Update 777 — 175,000 Jobs Added in April

Labor Market Data; Week’s Key Hill Hearings

On Wednesday, Fed Chair Powell made clear that long-elevated interest rates would remain in place, perhaps well into autumn, until either price or labor market data showed a retreat. This morning’s jobs report showing the economy added 175,000 jobs in April — well below broad estimates of 240,000 net additions — hints that the labor market, while still strong, may finally be starting down a path to softening and eventual interest rate cuts.

Below, we put this April payroll data in perspective, review the month’s dip in consumer confidence, and cover the week’s key economic policy hearings on the Hill, including the Senate Banking look into deceptive pricing practices that aggravate inflation.

Good weekends all…

Best,

Dana

Headline

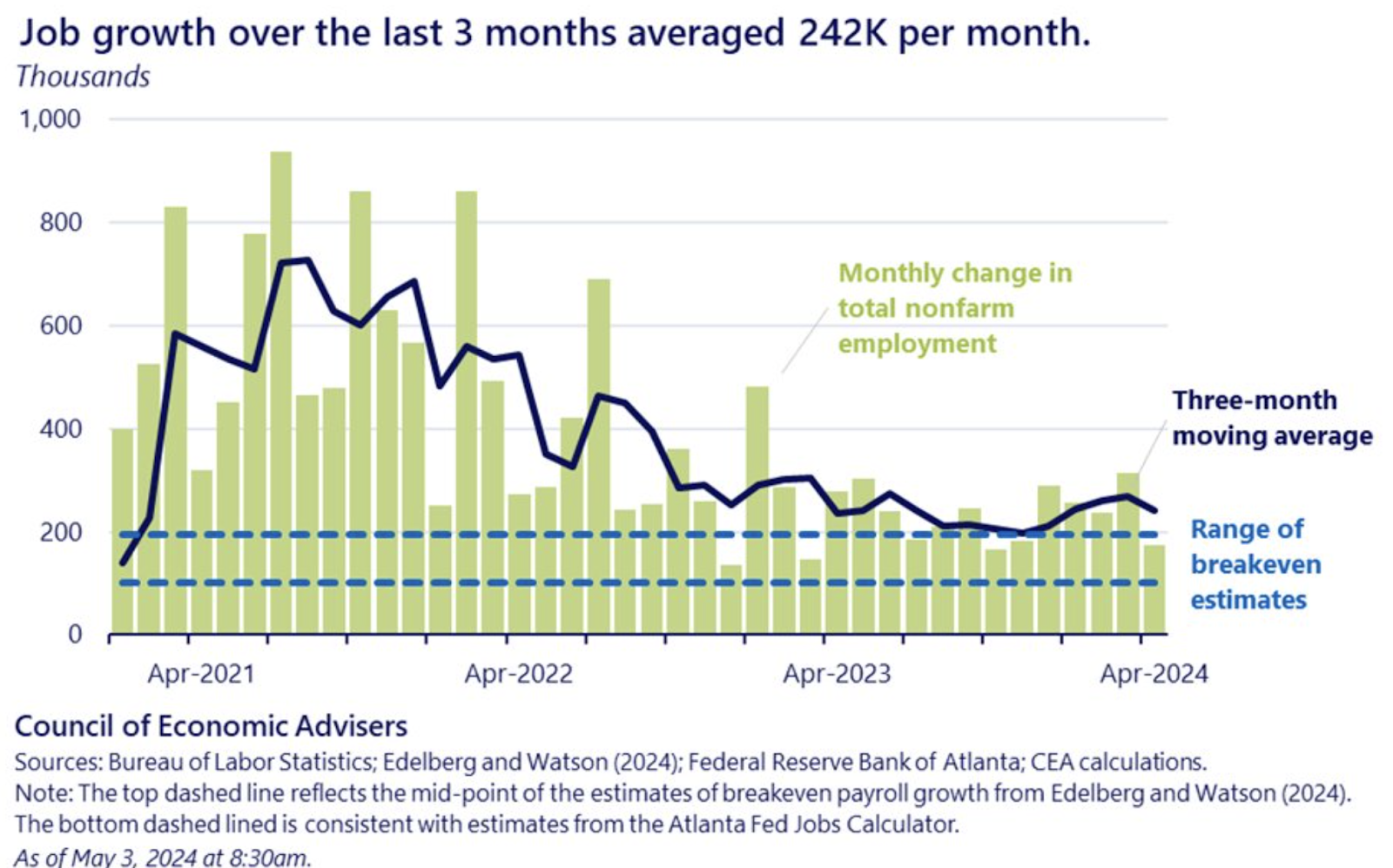

Lower-Than-Expected 175,000 Jobs Added in April

Total nonfarm payroll employment rose by roughly 175,000 jobs and the unemployment rate ticked up slightly to 3.9 percent in April, according to this morning’s DOL jobs report,

Job gains last month came in far lower than the 240,000 estimated by economists. Despite the lower-than-expected figure, April nevertheless represents the fortieth consecutive month of job growth. The largest gains came in:

- health care (56,000 jobs)

- social assistance (31,000 jobs)

- transportation and warehousing (22,000 jobs)

- retail trade (20,000 jobs)

- construction (9,000 jobs)

- government (8,000 jobs)

Job growth in March was revised up by 12,000, from 303,000 to 315,000 jobs, while job growth in February was revised down by a notable 34,000, from 270,000 to 236,000 jobs. This brings the average monthly gain over the past three months to 242,000.

Source: Council of Economic Advisers

The unemployment rate ticked up slightly from 3.8 percent in March to 3.9 percent last month, with 6.5 million people unemployed. The unemployment rate has remained in the 3.7 percent to 3.9 percent range since August and is still historically low. The unemployment rate has now remained below four percent for 27 consecutive months, the longest such stretch in over 50 years.

In April, average hourly earnings for all employees on private nonfarm payrolls increased by 0.2 percent, and by 3.9 percent over the past 12 months, below expectations. Although inflation data for April is yet to be released, on an annualized basis, wages are likely to have outpaced inflation last month. Wage increases have consistently run ahead of inflation since last May.

This week, Fed Chair Jerome Powell made clear that Federal Open Market Committee (FOMC) officials see two paths the economy could take in order to warrant initiating interest rate cuts: 1) inflation trending toward the Fed’s two percent goal or 2) a slowing of the labor market. Today’s jobs report is unlikely to push the FOMC toward a cut at its next meeting in June. In fact, markets are pricing in cuts not starting until November. The report shows that the labor market remains strong, but may have begun growing at a slower rate. FOMC officials will surely be watching April’s inflation data out later this month, hoping to see core PCE fall from 2.8 percent in March and headline PCE come down after ticking up to 2.7 percent.

Other Developments

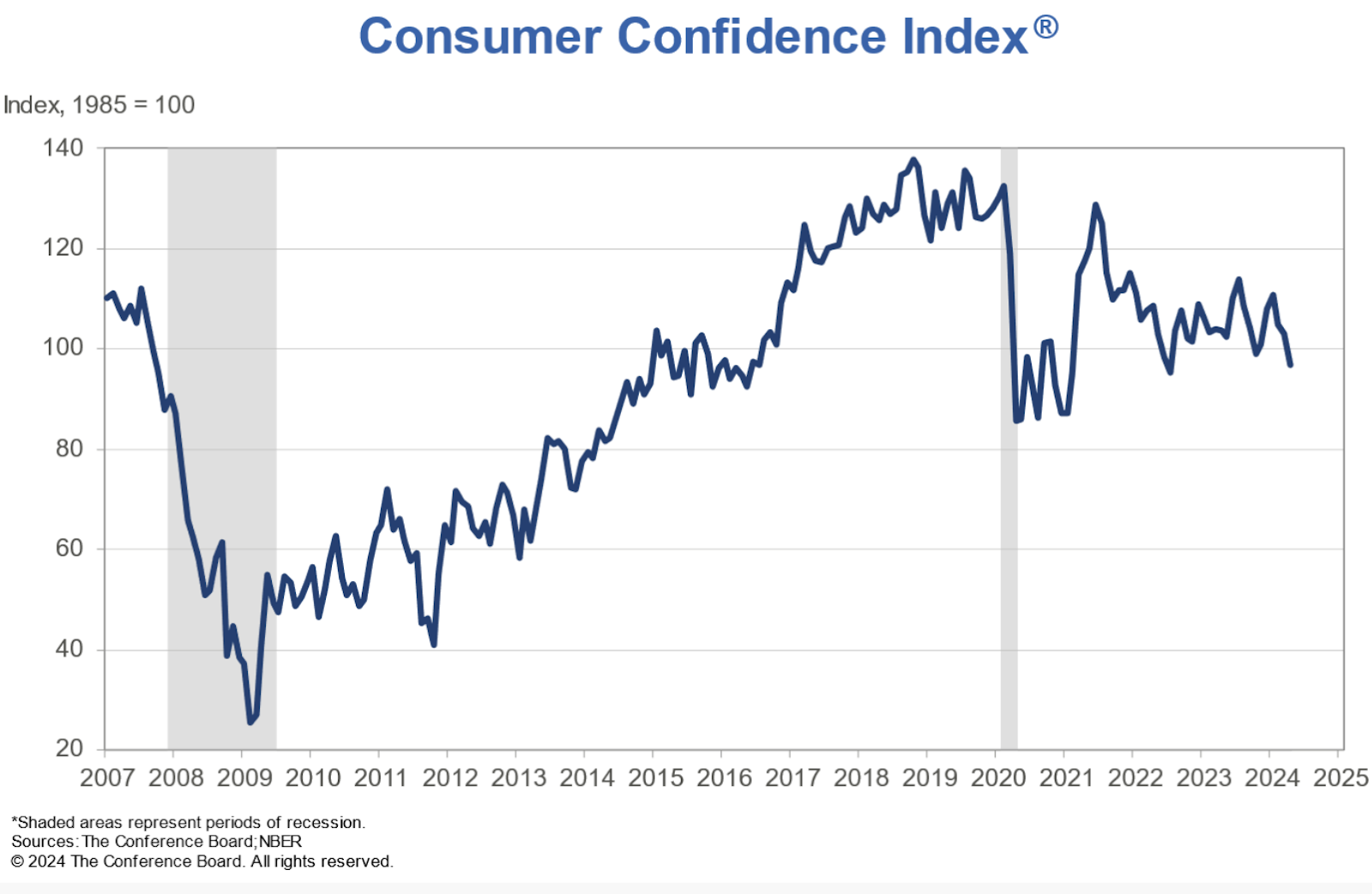

Consumer Confidence Continues to Dip

On Tuesday, The Conference Board released April’s consumer confidence score of 97 which fell from 103 in March. For the third straight month, confidence fell, this time to the lowest level since July 2022.

Source: The Conference Board

The Board also indicated that write-in responses citing “elevated price levels, especially for food and gas, dominated consumer’s concerns, with politics and global conflicts as distant runners-up.”

Meanwhile, new Gallup polls released Thursday showed similar sentiment, with 41 percent of respondents citing overall inflation as their most pressing financial concern ahead of taxes and energy costs. The reports continue to show that Americans are increasingly pessimistic about economic conditions.

Politically, decreasing consumer confidence will likely create difficulties for President Biden’s reelection campaign. The President has had difficulty translating progress on economic gains — record low unemployment, increases in wages, etc. — into poll positivity and Americans’ confidence in his ability to improve the economy thus far.

Biden to Cancel $6 Billion More in Student Debt

On Wednesday, President Biden announced an additional $6.1 billion in student debt forgiveness for 317,000 borrowers. Specifically, this aid is going to former students of the Art Institutes, a private for-profit art school system that closed down last year. The Art Institutes shut down after years of allegations that they had misled students through advertisements and recruitment efforts that exaggerated job placement figures and salary expectations. Biden leaned into how the school network had wronged these former students, stating, “[T]his institution falsified data, knowingly misled students and cheated borrowers into taking on mountains of debt without leading to promising career prospects at the end of their studies.” The newest round of student loan debt relief, provided by President Biden, brings total relief of $160 billion for nearly 4.6 million borrowers.

Hearings

House Ways and Means Questions Secretary Yellen

On Tuesday, Treasury Secretary Janet Yellen testified before the House Ways and Means Committee regarding the Administration’s FY25 budget proposal. Democratic members highlighted the positive state of the U.S. economy and the Biden Administration’s plans to build off of our remarkable economic recovery as shown through its latest budget proposal, while Republican members questioned the President’s track record and future plans.

TCJA Expirations and $400K pledge

Republicans like Committee Chair Jason Smith (R-MO) repeatedly took aim at President Biden’s recent statement that he would let major provisions of the Tax Cuts and Jobs Act (TCJA) expire as scheduled after 2025. GOP members argued that this plan is at odds with his promise not to increase taxes on Americans who make less than $400,000 a year (commonly known as his $400K pledge) as TCJA expirations would affect Americans under his target income threshold. But Secretary Yellen reiterated Biden’s commitment to ensuring this income cohort is protected from tax increases. Though President Biden has some time left before 2025 to clarify his plans for protecting taxpayers under the $400K threshold, it seems Republicans will continue to target this perceived contradiction as we approach the 2025 tax fight.

Direct File

The IRS was also a point of discussion in Tuesday’s hearing following the extremely positive 2024 tax filing season. Not only has the IRS made major strides in IT modernization and improving customer service, but it has also introduced a pilot program for Direct File — a service allowing taxpayers to fill out and file their taxes for free directly through an IRS website. Ways and Means Ranking Member Richard Neal (D-MA) relayed positive feedback for the program, which was available for taxpayers with relatively simple returns in Massachusetts and 11 other states. Secretary Yellen voiced her support for the Direct File program as well, noting that it helped save over 140,000 taxpayers an average of $270 and 13 hours this filing season. Treasury and the IRS have yet to release plans for Direct File moving forward, but the pilot’s success gives reason to be hopeful for expansion.

Senate Banking on Firms’ Deceptive Pricing Practices

On Thursday, the Senate Committee on Banking, Housing, and Urban Affairs held a hearing in which it discussed how “shrinkflation” and other deceptive pricing practices – enabled and exacerbated by technology and consolidation – have affected consumers.

Corporate profits contributed over 50 percent of overall inflation during the second and third quarters of last year according to research by Groundwork Collaborative, with the remaining increase in prices being due to other factors playing out throughout the economy. As Bilal Baydoun, Director of Policy and Research at the think tank noted in his testimony, many companies used inflation as cover to roll out an array of deceptive pricing strategies that allowed them to drive prices and in turn their profits up.

These strategies include so-called “shrinkflation” which occurs when companies reduce the quantity or size of a product while keeping the price the same or even raising it. As Committee Chair Sherrod Brown (D-OH) noted, companies have also begun to use “dynamic pricing” in which prices adjust in real-time using pricing algorithms and consumer data. Brown discussed the example of a consumer shopping around online for the lowest price on a washing machine, explaining “Now online retailers realize that you’re in the market for appliances, and start showing you higher and higher prices.” Brown cited a bill he has introduced with Senator Bob Casey (D-PA), S.3819, the Shrinkflation Prevention Act of 2024, which would direct the Federal Trade Commission to issue regulations to establish shrinkflation as an unfair or deceptive act.

Firms should make more money through innovation -– by innovating to provide better, cheaper goods and services to customers, rather than by figuring out the maximum price a consumer is willing to pay for a product. As technology becomes more and more advanced and industries become more and more consolidated, we must rein in corporations’ ability to price gouge their way to higher profits at the expense of consumers.

HFSC on Regulators’ Bank Merger Proposals, Bills to Delay Small Business Lending Discrimination Rule

The House Committee on Financial Services Committee Subcommittee on Financial Institutions and Monetary Policy convened on Wednesday morning for a hearing to discuss proposals by bank regulators to adjust their bank merger policies. The hearing focused on regulators’ recent proposals to adjust their bank merger policies, specifically the Office of the Comptroller of the Currency’s (OCC) proposal put forward in January and the Federal Deposit Insurance Corporation’s (FDIC) proposal put forward last month.

As senior officials at the OCC and FDIC noted at the hearing, more complicated proposals, proposed mergers involving larger and more complex banks, take longer to move through the approval process after a merger proposal is filed. Subcommittee Chair Andy Barr (R-KY) raised concerns that the bank merger approval process can in some cases take twelve months or longer. In response, the official representing the OCC noted that the majority of applications are completed in a timely manner. The hearing considered a bill led by Subcommittee Chair Barr, H.R. 7403, the Bank Failure Prevention Act, which would require regulators to grant or deny a bank merger application submitted within 90 days.

The hearing also discussed two additional bills:

- H.R. 1806, the Small Lenders Exempt from New Data and excessive Reporting (LENDER) Act, led by Representative J. French Hill (R-AR)

- H.R. 1810, the Business Loan Privacy Act, led by Representative Blaine Luetkemeyer (R-MO)

These bills would ultimately delay the Consumer Financial Protection Bureau’s rule implementing Section 1071 of the Dodd-Frank Act by requiring lenders to report data annually on credit applications to help the Bureau better understand the financing needs of small businesses owned by women and minorities and identify possible discrimination in an effort to facilitate the enforcement of fair lending laws

House Cmte. Hearing on Commercial Real Estate Markets

On Tuesday, the House Oversight Committee’s Subcommittee on Health Care and Financial Services held a hearing on Tuesday covering the slow-moving crisis occurring in the commercial real estate (CRE) market. Since the pandemic, commercial real estate – especially office buildings – has seen considerably less use, leaving a lot of commercial real estate at least partially vacant. At the same time, many companies and individuals holding CRE properties owe banks and lenders trillions of dollars in debt, and much of this debt is coming due. While many banks and lenders have given their borrowers extensions in hopes that they will be able to eventually make their payments, $2.2 trillion in debt is set to come due by the end of 2027, and high interest rates make refinancing that debt difficult.

Members of the Subcommittee largely agreed that CRE debt was a problem that needed to be addressed but differed on a number of key issues. In particular, the Republican members focused on criticizing President Biden for supposedly failing to quell and even adding to inflation, thus leading to high interest rates and in turn higher borrowing costs, and putting onerous regulations on the CRE and lending markets. Democrats pushed back on these accusations by arguing that inflation is due to factors outside of President Biden’s control, such as supply chain issues in the aftermath of the pandemic.

Look Ahead

Tuesday, May 7

- House Committee on Financial Services Subcommittee on Capital Markets hearing: SEC Enforcement: Balancing Deterrence with Due Process

- House Appropriations Subcommittee on Financial Services and General Government Budget Hearing: Fiscal Year 2025 Request for the Internal Revenue Service

Thursday, May 9

- Senate Committee on Banking, Housing, and Urban Affairs hearing: Consumer Protection: Examining Fees in Financial Services and Rental Housing