Update 701 – Economic Policy Week in Review

Fed Presses Pause; GOP Tax Bill Reported Out

The week saw the spectacle of a former president arraigned in the Federal District Court to enter a not guilty plea for his handling of classified documents. The field of GOP presidential candidates also grew this week, the size of which may be the former’s biggest political advantage.

Jerome Powell announced a suspension of the Fed’s year-long monetary policy campaign to halt inflation, pressing pause on his previously persistent rate hikes, as was expected. And the House Ways & Means Committee marked up and voted to approve a GOP package of tax cuts, a bold move given the party just drove the nation to the debt limit brink in the name of fiscal responsibility. These and the other economic policy highlights of the week are below.

Good weekends, all…

Dana

Topline News:

- Fed Pauses But Signals More Hikes This Year

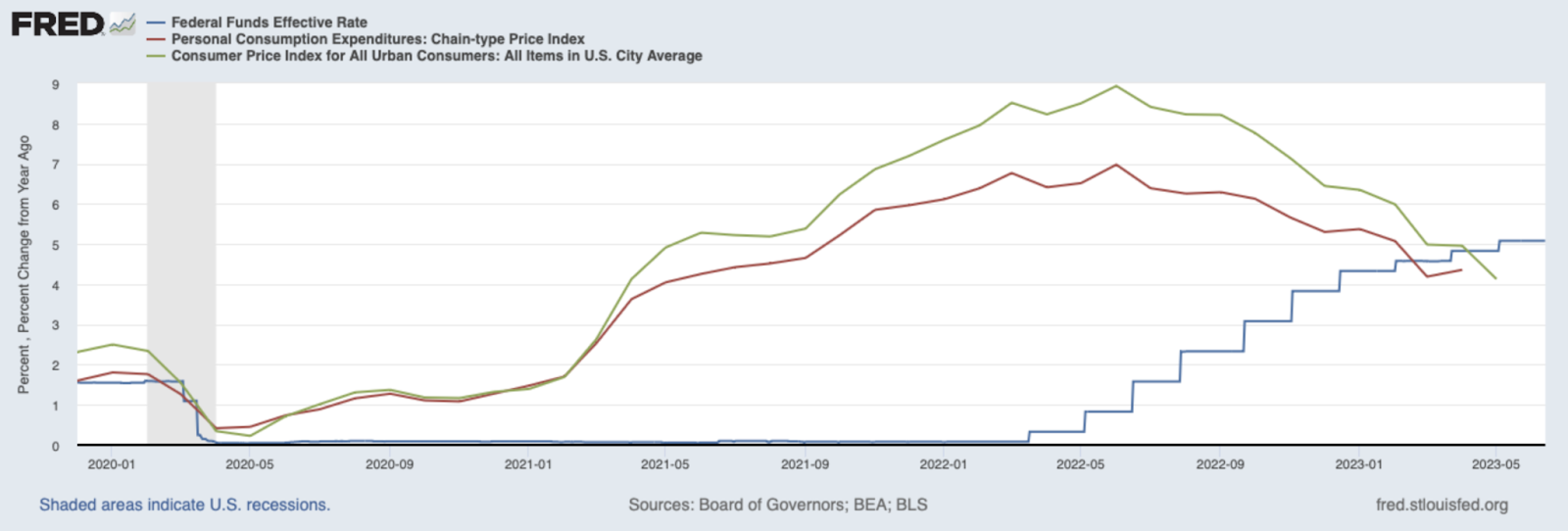

This week, the Federal Reserve finally paused its most aggressive series of interest hikes since the 1980s. The Federal Open Market Committee came to the decision at its June meeting on Tuesday and Wednesday. Following the meeting, Fed Chair Jerome Powell announced that after ten consecutive hikes that brought interest rates from near zero to the 5 to 5.25 percent range, the Fed would leave the current interest rate unchanged.

The Fed’s announcement comes after Tuesday morning’s consumer price index (CPI) data, which showed inflation continuing to moderate into May since the middle of last year. CPI rose 0.1 percent in May, a 4 percent increase from a year earlier. This represents the smallest annual increase since March 2021. Although inflation may be coming down, levels remain beyond than the Fed’s target of two percent. The most recent personal consumption expenditures (PCE) index data showed inflation increasing by 0.4 percent in April, a 4.4 percent increase from the year prior. This was up from a 0.1 percent increase the month before.

Federal Funds Rate, Personal Consumption Expenditures Index, and Consumer Price Index (2020 – Present)

A temporary pause before additional hikes at the FOMC’s remaining meetings this year will allow the Fed’s monetary policy – along with tightened credit conditions for businesses and households following the recent collapses of several mid-sized banks – to take effect. The impact of these on economic activity, hiring, and inflation are yet to become fully clear in economic data the Fed assesses in making its monetary policy decisions, and a temporary pause will give Fed officials an opportunity to reassess when it meets again on July 25-26 and on September 21-22.

The Fed’s decision to pause temporarily signals the central bank’s caution as it seeks to balance its dual mandate of controlling inflation and maintaining a strong labor market. May’s jobs report signaled that the job market has remained remarkably resilient in the face of the Fed’s action over the past 15 months, although unemployment has increased to 3.7 percent.

- House Ways and Means Marks Up Tax Bills

On Tuesday, the House Ways and Means Committee marked up the American Families and Jobs Act, a package of three Republican tax bills which we covered in more depth in Wednesday’s update. The three bills were all approved out of committee without a single Democratic vote.

Republicans also rejected a number of Democratic amendments. Ranking Member Richard Neal (D-MA) offered an amendment to exclude foreign research conducted in China from research and development tax benefits. Another offered by Congressman Don Beyer (D-VA) would have put guardrails on the Qualified Small Business Stock exemption to prevent a tax break aimed at encouraging investment in small businesses from becoming an unlimited giveaway to the ultrawealthy. Other committee Democrats put forward amendments to protect workers, tackle junk fees, and reduce the cost of accessing reproductive care, all of which were blocked by the majority.

The package, a starting point for Republicans in negotiations on a bipartisan tax bill, would renew a series of corporate tax breaks that had expired or will soon expire under the TCJA, along with a number of other provisions that would primarily benefit corporations, the wealthiest Americans, and foreign investors. According to analysis by the Institute for Taxation and Economic Policy, the richest one percent of Americans would receive an average of $16,560 in 2024; the poorest fifth would receive an average tax cut of just $40.

Hearings This Week:

- Chopra Stands Strong Against GOP Attacks

During his semi-annual report to Congress this week, Director Chopra defended the CFPB’s work in protecting consumers and businesses while minimizing regulatory arbitrage and adopting a holistic approach to consumer protection. Chopra emphasized the Bureau’s exclusive dedication to the well-being of American consumers.

In the Senate, Democrats led by Senator Brown (D-OH) highlighted the Bureau’s crucial work and dismissed unfounded attacks from Republicans and Wall Street that claim the Bureau’s actions hinder corporate enrichment at the expense of consumers.

- Senator Scott (R-SC) criticized the Bureau for unaccountable rule-making and the publication of blog posts with plain English explanations of regulatory policy. Director Chopra countered by highlighting that rules are made through regular processes and that small businesses appreciate the plain English explanations. Senator Tillis (R-NC) attacked the CFPB’s proposal to limit late fees, calling them an important source of countercyclical revenue.

- Senator Warren (D-MA) sought clarification, and Chopra confirmed that late fees represent a small portion of banking revenue but have a significant impact on consumers.

- Democratic Senators, along with Republican Senator Britt (R-AL), raised concerns about consumer protection from scams facilitated by generative artificial intelligence. Director Chopra acknowledged the insufficiency of current anti-fraud measures and pledged to work with authorities to safeguard American consumers.

- Senators Scott, Daines (R-MT), and Kennedy (R-LA) asked about a recent data breach. Chopra expressed concern about the brief but confirmed that no personally identifiable information had been compromised.

- Senator Van Hollen (D-MD) requested clarification on rent-a-bank schemes, and Chopra highlighted the Bureau’s ability to coordinate efforts and address regulatory evasion tactics across fragmented regulatory structures.

In the House, Republicans on the House Financial Services Committee objected to the Bureau’s practices, criticizing the director’s public guidance and funding mechanism they deemed unconstitutional. But no Republican supported nullifying rules based on this funding structure. Republicans criticized regulations that would prevent credit card companies from imposing unreasonable late fees and shifting the costs onto timely payers.

Director Chopra insisted these regulations would make credit card companies disclose their full costs and benefits, and provide transparency for consumers to make informed choices. Ranking member Waters (D-CA) emphasized the tradition of granting congressional leeway in funding decisions for executive branch agencies, and Rep. Beatty (D-OH) raised concerns about the potential chaos resulting from nullifying all existing CFPB rules if the Supreme Court deems the funding structure unconstitutional.

- House Appropriations Committee Begins Markups at FY22 Levels

This week, the House Appropriations Committee began full committee markups of Fiscal Year 2024 appropriations bills. These markups were originally scheduled to take place last month, but were postponed until after a deal on the debt limit was reached.

Chairwoman Kay Granger (R-TX) announced this week that Republicans would be moving forward with markups at deeper cuts than the compromise budget agreement specifies, drawing ire from the committee’s Democrats. House Republicans have been insisting that budget caps in the Fiscal Responsibility Act were a ceiling, not a floor — in clear conflict with the intention of the bipartisan agreement.

Full committee markups began with the Military Construction, Veterans’ Affairs, and Related Agencies bill, which cuts funding for military construction and includes a number of partisan riders, primarily related to culture war issues. The bill was approved by the Committee along party lines.

The Committee also approved the Agriculture bill on a party line vote Wednesday. The full committee then began considering the majority’s 302(b) allocations, which total roughly $1.47 trillion, $119 billion lower than the levels set out in the bipartisan agreement. The committee was unable to complete work on the allocations until Thursday morning, when the allocations were approved with every Democrat voting against.

- Secretary Yellen Faces House Financial Services

On Tuesday, Treasury Secretary Janet Yellen testified before the House Financial Services Committee in a hearing focused on international financial institutions. Representatives on both sides of the aisle took the opportunity to discuss a broad range of issues, including the recent debt ceiling standoff. Republicans insisted that the Treasury Department failed to provide sufficient transparency around its determination of the “X-date” and extraordinary measures taken to avoid default ahead of the bipartisan deal to suspend the debt limit through 2025.

Both Democrats and Republicans expressed concerns about the strength of small- and medium-sized banks in the aftermath of recent bank failures and subsequent deposit flight and growth of “too big to fail” banks. Secretary Yellen defended the Treasury and regulators’ action to avert a crisis in the days after Silicon Valley Bank failed and the bidding process through which JP Morgan Chase’s acquisition of a majority of assets and certain liabilities of First Republic Bank following its collapse was finalized.

The Secretary’s recent comments suggesting that additional mergers may occur, as stocks of some banks remain under pressure, have faced criticism from progressive advocates including 20/20 Vision. The trend of consolidation in the banking sector amidst a lack of strong merger guidelines increased the systemic risk of this year’s bank failures. Further consolidation reinforces an underlying problem rather than presents a solution.

Committee Republicans, including Representative Frank Lucas (R-OK), also targeted increased capital requirements for banks that are expected to be proposed by the Federal Reserve in the coming months. Yellen highlighted that capital requirements for banks of the failed Silicon Valley Bank’s size were rolled back in the years ahead of its failure.

- HFSC Pushes Ahead on Digital Asset Agenda

On Tuesday, June 13th, House Financial Services convened for a full committee hearing to explore regulation around the digital asset marketplace – their 6th full committee hearing on this topic to date. To little surprise, House Republicans and their respective witnesses used the hearing to highlight their digital asset agenda and offer potential pathways forward for the rapidly evolving industry. The hearing spotlighted two key pieces of legislation, the first on stablecoins, penned by Chair Patrick McHenry (R-NC) and the second on a market structure bill jointly penned by McHenry and House Ag Committee Chair Glenn Thompson (R-PA).

- Stablecoin Bill:

Ahead of Tuesday’s hearing, House Republicans released a third version of their stablecoin bill in efforts to reconcile a few differences that Democratic lawmakers had expressed concerns over. The notably shorter draft is intended to serve as another step forward in finding consensus among the polarizing parties and is meant to instill guardrails around the stablecoins following an undoubtedly tumultuous year.

Last month, Democrats were particularly agitated when the House GOP released what they claimed to be a bipartisan bill, and in turn released their own version with a few stark differences. On Tuesday, however, the tone seemed to have changed. Ranking Member Maxine Waters (D-CA) voiced her eagerness to return to the negotiating table and get legislation in the books once and for all. For now, the two parties remain far apart, but arguably closer than they’ve ever been.

- Market Structure Draft Discussion:

In addition to their stablecoin bill, the GOP showcased their Digital Asset Market Structure Discussion Draft. Waters has repeatedly referred to the 162-page bill as “highly complex” and a product that would essentially “overhaul our nation’s capital markets.” Democrats remain extremely cautious in this realm and utilized the hearing to identify all the innate flaws woven throughout the bill, including but not limited to its language over securities laws and broker dealers.

While there has yet to be a formal timeframe put in place, Rep. McHenry announced that he intended to markup the stablecoin bill – or some variation of it – shortly after July recess. 20/20 Vision remains hopeful that House Democrats, and their Senate companions, will stand firm in any negotiations brought on and uphold the values and consumer protections that our traditional securities laws have afforded the investor community for decades.

The Week Ahead:

Both the House and Senate will be in session next week, and all eyes will be on Jerome Powell as he delivers the central bank’s semi-annual monetary policy report before both chambers. Powell is widely expected to offer a preview as to what’s to come in terms of rate hikes throughout the rest of the year. Additionally, Sherrod Brown (D-OH) announced he would host a markup on the Recovering Executive Compensation Obtained from Unaccountable Practices (RECOUP) Act, following the fallout of Silicon Valley Bank. The bill is said to give bank regulators stronger authority to claw back incentive-based pay, among other things.

Wednesday, June 21:

- House Financial Services: “The Federal Reserve’s Semi-Annual Monetary Policy Report”

- Senate Banking Committee: Markup of the Fentanyl Eradication and Narcotics Deterrence (FEND) Off Fentanyl Act and the Recovering Executive Compensation Obtained from Unaccountable Practices (RECOUP) Act

- Senate Banking Committee: “Nomination Hearing”

Thursday, June 22:

- House Financial Services Oversight & Investigations Subcommittee: “Oversight of the SEC”

- Senate Banking: “The Semiannual Monetary Policy Report to the Congress”

Other Related Articles

- Update 715 — Weekly Economic Roundup

- Update 710 — Econ. Policy Week in Review:Legislative Push in Run-up to August Recess

- Update 709 — Summer of Labor Discontent: What’s at Stake for Workers in the Strikes?

- Fed Rates, Crypto on Front Burner

- Update 741 — Fed Holds Rates; CPI 3.1%: (When) Can Fed Pivot from Long Pause?