Update 804 — July CPI Gain Under 3%;

Dip Marks Lowest Increase Since 2021

Today, Democratic presidential hopeful Kamala Harris released her lowering costs agenda, her most specific plan to date on economic policy, which she has pledged to pursue in her first 100 days in office. The agenda addresses a myriad of economic priorities, including housing policy, medical and grocery costs, and tax relief for lower- and middle-class Americans. Next week, we take a deeper look into the Harris economic policy agenda as Democrats meet in Chicago for the much-anticipated Democratic National Convention.

The release of Harris’s economic policy agenda comes just two days after the Bureau of Labor Statistics released new inflation data for July, showing that inflation has fallen to its lowest level in over three years. With inflation remaining the central economic issue of the election cycle, we explore the CPI report and the growing need for the Federal Reserve to cut interest rates next month.

Good weekends, all…

Best,

Dana

The cost of living continues to be front of mind for American families, particularly as they face high prices at the grocery store. Inflation, which spiked during 2022, has continued to be a central issue for voters and campaigns ahead of the November general election.

This week, inflation crossed a notable milestone, falling below three percent growth on a year-on-year basis for the first time in over three years. This progress prompted many Democrats to declare victory over inflation, as the Harris campaign highlighted its plans to lower costs for American families.

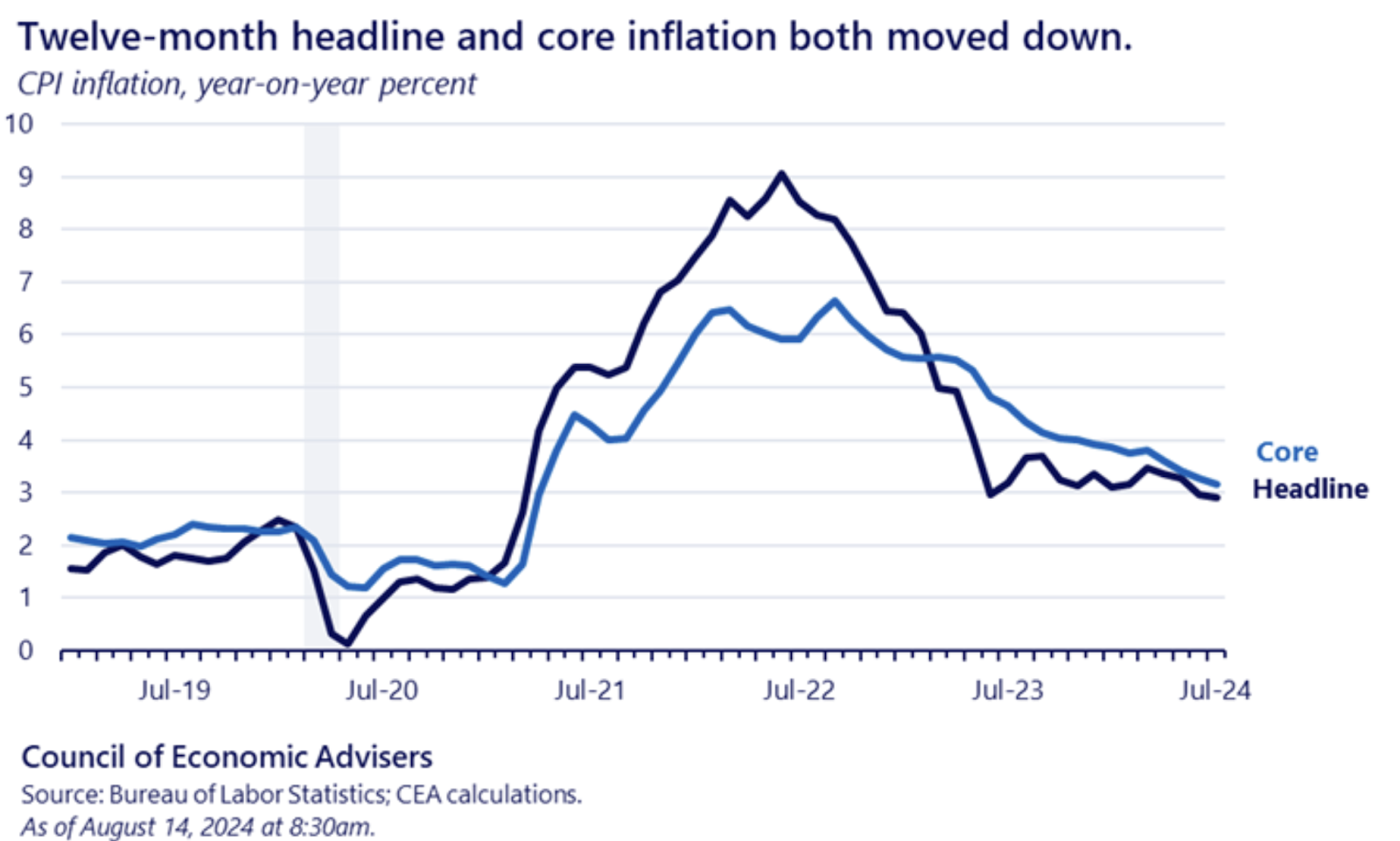

Inflation Falls Below 3 Percent In July

Inflation fell below three percent last month for the first time since March 2021, according to the July Consumer Price Index (CPI) report which the Bureau of Labor Statistics released on Wednesday.

Consumer prices rose by 0.2 percent on a monthly basis and by 2.9 percent on a year-on-year basis in July. Headline CPI decreased on a year-on-year basis for the fourth consecutive month, falling below 3.0 percent for the first time since March 2021. Core CPI inflation – which excludes food and energy prices – also rose by 0.2 percent on a monthly basis and rose by 3.2 percent on a year-on-year basis in July. On a year-on-year basis, core CPI fell to its lowest level since April 2021 last month.

This week’s CPI data makes clear that inflation is moving closer to the Federal Reserve’s two percent target. Headline CPI finally falling below three percent shows the significant progress in reining in inflation, which peaked at 9.1 percent in June 2022.

Source: Council of Economic Advisers

Prices within several sectors notably rose last month, including:

- Housing – The shelter index – a measure of the cost of housing that comprises roughly a third of the overall index – rose by 0.4 percent on a monthly basis in July, leading the overall index. One component of shelter costs, rents, rose by 0.5 percent in July, up from a 0.3 percent increase in June. Shelter costs rose by more than expected last month. Shelter inflation is far lower than at its peaks in 2022 and early 2023.

- Food – Food prices rose by 0.2 percent on a monthly basis in July, just as they had in June, with grocery prices rising by 0.1 percent and prices of food away from home rising by 0.2 percent.

- Energy – Meanwhile, energy prices remained flat on a monthly basis in July after falling by 2.0 percent in June, with gasoline prices remaining unchanged, electricity prices increasing by 0.1 percent over the month, fuel oil prices increasing by 0.9 percent, and natural gas prices decreasing by 0.7 percent.

Prices of used cars and trucks, airline fares, and hospital services each fell by at least one percent on a monthly basis in July.

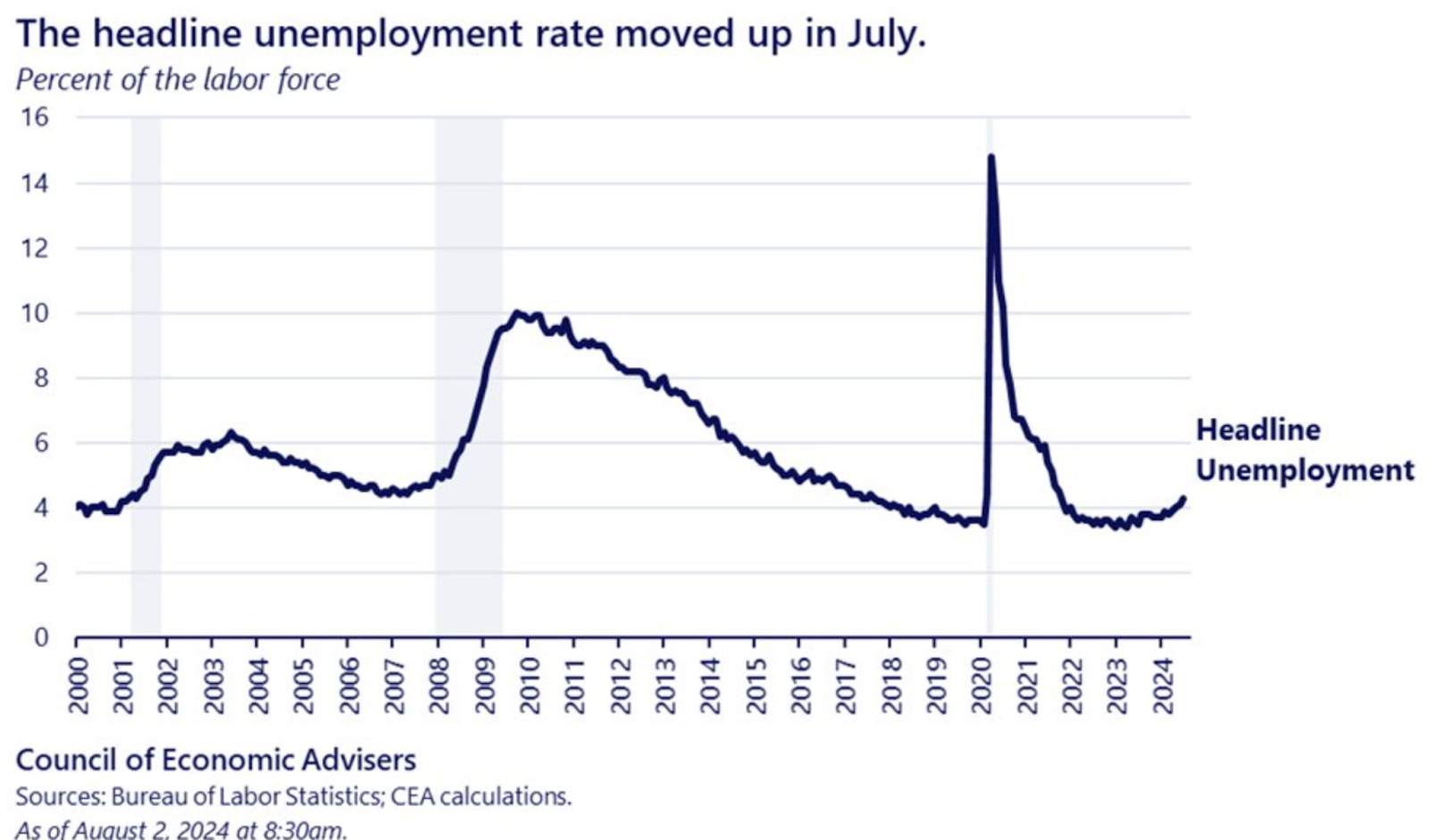

Labor Market Cooling Amidst High Interest Rates

Last month’s continued progress on inflation is a positive sign, but some of this progress has come at the expense of the strength of the labor market, which has seen unemployment increase, job gains moderate, and wage growth slow in recent months.

The Federal Reserve raised interest rates from near zero in early 2022 to the 5.25 to 5.5 percent range last July and has opted to hold rates at this elevated level ever since. While the labor market remained remarkably strong amidst the Fed’s current cycle of rate hikes, unemployment has risen, job growth has notably moderated, and wage growth has slowed in recent months. This labor market cooling was evident in the cooler-than-expected July jobs report, which showed signs of cooling below the surface becoming clear.

Last month, elevated interest rates pushed the unemployment rate to 4.3 percent, its highest level since October 2021. Job growth over the three months ending in July averaged roughly 170,000 jobs. This is a notable moderation as three-month average job growth remained over 200,000 jobs earlier this year. Additionally, wage growth on an annualized basis slowed in July to 3.6 percent, down from 3.9 percent in June.

Source: Council of Economic Advisers

Though unemployment remains historically low and job gains and wage growth remain relatively strong, a continuation of recent trends could reverse some of the extraordinary labor market gains the American economy has seen in its post-pandemic recovery.

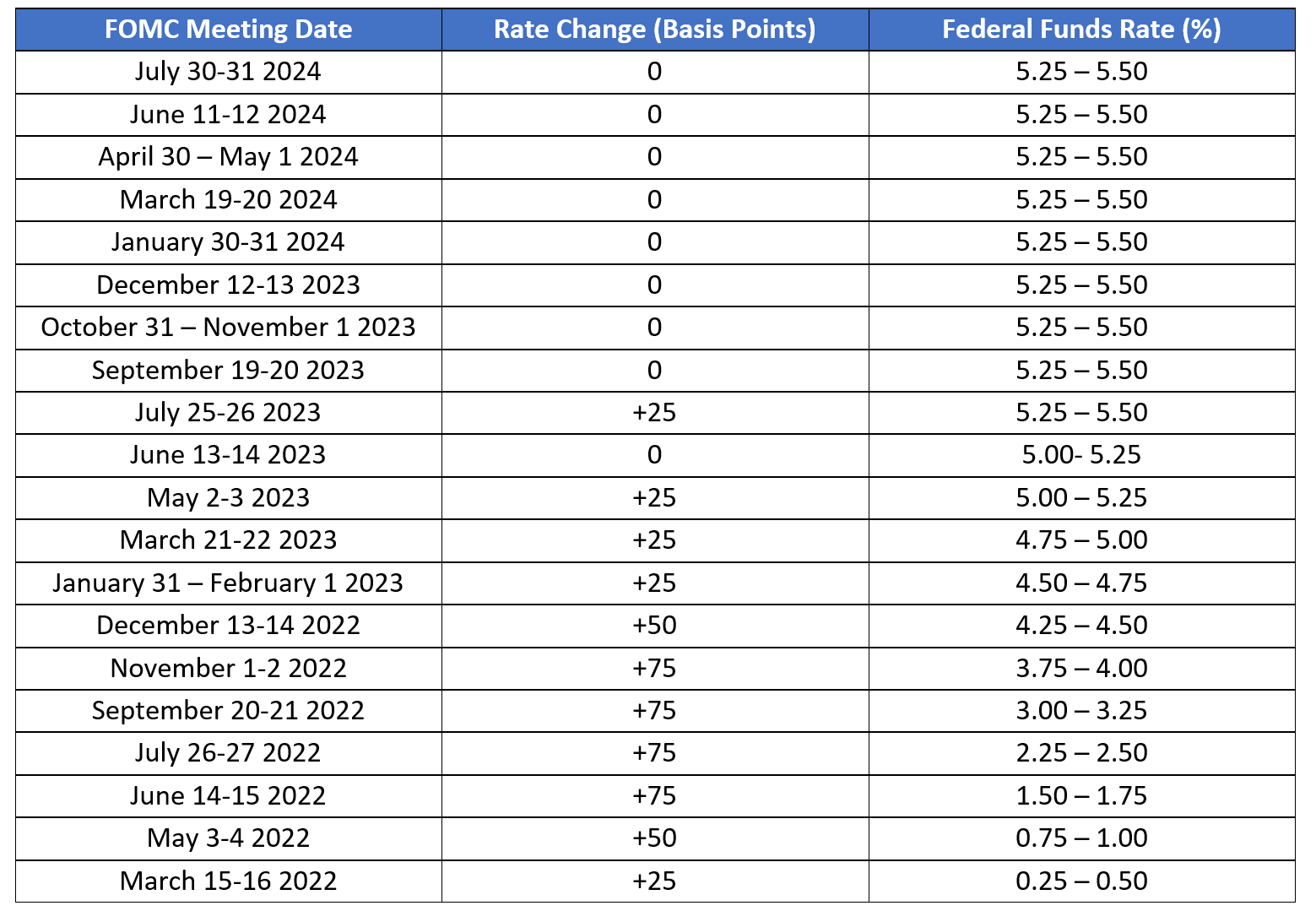

Fed Poised to Cut Rates in September, But By How Much?

The release of the July jobs report came days after the Federal Open Market Committee’s (FOMC) last meeting in which the Fed’s interest rate-setting body opted to hold rates steady. The Committee strongly signaled that it would initiate cuts at its next meeting on September 17 and 18. The labor market cooling revealed in the jobs report combined with this week’s inflation data sets the FOMC on a solid path to cut rates next month. The question FOMC officials should be considering is not whether but by how much interest rates should be cut.

The Committee began hiking rates slowly in 2022, initially increasing the interest rate by 25 basis points, then by 50 basis points, then by 75 basis points in each of four consecutive meetings.

With the stress of elevated interest rates continuing to restrict the labor market, the FOMC should not risk lowering interest rates as gradually as it increased them. A 25 basis point cut would bring the interest rate to the 5.0 to 5.25 percent range, a lower but still remarkably restrictive level, where it would remain until the FOMC’s following meeting in November. As Federal Reserve Chair Jerome Powell noted last month, monetary policy acts with long and variable lags which will apply as interest rates are lowered. The easing of restrictive monetary policy will take time to affect financial conditions, economic activity, and the labor market. Reducing the tightness of monetary policy too little could weaken the broader economy.

The August jobs report to be released ahead of the FOMC’s next meeting may very well show that such labor market weakening has continued, while the July Personal Consumption Expenditures (PCE) Price Index data and the August CPI report, which will be released in the coming weeks, are likely to show inflation continuing to trend downward.

Should the data continue to follow recent trends, the Committee should opt to cut the interest rate by 50 basis points at its next meeting, bringing the interest rate to the 4.75 to 5.0 percent range. Fed Chair Powell could use his address at the Jackson Hole Economic Symposium later this month as an opportunity to signal that such a cut is on the table.

As the Fed’s goal of bringing inflation down appears to be all but achieved, it must now focus on fulfilling the other half of its dual mandate, promoting maximum employment. With interest rates held at an elevated level for over a year, a rebalancing of the mandate is crucial at this point in the Fed’s rate hike cycle, especially to avoid recession which the American economy has managed to stave off over its post-pandemic recovery, and ensure that the soft landing that has been tentatively achieved is not jeopardized.