Update 389 — Recessionary Indicators, Pt. 1

What the Economic Tea Leaves Say Today

Over the next two updates, we will look at macroeconomic indicators of the end of the current post-crisis expansion — leading vs. lagging, from coal mine canaries, to red herrings, to black swans.

The political implications of an economic reversal of fortune could be sizable, in electoral terms but also in economic policy outcomes, many of which were hinted at in last night’s Democratic presidential debate in Ohio. The causes, timing, geographical and sectoral location, and severity of any such reversal intimated by the indicators will color next year’s vote.

What do the tea leaves say today about the economy 12 months out?

Best,

Dana

————

At the beginning of each month, government entities and private market participants release a trove of data points pertaining to the state of the national economy. These include all-important unemployment figures, wage growth, retail sales, and more. Data from September gives the impression of an economy running smoothly, with other economic variables now signaling trouble on the horizon.

In our first of two perspectives on trends and indicators, we review an inventory of the leading macroeconomic indicators and what they mean for the trajectory of the economy. In the next update, we will look at not at the forecast but at what the lagging and coincident indicators are already signaling — can anything be gleaned, and are we heading for a recession?

Leading Indicators: Flashing Red

- Manufacturing: Last Tuesday, the Institute of Supply Management published its September Manufacturing Purchasing Managers’ Index (PMI) reading coming in at 47.8 percent — the lowest since 2009 and down from 49.1 percent in August. The ISM index is a widely-used indication of economic trends in the manufacturing and service sectors and a reading below 50 percent indicates a contraction in business activity. Manufacturing accounts for a small fraction of the domestic economy — around 11 percent — but weakness in this area can be signal. This slowdown in business activity in the sector was reflected in Friday’s manufacturing jobs number that showed a negative 2,000 month-over-month change.

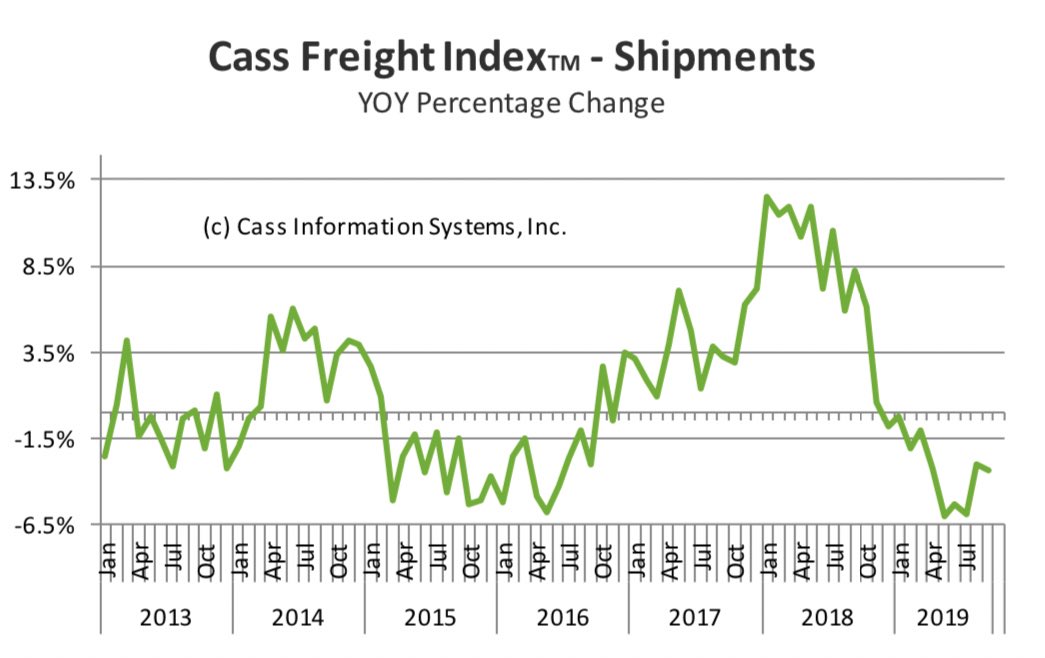

- Cass Freight Index: This week, the Cass Freight Index, a lesser-known but critical barometer of the overall shipping and haulage industry that measures aggregate U.S. freight delivery volumes, recorded its tenth consecutive month of annual shipment declines for September. The index turned negative in December 2018, and September shipments showed a 3.4 percent decline year-over-year. The index has gone negative before without leading to an economic contraction, but ten consecutive months of negative shipments have some market observers concerned: “the shipment index has gone from ‘warning of a potential slowdown’ to ‘signaling an economic contraction,’” wrote Donald Broughton, the September Cass Freight Index Report’s author.

Source: Cass Freight Index Report

Leading Indicators: Flashing Yellow

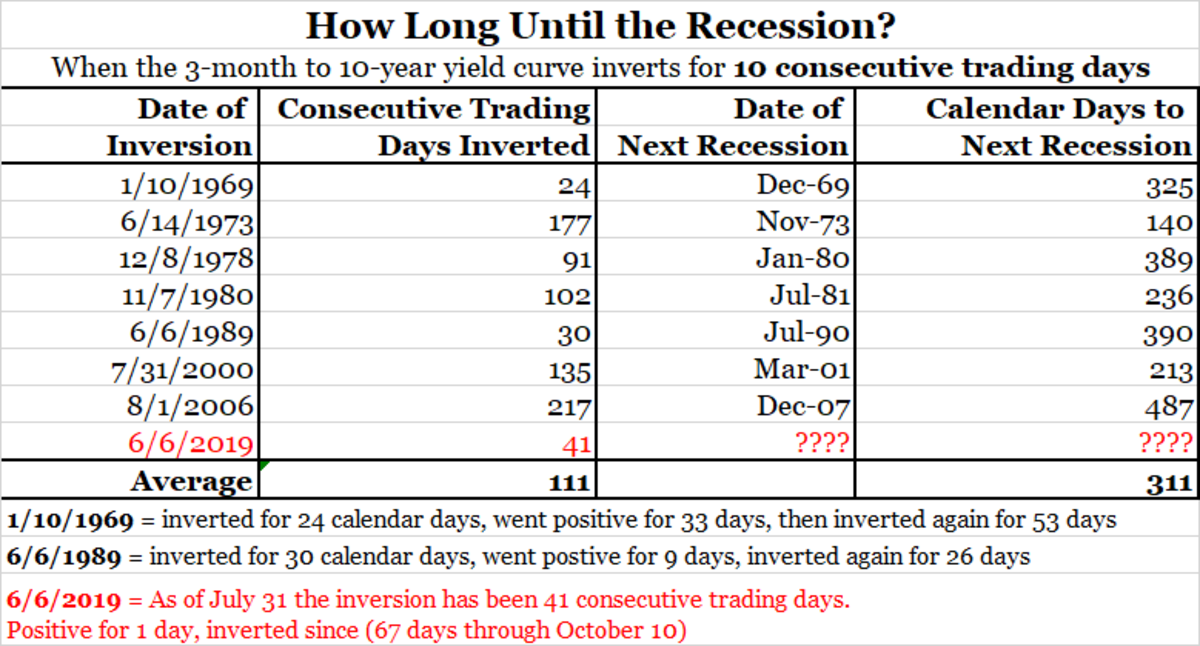

- Bond Market: We have covered the signal of the yield curve a number of times in recent updates as it is a reliable leading indicator of recession. The most closely watched measures of the yield curve are the differences between the yield on the 3-month Treasury bill and the 2-year Treasury bond versus the 10-year bond yield. Last week, the 3-month/10-year curve reverted to its normal upward slope, but some market participants are wary of saying that the bond market is no longer predicting a recession, in part because the 3-month/10-year yield curve was inverted for longer than preceded previous recessions.

Source: Bloomberg

- Weekly Hours: Per the BLS, nearly 59 percent of the American workforce are hourly workers. A drop in weekly hours is a leading indicator of a recession, as employers are likely to reduce worker hours before laying them off. A reduction in hours also has a compounding effect on the economy, as workers whose hours are cut get smaller paychecks which reduces their spending potential.

The average hours worked for production workers has stayed relatively consistent during the recovery, hovering around 42 hours per week, rising to a high of 42.4 hours per week in April 2018, but the sector has seen a precipitous decline since then, falling to 41.5 last month — the lowest since January 2014. In addition, the average workweek in the private sector as a whole has dipped to 34.3 hours in July, down from 34.5 hours in March — the lowest level and largest decline since early 2017.

Leading Indicators: Holding Steady

- Consumer Confidence: Consumer spending makes up about 70 percent of the US economy, so it follows that when confidence is low, a recession is not far behind. Traditionally, consumer confidence falls sharply about three months before a recession hits. Per the University of Michigan, consumer sentiment rose to 92 in September from 89.8 in August. Despite the positive headline figure, 38 percent of consumers expressed concerns about the negative impact of tariffs, the highest percentage since March 2018. As trade tensions continue to cast a shadow over the economy, consumers may only get more skittish over trade issues as the holiday season fast approaches.

- Corporate Earnings: Corporate profit margins are a good leading indicator of the business cycle because they are reflective of underlying aspects of the economy. Narrowing profits can also result in decreased capital investment and hiring in the future. So far, margins for large-cap companies are showing resilience to much of the geopolitical uncertainty and trade tensions, but margins for small-to-medium-size businesses are feeling the strain, per the BEA’s National Income and Product Accounts (NIPA) profit margins report. 77 percent of Americans are employed by firms with fewer than 500 workers. If margins at these firms continue to be squeezed, layoffs may ensue, having ripple effects throughout the rest of the economy.

- Capital Markets: The big indexes — S&P 500 and the Dow Jones — recently reached record highs since the stock market rallied from its December lows. But percentage gains this year conceal the fact that the indexes are actually little changed since this time last year. The markets are one of the more consistently referenced indicators by the president as a gauge on how well the economy is doing.

The markets recovered since the Fed changed its direction on interest rate hikes, but trade war headlines and developments have created a substantial amount of volatility in recent months. While the stock market plays an important role, it is not as linked to the real economy as one might think. What to watch for: before a sustained contraction in the economy, the equity market will likely experience a substantive decline, in the order of 20 percent or more.

No Black Swan Around, But Troubles Abound

High-frequency data that show monthly and weekly changes in the economy can often be misleading as to grander conclusions about the direction of the overall economy. But some of the incoming data show weakening in key sectors like manufacturing and agriculture and paint a not-so-rosy picture of the rest of the economy. Some market observers are already ringing alarm bells.

In the next update, we will take a look at what some of the other coincident and lagging macroeconomic indicators are telling us about short-term and long-term economic growth. Are any of these indicators showing their cards at this stage in the cycle, and are there any takeaways as we approach November, the beginning of the one-year presidential election countdown?

Other Related Articles

- Update 735: Shutdown Threat In Temporary Remission

- Update 729 — House Elects Speaker: Can Bipartisan Fiscal Policy Follow?

- Update 728 — Suspended Animation:House Left Behind as the World Turns

- Update 722 — From Strikes to Shutdown: Challenges to the Post-Covid Recovery

- Update 720 — Weekly Economic Roundup

http://gcialisk.com/ – cialis reviews

It’s not my first time to visit this web site, i am browsing this site dailly and obtain nice data from here all the time.

asmr 0mniartist

I’d like to find out more? I’d like to find out some additional information. 0mniartist asmr

Excellent way of telling, and nice paragraph to obtain facts regarding my presentation subject matter,

which i am going to convey in academy. asmr 0mniartist

Wonderful beat ! I would like to apprentice while you

amend your website, how could i subscribe for a

blog website? The account helped me a acceptable deal.

I had been tiny bit acquainted of this your broadcast offered bright

clear concept 0mniartist asmr

online dating

dating

Heya i am for the first time here. I came across this

board and I find It truly useful & it helped me out much. I hope to give something back and help others like you

helped me.

We are a group of volunteers and starting a new scheme

in our community. Your website offered us

with valuable info to work on. You have done an impressive job and our

entire community will be thankful to you.

Hello! Someone in my Facebook group shared this site with us so I came to check it out.

I’m definitely loving the information. I’m bookmarking and will be tweeting this to my followers!

Exceptional blog and wonderful style and design.

That is a great tip especially to those new to the blogosphere.

Short but very accurate information… Thank you for sharing this one.

A must read post!

tider , tider

tinder app

What’s up friends, good piece of writing and pleasant arguments

commented here, I am in fact enjoying by these.

What’s up Dear, are you genuinely visiting this website regularly, if so after that

you will without doubt obtain pleasant know-how.

Hey there! Do you know if they make any plugins to assist with Search Engine

Optimization? I’m trying to get my blog to rank for some targeted keywords

but I’m not seeing very good success. If you know of any please share.

Thank you!

Simply wish to say your article is as amazing. The clarity in your post is just spectacular and i can assume you’re

an expert on this subject. Fine with your permission let me to

grab your feed to keep up to date with forthcoming post.

Thanks a million and please carry on the rewarding work.

Wonderful site you have here but I was wondering if you knew of

any forums that cover the same topics talked about here?

I’d really love to be a part of community where I can get feedback from other experienced people that share the same interest.

If you have any recommendations, please let me know. Thank

you!

Aw, this was an exceptionally good post. Taking the time and actual effort to produce a very good article… but what can I say… I procrastinate a whole lot and never seem to get nearly anything done.

tindr , tider

tinder online

tinder app , what is tinder

http://tinderentrar.com/

scoliosis

Good blog you’ve got here.. It’s difficult to find excellent writing like yours nowadays.

I seriously appreciate people like you! Take care!!

scoliosis

scoliosis

Hi there, i read your blog from time to time and i own a similar one and i was just curious if

you get a lot of spam responses? If so how do you prevent

it, any plugin or anything you can recommend?

I get so much lately it’s driving me mad so any assistance is very much appreciated.

scoliosis

scoliosis

This blog was… how do I say it? Relevant!! Finally I have

found something that helped me. Many thanks! scoliosis

dating sites

Pretty section of content. I just stumbled upon your blog and in accession capital to assert that

I acquire actually enjoyed account your blog posts.

Anyway I will be subscribing to your augment and even I achievement you access consistently

fast. free dating sites https://785days.tumblr.com/

dating sites

Wow, this post is fastidious, my sister is

analyzing these kinds of things, thus I am going to inform her.

free dating sites

Hey there! I could have sworn I’ve been to this website before but after browsing

through some of the post I realized it’s new to me. Anyways, I’m definitely delighted I found it and I’ll be book-marking and checking back often!

This article will assist the internet people for

creating new weblog or even a blog from start to end.

Keep on writing, great job!

Whats up this is kind of of off topic but I was wondering if

blogs use WYSIWYG editors or if you have to

manually code with HTML. I’m starting a blog soon but

have no coding knowledge so I wanted to get advice from someone with experience.

Any help would be enormously appreciated!

I am really impressed with your writing skills

as well as with the layout on your blog. Is this a paid theme or

did you customize it yourself? Either way keep up the nice quality

writing, it’s rare to see a nice blog like this one nowadays.

Article writing is also a fun, if you be familiar with

afterward you can write or else it is difficult to write.

You actually make it seem so easy with your presentation but I find this matter

to be really something that I think I would never understand.

It seems too complex and extremely broad for me. I’m looking forward for your next

post, I will try to get the hang of it!

I love your blog.. very nice colors & theme. Did you design this website yourself or did you hire someone to do it for you?

Plz reply as I’m looking to design my own blog and would like to know

where u got this from. kudos

Asking questions are genuinely nice thing if you are not understanding something completely, but this article presents

nice understanding yet.

Howdy! This article could not be written much better!

Looking through this post reminds me of my previous roommate!

He always kept talking about this. I will forward this article to him.

Pretty sure he’s going to have a very good read. Thanks for sharing!

cheraman kadhali book free download Codec Adobe After Effect Gratuitement book graphiste mise en page

7 Day To Day Jeton De Casino Trouv E Epiphone Casino Nut Width Quelle Est La Date D Ouverture Du G Ant Casino De Toulouse

Casino Berthelot Traiteur Casino De Paris Premier Rang Fallout 76 Unlock More Character Slots

dating sites free no registration

free senior dating sites

dating sites for gay trans men

rural gay dating

gay dating in qatar

can you take prozac and viagra generic viagra overnight delivery – what’s the least expensive place to buy viagra

Pingback: keto icecream

You actually make it seem so easy with your presentation but I find this topic to be really something which I think I would never

understand. It seems too complicated and extremely

broad for me. I’m looking forward for your next post, I will try to get the hang of it!

online free gay dating

gay men dating service

gay male fetish dating

Hi! I’ve been following your blog for a long time now and finally got

the bravery to go ahead and give you a shout out from Humble

Texas! Just wanted to tell you keep up the fantastic

job!

top rated gay dating sim

gay dating boston

tall gay men dating

gay online dating

obsessive boyfriend gay dating

gay teen sex dating games