The slumping U.S. housing market wallows in a 13-year-low in existing-home sales amid record high prices due to constrained supply and mortgage rates, now at a 22-year high. The Wall Street Journal reported today that home prices hit a record level in September, pushing homeownership further out of reach for an increasing number of Americans who will not enjoy the benefits and security of building home equity anytime soon. How long will this housing affordability crisis last? What can policymakers do about it, and will they?

Housing and homeownership stand at the heart of the economy as well as the American Dream. Today, we look at the difficulties besetting the housing market, the short-term prospects for the market, and longer-term solutions to the chronic aspects of the crisis in housing under discussion.

Best,

Dana

The Centrality of the Housing Market

The housing market accounted for 16.2 percent of the national GDP in 2022. Housing costs represent the largest category of household spending with an average of 33.3 percent of consumer expenditures in 2022, an annual increase of 7.4 percent. Such high housing expenditures mean less disposable income and less consumer spending overall. Over the last decade, the typical homeowner became 40 times wealthier than they would have been had they remained renters. This reduces wealth accumulation for non-homeowners who miss out on home equity and has generated inequality, given that people of color and other historically underserved communities have lower rates of homeownership. 73 percent of non-Hispanic white Americans are homeowners, as compared to 42.1 percent of Black Americans and 47.5 percent of Hispanic or Latino Americans. At the lower end of the income scale, we see increased homelessness. 582,462 people experienced at least one night of homelessness in America in January 2022, up from 551,000 five years ago, with 22 percent chronically homeless, and a shocking share – 28 percent – including families with children. The rate of unsheltered homeless individuals, those whose primary nighttime residence is not suitable for human habitation, rose from 34.5 percent of all homeless individuals in 2017 to 40.1 percent in 2022. Building housing and helping the unhoused access it has proven successful in Houston and elsewhere. Other localities, as well as the federal and state governments, should consider this model.

Conditions in the Housing Market(s)

The housing market encompasses several markets, all of which suffer from their own problems. They include:

The Existing-Homes and New Homes Market

Existing single-family homes have become increasingly out of reach for the average American. In October, the median existing-home sales price rose to $391,800, a 3.4 percent annual increase and a record high. Monthly payments for principal and interest rates on a median-priced home surpassed $2,500, a 94 percent increase in just two years. With the overall median household income at $74,580 for 2022, homeownership is an unattainable dream for more and more Americans.

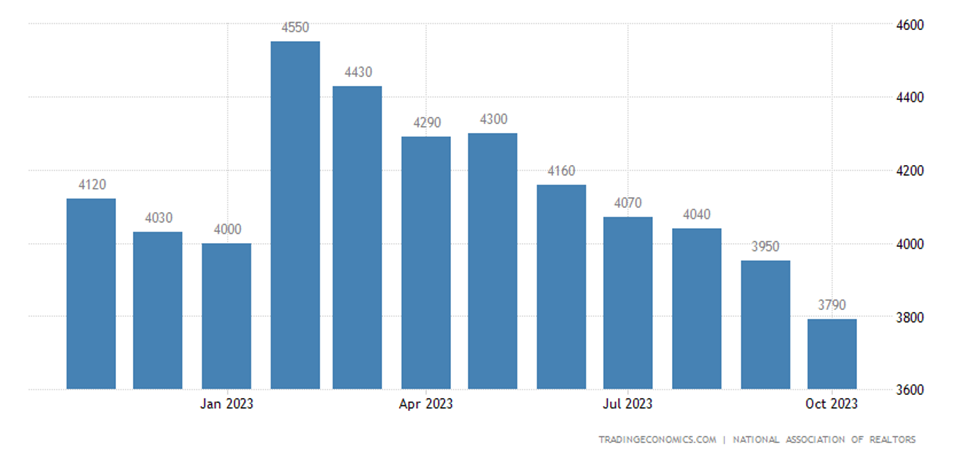

It is unsurprising that more Americans are losing interest in buying a home, with 85 percent of Americans saying it’s a bad time to do so, the highest rate since 1982. Existing-home sales fell to 3.79 million in October, down 14.6 percent from a year ago, reaching a 13-year low. New single-family home sales fell to 679,000 in October, down 5.6 percent from September, though 17.7 percent higher from October 2022.

Existing-Home Sales (by thousands)

Source: Trading Economics

The main culprit behind the current slump in sales is the recent jump in mortgage rates, which reached a 23-year peak of nearly 8 percent in October, up from less than 4 percent in 2020. This correlates with the Federal Reserve’s decision to hike interest rates beginning in March 2022.

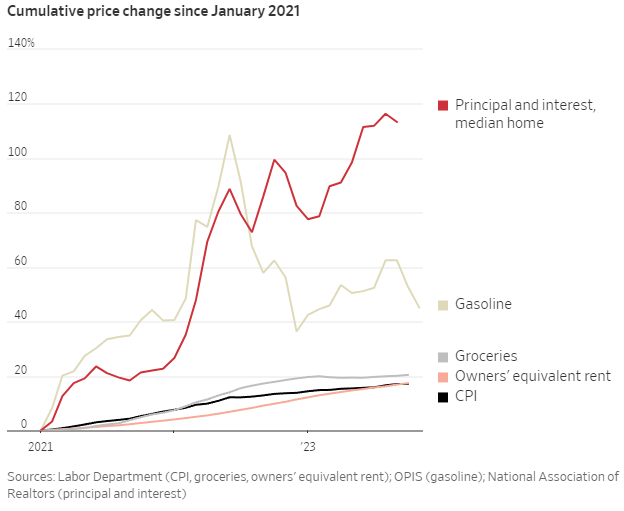

The housing market is also beset by underlying inflation. Since January 2021, home prices have risen 29 percent, almost double the core consumer price index increase of 15 percent over the same period. Additionally, current homeowners who locked in lower mortgage rates before the Fed started hiking interest rates are deferring plans to move, reducing supply by keeping these homes off the market.

Source:Wall Street Journal

The Rental Market

Rising homeownership costs are driving many would-be home buyers out of the purchasing market entirely, boosting the number of renters. Increased demand for rental properties has consequently driven rents up. Year-over-year increases in rent peaked at 16 percent in February of 2022 and remained at 7.2 percent as of October — nearly double the rate of inflation. This cost now accounts for 40 percent of renters’ core spending, an annual increase of 6.7 in October. Last month, low-to-moderate income renters, nearly 70 percent of all renters, spent an average of around 40 percent of their incomes on rent. In comparison, for an affordable house, housing expenditures should cost 30 percent or less of a household’s income. So even many families that choose not to buy homes find themselves especially “cost-burdened” by high rent prices. To reduce rental costs generally, it is imperative that localities approve the construction of new units, as recent research underscores.

The Construction Market

There is a housing supply shortage in the U.S., with 1.15 million unsold units at the end of October, up from 860,000 unsold units in January 2022. New home construction is also down from a year ago, with building permits issued in October decreasing at an annualized rate of 4.4 percent to 1,487,000.

Additionally, inflation bears heavily on housing construction costs. Building material costs have increased by 37.7 percent since 2020, with construction labor costs also increasing. The rise in construction costs is further compounded by:

- a lack of developable land.

- zoning restrictions, with about 75 percent of land in most US cities reserved for single-family detached homes, prohibiting the construction of apartments and other multifamily units.

- continuing supply chain issues from the pandemic.

- burdensome permitting processes.

New home construction is expected to pick up as the construction industry recovers from the pandemic and as lower mortgage rates increase the number of available buyers, but this will likely be a slow process. The National Association of Home Builders is projecting a five percent increase in single-family housing starts in 2024.

Action and Options in the Policy Landscape

Recent Executive Action

In late October, the Biden Administration took steps to alleviate housing shortages in major cities, announcing an initiative to help accelerate the conversion of commercial real estate to residential real estate. Office vacancy rates reached 17 percent nationally in June 2023, with cities such as San Francisco as high as 31 percent. Under the initiative:

- The Department of Transportation will provide $35 billion in lending for developing residential real estate with easy access to transportation.

- HUD will update the Community Development Block Grant fund to include “the acquisition, rehabilitation, and conversion of commercial properties to residential uses and mixed-use development.”

In mid-October, the Biden Administration announced a plan to strengthen homeownership, proposing $16 billion for the Neighborhood Homes Tax Credit as well as a $10 billion down payment assistance program for first-time homebuyers whose parents do not own a home.

Key Legislative Proposals

While Democrats and Republicans tend to be far apart when it comes to solutions to the housing crisis, some legislation has garnered bipartisan support:

- S. 657, the Neighborhood Homes Investment Act (NHIA) of 2023, introduced by Senators Ben Cardin (D-MD) and Todd Young (R-IN) would create tax credits for developers, lenders, and local governments to develop or rehabilitate homes to be sold to lower- or middle-income families. The NHIA has support from the housing industry as well as housing advocates, including the National Urban League and the Local Initiatives Support Corporation.

- S. 1257, the Family Stability and Opportunity Vouchers Act of 2023 introduced by Senators Chris Van Hollen (M-MD) and Todd Young (R-IN), would add 500,000 to the currently 5 million housing voucher usersrs over five years for low-income, high-need families with young children. It has support from housing and civil rights advocates including the NAACP, the National Alliance to End Homelessness, and the National Low Income Housing Coalition.

Both bills face steep challenges ahead as an election year approaches and risk being crowded out in a congested Congressional agenda.

Regulatory Changes

Some federal agencies have moved on their own to address the housing crisis. A recent Federal Housing Finance Agency (FHFA) report outlined a new set of proposed rules and guidelines for the Federal Home Loan Bank (FHLB) system. FHFA seeks to return the FHLB system back to its original purpose, supporting housing and community development.

In addition, the FHFA stated that it would increase the maximum size of home mortgage loans eligible for backing to $1,149,825 next year for high-cost markets such as California and New York, up from $1,089,300 this year. For lower-cost markets, the maximum would rise to $766,550, up from $726,200 this year.

Light at the End of the Tunnel?

Despite the many challenges facing the housing market, some relief is in sight: after reaching a high of nearly 8 percent in late October, rates for 30-year fixed mortgages fell to 7.29 percent in the week of November 22, marking the fourth consecutive week that mortgage rates have fallen. This is still more than twice the 3 percent mortgage rates seen just two years ago, but a significant reversal is likely to continue.

This decline in mortgage rates arises as the Fed has paused on raising interest rates since July, holding to the target range of 5.25 to 5.5 percent. The federal funds rate indirectly fuels mortgage rate increases by raising borrowing costs for banks, affecting every market including housing. If the Fed pauses its series of rate hikes, mortgage rates will ease.

Lawrence Yun, the chief economist for the National Association of Realtors, predicted that mortgage rates will drop to between 6 and 7 percent by Spring 2023. But mortgage rates are not expected to decline quickly, and few economists expect them to fall below 5 percent. Monthly mortgage payments are expected to decline with mortgage rates, which will come as a relief to mortgage holders who, as of October, were paying $2,012 in median monthly payments. The housing market will likely have to accept that the era of inexpensive mortgages is over and adjust accordingly.

The decline in inflation will also alleviate rent prices and slow the growth of home prices. Affordability depends most of all on Americans’ incomes rising at a faster rate than home values. This process would take years and will likely be hindered until income growth once again surpasses the rate of inflation.

Despite promising signs of short-term improvements in the housing market, the affordability crisis will continue in the face of chronic undersupply. Policymakers at the federal, state, and local levels must address the housing shortage, the lack of access to affordable dwelling units, and barriers to the construction of affordable homes. There are simple solutions to many of these problems, some of which even have bipartisan support such as modifying housing tax credits and improving land use regulations. But these solutions require the political will to enact and implement them; barring that, it is unlikely that the problems facing the housing market will abate anytime soon.

Other Related Articles

- Update 741 — Fed Holds Rates; CPI 3.1%: (When) Can Fed Pivot from Long Pause?

- Update 740 — A Supplemental Surprise: Political Timelines vs. Actual Emergencies

- Update 739 — SCOTUS Seems Moore Unsure: Re Congress’ Authority to Tax Certain Income

- Update 738 — Immaculate Disinflation: Felt or Not, Prices Nearer Fed’s Target

- Update 736 — Thanksgiving Leftovers: CR Signed; Room for December Items?