rises, there are signs that Americans are less able to pay it off. According to the New York Fed, the rates of serious delinquencies – as measured by the percentage of balances that were 90 days or more delinquent – on credit card balances rose to 6.36 percent in Q4 of 2023, an increase of 2.35 percentage points over the same quarter in 2022. Overall delinquency rates on credit card balances reached 8.5 percent by the end of 2023, their highest level since 2013. While delinquency rates rose across all age groups, those aged 18 to 29 saw the highest serious delinquency rate of roughly 10 percent, while delinquencies rose fastest for millennials aged between 30 and 39 with a serious delinquency rate of a little less than 9 percent. Both of these age cohorts also are dealing with a resumption in student loan payments, further adding to their financial stress.

Americans are also slower to pay off their credit card debt, with each of the four biggest American banks – JP Morgan Chase, Citigroup, Bank of America, and Wells Fargo — reporting an increase in credit card loans in 2023. This rise in credit card delinquency is causing banks to respond in kind, with the Philadelphia Fed reporting that banks are tightening their credit standards, granting fewer credit-line increases, and reducing limits more frequently. The rise in credit card debt and the increased difficulties in paying off said debt indicate increased financial stress for many American household borrowers, one that could imply reduced consumer spending should it continue.

Mortgage Applications Low as Rates Remain High

Rates on 30-year fixed mortgages have fluctuated considerably over the past couple of years, as rates have risen and fallen largely in response to changes in the federal funds rate. While average mortgage rates briefly exceeded 8 percent in October — a 20-year high — they fell to below 6.7 percent in December after the Fed decided to hold interest rates steady at the 5.25 to 5.5 percent range. The average mortgage rate in the 30-year loan surpassed 7 percent again as of February 5, as the surprisingly strong January jobs report suggested that the economy is growing, suggesting the Fed will hold off on lowering interest rates for the time being, lifting mortgage rates.

High mortgage rates have translated to lower demand for 30-year fixed mortgages, creating a ripple effect in the housing market. High mortgage rates mean that many would-be first-time home buyers are holding off on purchasing a home. Existing homeowners are “locked in” to their existing mortgages with rates well below current market rates, unwilling to purchase a new home or refinance their current mortgages as a result. In response to the spike in mortgage rates, applications last October hit their lowest level since 1996.

While mortgage applications rose steadily through mid-January in response to the easing of mortgage rates, the recent uptick in rates suggests that demand for mortgages will remain depressed. Mortgage debt also increased by $112 billion in Q4 of 2023 to a total of $12.25 trillion, representing about 70 percent of household debt, though the serious delinquency rate for mortgages remained low at .82 percent due to a combination of fewer low-quality borrowers and the aftereffects of the refinancing boom during the pandemic. The lack of affordable mortgages helped cut 2023 sales to lowest year existing homes in the US since 1995, though new home sales in 2023 showed signs of recovery. Unless the Fed cuts interest rates and mortgage rates fall accordingly, high rates will likely continue to burden the housing market throughout 2024.

Other Types of Consumer Debt

Auto loans also saw a rise in delinquencies in the fourth quarter of 2023. 7.69 percent of auto loan balances became delinquent — the highest level of delinquency since 2010 — while 4.2 percent were seriously delinquent. Auto loan debt rose by $25 billion in Q4 of 2023, with a total of $1.61 trillion or 32.9 percent of non-housing debt. The rise in auto loan debt is due largely to car ownership itself becoming more expensive, as a combination of inflation and supply chain issues sharply increased the price of cars and high interest rates increased auto loan costs. This trend produced a jump in the average monthly payments on new car loans, which are now well above $500 compared to $450 for people in the highest income bracket in 2017.

While cars represent one of the largest purchases average Americans make, second only to buying a home, Americans are less likely to put off buying a car compared to buying a home. 68 percent of Americans use their cars to drive to work, while 88 percent use their cars to shop for groceries, meaning that cars are a necessity for many American families. As such, over 100 million Americans have an auto loan.

Beyond the above — credit card debt, mortgage debt, and auto debt — other kinds of consumer debt are on the rise, as well. Home equity lines of credit (HELOC) increased by $11 billion in Q4 of 2024, with Americans holding $360 billion. Consumer finance and retail loans increased by $25 billion in 2023, totaling $554 billion.

Fed Interest Rate Hikes and Consumer Debt

The Federal Reserve plays an outsized role in consumer credit through its adjustment of the federal funds rate, which has a significant, though indirect. effect on the cost of consumer credit: by changing the federal funds rate, the Fed influences borrowing costs for lenders, putting upward pressure on interest rates charged by banks for consumers. Fed fee hikes have indirectly influenced the borrowing cost for financial products including mortgages, credit cards, and auto loans. After the Fed started raising rates in early 2022, credit card rates jumped from 16.34 percent in March 2022 to 21.5 percent today while mortgage rates surged from under four percent to over seven percent in that same period.

While the increase in consumer spending bolstered by consumer credit may fuel greater economic growth in the short term, the increase in delinquencies begs the question: how long that spending can last?

What Lies Ahead for Consumers?

We are inching closer to the point where consumers maintaining a higher level of spending through increasing their debt burden becomes unsustainable. The ratio between total credit card debt and deposits rose to 7.1 percent in the third quarter of 2023. The Fed has sought since the beginning of its ongoing cycle of interest rate hikes, to reduce inflation, but for household debt in particular.

But economists aren’t yet sounding the alarm on the state of consumer credit. While consumer debt has resulted in higher overall household debt, the Fed’s household debt service ratio — which measures household debt-servicing payments as a percentage of disposable personal income — was 9.77 percent, below what it was at the end of 2019 and significantly below the ratio for much of the 2000s.

While delinquency rates for credit card debt and auto loans increased significantly by the end of 2023, the overall delinquency rate on outstanding debt stood at 3.1 percent, 1.6 percentage points below what it was in the fourth quarter of 2019. In short, there are a few troubling signs regarding consumer credit but the situation is not so dire that people should begin to panic.

Going forward, one should keep an eye out for if overall delinquency rates begin to reach the heights that they did during the Great Recession (topping out at nearly 5 percent) or if the household debt service ratio rises to the same peaks it climbed to during the same period (over 13 percent). Until household debt reaches a point where Americans are unable to pay, as would be indicated by a spike in the household debt service ratio and overall delinquency rates, consumer credit will likely continue to fuel consumer spending for the foreseeable future.