The Fed’s almost two year campaign of high interest rates, painful medicine to fight the worst bout of inflation in 40 years, is proving out, impelling the Fed to hold interest rates at its current 5.25-5.50 percent range. Price increases fell again in November, led by moderation in the key energy sector — where the evidence should be the most obvious, at the gasoline pump for example, where prices eased by six percent, a factor in today’s Fed decision that we review below.

Markets roared in approval of the Fed’s decision today to hold interest rates steady and Jerome Powell’s comments this afternoon following the conclusion of the Fed meeting. The Dow rose by 1.4 percent and closed at a record 37,090.24, up over 500 points. The S&P 500 and Nasdaq also gained 1.4 percent, with 10-year Treasuries falling by 30 basis points after the Fed’s announcement. It is clear that market watchers broadly assume that interest rates have peaked over this cycle of hikes.

Best,

Dana

The Federal Reserve today projected three rate cuts in 2024 as the Fed has paused interest rates at the 5.25 to 5.50 percent range where they have been held since July.

A tight labor market, evident by a slight drop in unemployment last month from 3.9 to 3.7 percent, and increases in rents, medical care, and car insurance, suggest a mixed enough picture on prices that the Fed’s hoped-for soft landing still requires higher-for-longer rates in the short-to-medium term.

Recent data has cemented expectations that inflation will continue its trend downward. These optimistic indications pushed the Fed to pause interest rate hikes today as the central bank may finally be at or nearing the end of its cycle of rate hikes. The Fed also placed the prospect of a pivot to rate cuts in 2024 firmly on the table. With economic data showing a resilient economy in the face of aggressive hikes, the path to a soft landing seems all the more clear.

Fed Holds Rates Steady, Projects Cuts Next Year

The Fed has opted to hold the federal funds rate steady at the 5.25 to 5.50 percent range for the third consecutive time. The Federal Open Market Committee (FOMC) announced the interest rate pause following the conclusion of its final meeting of the year this afternoon.

The dominant question now is how long the Fed will opt to keep interest rates elevated before likely beginning to cut in the next year. Economic projections released by the FOMC following the meeting show that officials project the Fed will make roughly three cuts next year, bringing interest rates to 4.6 percent in 2024. Officials projected further cuts in 2025 and 2026.

The Fed has raised rates eleven times from near zero in early 2022 to its current range in its most aggressive series of interest rate hikes since the 1980s. Strong inflation and labor market data over recent months have inclined the Fed to extend its pause. Federal Reserve Chair Powell highlighted recent economic developments showing the impact of the Fed’s hikes as they continue to set into the broader economy. Growth has slowed substantially since the third quarter but remains strong. In the housing sector, where prices have driven inflation up in previous months, the Fed observes that activity has flattened out reflecting higher mortgage rates.

The labor market has remained remarkably resilient with unemployment remaining below four percent, job creation remaining strong, the supply of workers increasing, and the labor force participation rate moving up since last year. Even so, there are signs of cooling as nominal wage growth is easing and job vacancies have declined. Powell noted that a rebalancing of labor market pressures may ease upward pressure on inflation.

If inflation continues to trend toward the Fed’s two percent target in the coming months and additional signs of labor market cooling arise in subsequent data, the FOMC may be inclined to keep rates steady before moving to cut rates as early as the second quarter of 2024. It must be noted that the Fed has continued to insist that a higher-for-longer strategy is preferable to premature cuts. The Fed is highly unlikely to cut rates as aggressively as it increased them.

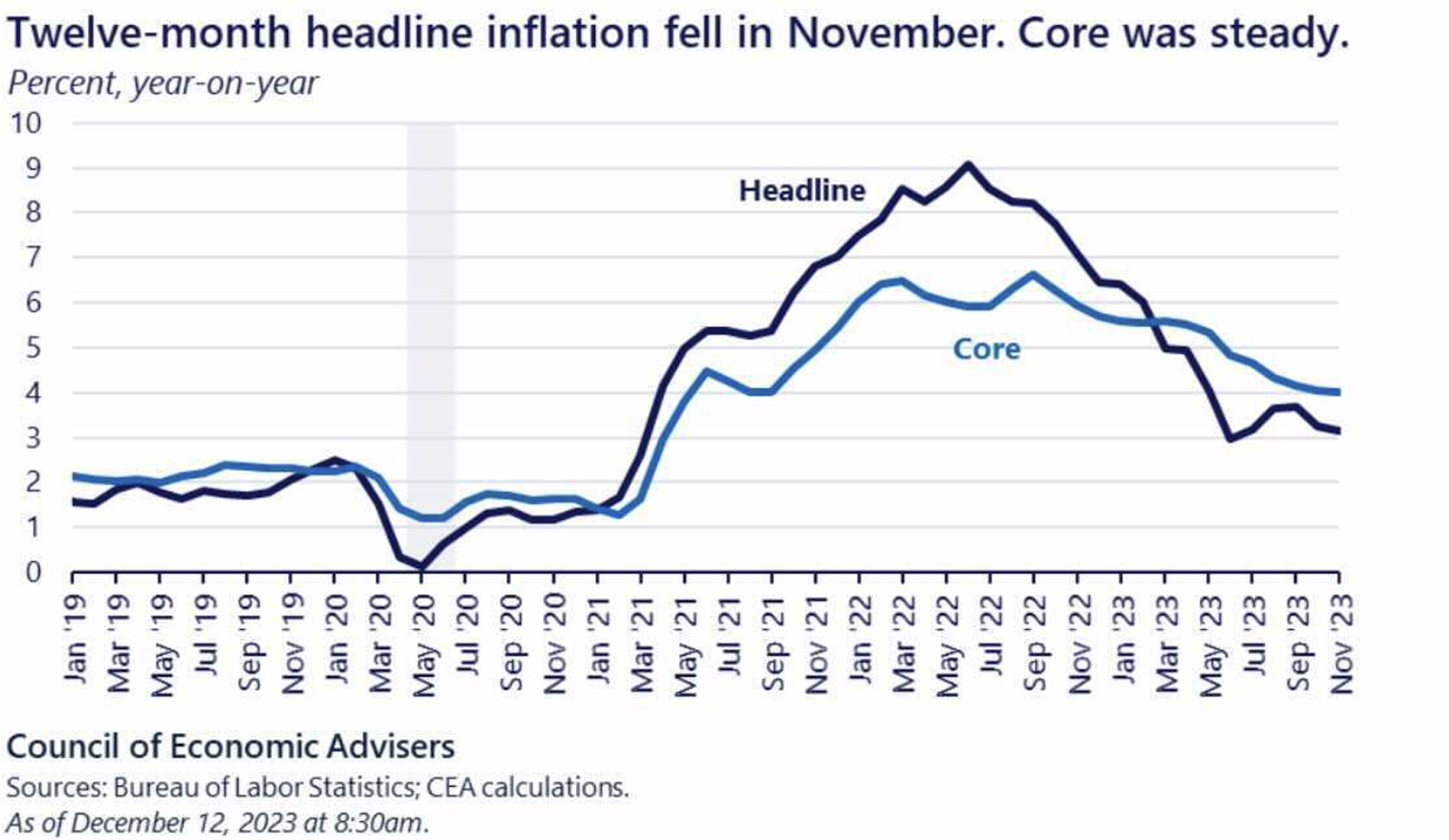

Inflation Continued to Cool Last Month

Consumer Price Index (CPI) data released yesterday showed inflation continuing to cool in November. Core CPI, which excludes food and energy prices, rose by 0.3 percent last month. This is consistent with 0.2 to 0.3 percent increases in core CPI during each of the prior five months. Core CPI remained flat on a year-on-year basis, on par with the 4.0 percent annual increase seen in October.

Headline inflation rose only slightly in November with prices rising by 0.1 percent over the month. On a yearly basis, prices rose by 3.1 percent, down from the 3.2 percent annual increase over the month prior, and roughly six points down from a peak of 9 percent reached in June 2022.

Source: Council of Economic Advisors

Indices that strongly contributed to the increase include:

- Shelter costs – Shelter costs ticked up by 0.4 percent in November, an annual increase of 6.5 percent. The shelter index was the largest factor in the monthly increase in core CPI, accounting for nearly 70 percent of the total increase. Housing inflation has remained stubbornly high and continued to have an outsized influence on inflation. Notably, the year-on-year increase in shelter costs has fallen from its peak early this year.

- Food prices – Food prices rose by 0.2 percent in November as prices of food away from home rose by 0.4 percent and prices of food at home rose by 0.1 percent. Meanwhile, prices of services excluding energy and housing rose by 0.4 percent.

Energy prices fell by 2.3 percent over the month as the prices of gasoline and fuel oil fell by 6 percent and 2.7 percent respectively. These negative contributions to the CPI were offset by increases in the natural gas index, which rose by 2.8 percent, and the electricity index, which rose by 1.4 percent in November. The path forward for energy prices remains uncertain as OPEC (Organization of the Petroleum Exporting Countries) has continued to cut oil production while production in other countries has remained strong.

Yesterday’s CPI data showed that specific deflationary trends watched for by the Fed are continuing. Producer price index (PPI) index data released by the Labor Department this morning further reinforced that inflation is trending down. Producer prices remained flat on a monthly basis and rose by 0.9 percent on an annual basis in November.

Inflation continues to trend toward the Fed’s two percent target and the causes of inflation in the first half of 2021 and early 2022 look on a sustainable path to further reduction. The Fed has been seeking such reassurance in making recent decisions. These trends were a positive sign for the Fed and likely reinforced officials’ decision to pause.

Likelihood of a Soft Landing Grows

With the strong data signaling economic resilience amid tightening conditions, a once tentative soft landing — in which a central bank raises interest rates enough to cool inflation without tipping the economy into recession — looks increasingly likely.

As the end of 2023 draws near, the American economy has experienced one of the strongest recoveries in the world with the labor market and growth remaining strong and inflation trending persistently downwards. If rates have reached their peak, the Fed’s path to such a landing seems all the more clear.

As Fed officials contemplate the end of its cycle of interest rate hikes and the period over which it will keep rates elevated, it is sure to pay close attention to upcoming data on inflation and the labor market. Officials will consider several data points before its next meeting. These include

- Estimated GDP growth during the third and fourth quarters of 2023

- December jobs report

- November and December personal consumption expenditure (PCE) price index data

- December CPI data

The FOMC will meet next on January 30 and 31.

The impact of recent rate hikes continues to ripple throughout the broader economy and appears poised to continue to unfold even as the Fed keeps rates elevated. Additional softening in the labor market is likely next year, which the Fed will be paying attention to as it monitors wage inflation.

The Fed’s projections of continued strong growth and labor market strength, and the fact that the Fed’s monetary policy has not yet produced a significant disruption to the economy’s recovery, provide an undeniable basis for tentative optimism.

Other Related Articles

- Update 740 — A Supplemental Surprise: Political Timelines vs. Actual Emergencies

- Update 739 — SCOTUS Seems Moore Unsure: Re Congress’ Authority to Tax Certain Income

- Update 738 — Immaculate Disinflation: Felt or Not, Prices Nearer Fed’s Target

- Update 737 — Undersupply and Costs: Problems Besetting the Housing Market

- Update 736 — Thanksgiving Leftovers: CR Signed; Room for December Items?