July Inflation 3.2%: Cooling and the Core

The encouraging moderation in prices throughout the economy this summer belies the fact that the trickiest part of fighting inflation lies just ahead: knowing when to stop. The contractionary policy of the Fed, which is in the midst of its steepest set of interest rate increases since the 1980s, has a long and variable lag effect that can take anywhere from 6 to 18 months to kick in. So, the contraction may not cease until next year, a politically sensitive period.

A Fed focus on its credibility in the fight to get the rate of inflation from its current 3.2% annual rate down to the 2% target rate may make it tempting for the Fed to keep hiking until that goal is reached. The problem with doing so is that it risks throwing the baby (strong growth) out with the bath water (inflation), as a rate hike today remains contractionary long after the fight is won.

Good weekends, all …

Dana

——————————————————————————

Headline News

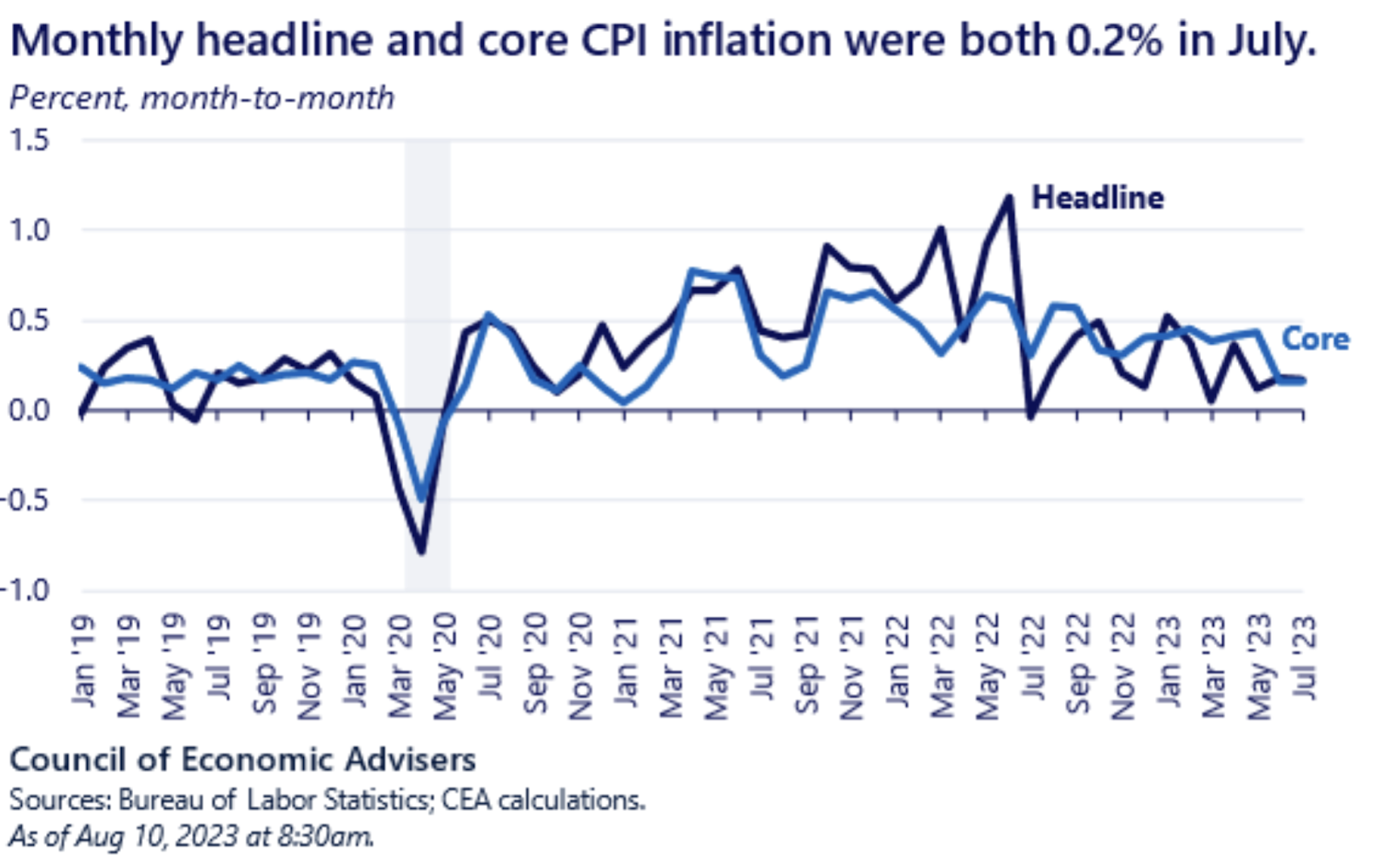

Inflation Still Moderate in July; Labor Market Resilient

Inflation remained moderate in July in a positive sign for the Fed before it decides the fate of interest rates next month. Yesterday’s consumer price index (CPI) data showed that consumer prices rose by 0.2 percent last month, consistent with the 0.1 percent and 0.2 percent month-on-month increases seen in May and June, respectively.

Consumer prices rose 3.2 percent over the 12 months through July. This is slightly above the 3 percent annual increase in inflation seen the month before, and marks the first increase in year-on-year inflation in 13 months. This slight increase is unlikely to raise concern from the Fed as it reflects the rapid pace at which inflation has fallen since July 2022, when the figure reached a four-decade high of 9.1 percent year-on-year, and should not be taken as a sign that the ongoing trend of sustained lower inflation may be in jeopardy.

Shelter costs represented the largest contributor – over 90 percent – to the monthly increase in prices. Energy prices increased by 0.1 percent last month, with gasoline prices rising by 0.2 percent and prices of household electricity falling by 0.7 percent over the month. Food prices rose by 0.2 percent in July.

Meanwhile, monthly core inflation was 0.2 percent in July, on par with the 0.2 percent increase in core CPI seen the month prior. Core CPI rose by 4.7 percent on an annual basis, a slight decrease from the 4.8 percent increase seen in June. This was the lowest level core CPI has reached since October 2021. Housing costs fueled about 40 percent of the increase in core CPI.

This week’s release of inflation data follows the release of the latest jobs report last Friday. The report showed continued strength in the labor market despite some signs of a slowdown, with nonfarm payroll employment increasing by 187,000 and unemployment clocking in at 3.5 percent in July. The report also revised down job growth in May and June by a combined 49,000 jobs.

The latest inflation and labor market data are positive signs for the Federal Open Market Committee (FOMC) ahead of their next meeting on September 19-20. The FOMC raised the federal funds rate by a quarter of a percentage point, bringing it to a 22-year high of 5.25 to 5.5 percent at their last meeting in July, and have suggested that a pause is possible depending on data released in the interim. The Fed will also be closely watching the August jobs report which will be released on September 1, ahead of its next decision.

Other Developments This Week

- Moody’s Downgrades Small and Mid-Sized Banks

On Monday afternoon, Moody’s announced its decision to downgrade the credit ratings of ten small and mid-sized banks and place the ratings of six additional lenders under review.

Downgraded firms include Commerce Bancshares, Inc., BOK Financial Corporation, M&T Bank Corporation, Old National Bancorp, Prosperity Bancshares, and Amarillo National Bancorp, while lenders including Bank of New York Mellon, Northern Trust Corporation, and Truist Financial were placed under review, signaling that a potential downgrade is possible in the near future. This brings the number of banks on downgrade review or with negative outlooks to over a dozen.

The credit rating agency cited several factors in its decision, including challenging conditions in the commercial real estate sector and the Federal Reserve’s tightening of monetary policy, which has left banks with significant unrealized losses that are not reflected in their regulatory capital ratios, and vulnerable to a loss in confidence by investors.

- Kanter and Khan Discuss Merger Guidelines

On Thursday, Chair of the Federal Trade Commission Lina Khan and Assistant Attorney General for the Antitrust Division in the Department of Justice Jonathan Kanter discussed their agencies’ recently released draft of updated merger guidelines. The draft represents one of the most important developments in antitrust law in over a decade.

Khan and Kantar spoke at American Economic Liberties Project’s virtual town hall. Khan stressed the FTC’s emphasis on hearing from the actual consumers, workers, and businesses affected by mergers in crafting the updated guidelines. The agencies gathered thousands of public comments and engaged in listening sessions to hear directly from market participants.

Kantar stressed that today’s market realities present differently than in the 1950s and 1960s, and that a timely update of guidelines requires first asking fundamental questions about how competition presents in today’s economy. They highlighted that anti-competitive market conditions do not only affect consumers through higher prices, but workers who may be forced to navigate unpredictable schedules by newly empowered employers, and businesses who may see costs go up due to suppliers increasing their prices.

The draft guidelines update the technical framework used to assess the effect of mergers on competition by laying out 12 clear ways that mergers can violate the Clayton Act, the statute that most directly addresses mergers.

The draft guidelines are open to public comment until September 18. The FTC and DOJ will then move towards finalization of the proposed guidelines.

- Paypal/Paxos stablecoin

On Monday, PayPal announced that it would be adding functionality within its site and app for PayPal USA, a stablecoin issued by Paxos. Paxos has said that the stablecoin will be backed by deposits, short term treasuries, and cash equivalents. PayPal users will be able to transfer units of the stablecoin to one another without fees, the same way current users can send dollars from their PayPal balance or bank account without fees. They will be able to buy other cryptocurrencies through PayPal’s built in crypto wallet for the same fees as users currently using their PayPal balance or bank account. PayPal will also allow users to pay for goods and services with PayPal USD, by first converting the PayPal USD into dollars and then giving those dollars to the merchant. This reads as more of a marketing stunt than a financial innovation, but the description of PayPal USD appears similar to that of a money market fund, only unlike money market funds that are regulated by the SEC, Paxos is regulated by the New York Department of Financial Services.

- Ohio Special Election Results

On Tuesday, Ohio Republicans’ attempt to amend their state constitution to require amendment referenda to receive a supermajority 60 percent of the vote failed spectacularly, rejected by 3.1 million voters by a 57-43 percent margin. This attack on the state’s democracy was aimed at preventing an upcoming November 2023 referendum enshrining abortion rights in the state’s constitution from being able to pass. Their purpose was twofold: to set a high enough threshold to protect their deeply unpopular six-week abortion ban, and to entrench Republican power in a state whose elected institutions have designed a system that gives them “significant advantage.”

Opposition to the referendum, which ran 19 points ahead of President Biden’s 2020 election results, bodes well for the upcoming November referendum. A successful campaign could prove to be the shot in the arm Sen. Brown (D-OH) needs in the lead up to his tight 2024 reelection bid, as organizers look to build on any momentum they gather.

Look Ahead

Monday, August 14th

- The Brookings Institution: The Resolution of Large Regional Banks and Lessons Learned with Martin Gruenberg

Wednesday, August 16th

- Minutes of July 25-26 FOMC Meeting

- Industrial Production and Capacity Utilization

- New Residential Construction report

Other Related Articles

- Update 710 — Econ. Policy Week in Review:Legislative Push in Run-up to August Recess

- Update 709 — Summer of Labor Discontent: What’s at Stake for Workers in the Strikes?

- Fed Rates, Crypto on Front Burner

- Fed Presses Pause; GOP Tax Bill Reported Out

- Update 741 — Fed Holds Rates; CPI 3.1%: (When) Can Fed Pivot from Long Pause?