Update 747 — The Week in Retreat:

Reversals on Budget, Inflation, Crypto

The week opened with one step forward, as Hill leaders finally agreed on FY24 budget targets totaling $1.59 trillion on Sunday, only for House GOP hardliners to demand a renegotiation of the deal on Thursday, leaving Speaker Johnson with no clear route forward and only one week left before hitting a partial federal government shutdown deadline, three weeks before a total government shutdown.

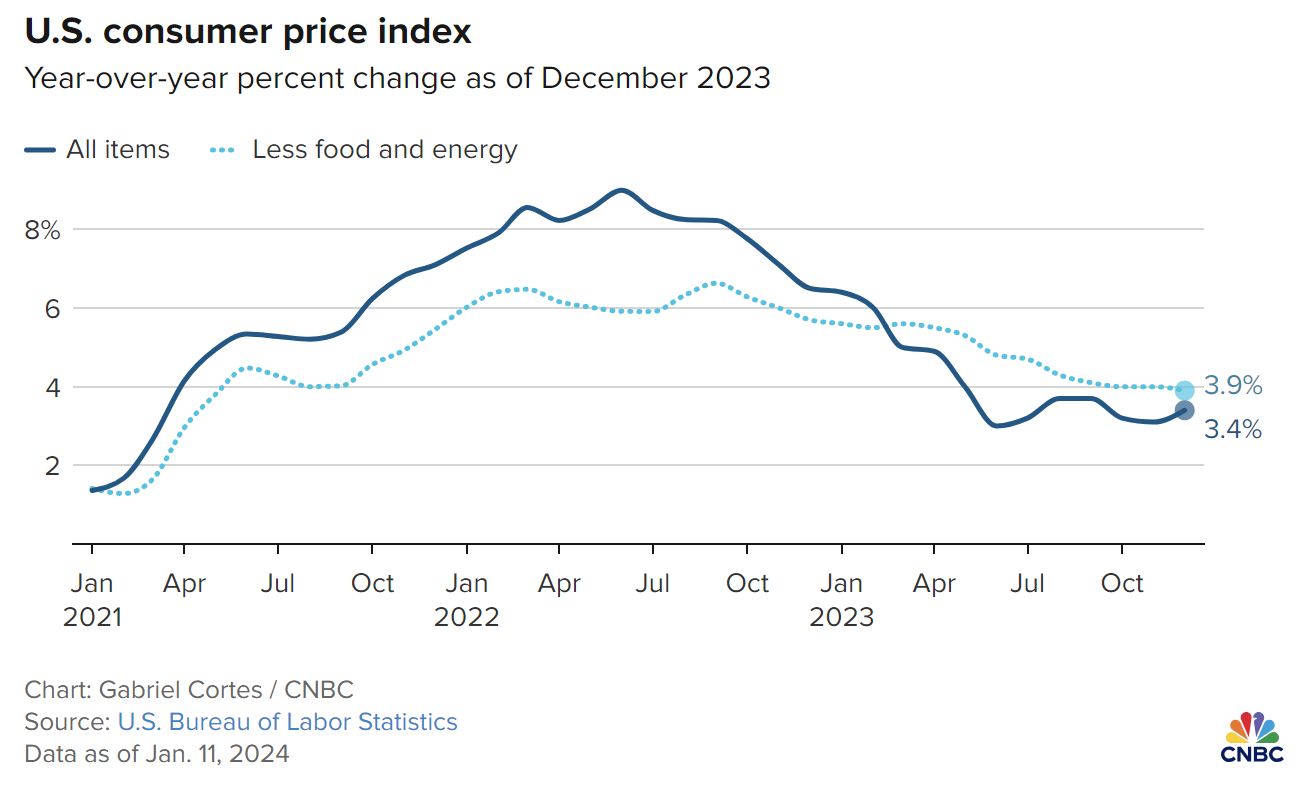

The past year’s steady gains on the inflation front were marginally reversed in yesterday’s CPI report for December, with housing costs pushing headline prices up last month to 3.4 percent on an annualized basis, up from 3.1 percent in November. Meanwhile, the SEC did an about-face on Wednesday, giving the green light to Bitcoin trading on securities exchanges for the first time.

For details on these and other economic policy developments of the week and what lies ahead, see below.

Happy MLK long weekend, all…

Best,

Dana

Headline

HFC Pushes for FY24 Top-Line Renegotiation; Johnson Walks Back Opposition to Short-Term CR

Speaker of the House Mike Johnson (R-LA) met with members of the House Freedom Caucus (HFC) yesterday following retaliation from 12 House Republicans who torpedoed a rules vote on Wednesday in protest of the top-line spending agreement announced on Sunday. Members of the HFC called on Speaker Johnson to renegotiate the top-line agreement made with Majority Leader Chuck Schumer (D-NY) – a move that would surely have consequences, dilatory or worse, for FY24 budget negotiations.

Johnson has apparently decided to stay the course, stating today that the top-line agreement is “strong.” Members of the HFC, led by Chairman Bob Good (R-VA), will continue to push the Speaker to renege on the deal, while Democrats and moderate Republicans look to move forward in the appropriations process. Ongoing opposition from the HFC to the top-line deal could make the passage of FY24 appropriations bills impossible without Democratic votes.

Regardless of Johnson’s next move, it is all but certain a Continuing Resolution (CR) will be needed to avoid a partial government shutdown come January 19. Both Democratic and Republican Senate leadership insist that passage of the four appropriations bills under the first CR deadline will be impossible by the end of next week. Speaker Johnson has walked back his opposition to a short-term CR, acknowledging that a CR is a price worth paying to prevent a partial shutdown. Majority Leader Schumer filed a cloture motion Thursday for a shell bill to allow a procedural vote on the CR early next week. Schumer is currently working on the terms of a short-term CR, which could push back one or both of the January 19 and February 2 funding deadlines until March with a simple date change, with a final passage vote later next week that would force a House vote on his bill.

New Details of the Bipartisan Tax Package Revealed

Details of the long-awaited bipartisan tax package are beginning to come to light. Senator Ron Wyden (D-OR) and Representative Jason Smith (R-MO), chairs of the Senate and House tax-writing committees respectively, have been negotiating a tax package that would address three Trump-era business tax provisions and expand the Child Tax Credit (CTC).

The initial ~$100 billion proposed package provided parity between the three business tax provisions and the Child Tax Credit at ~$49 billion each. Reporting from Punchbowl News on Wednesday revealed the modified package is more likely to total ~$70 billion with parity at ~$35 billion. The new proposal includes the same three business provisions and CTC priorities at a smaller scale than the ~$100 billion deal on a pro-rata basis. The business tax provisions would reinstate the 100% bonus depreciation deduction as well as delay the R&D amortization requirement and interest expensing limits. The Center on Budget and Policy Priorities (CBPP) reported the package will be offset by ending new claims for the Employee Retention Credit, but it is currently unclear how large the offset will be.

According to a thread on X, formerly Twitter, shared by Politico tax reporter Ben Guggenheim, the package to expand the CTC could include:

- an increase of the refundability cap to $1,800 in 2023; $1,900 in 2024; and $2,000 in 2025 to index for inflation;

- phase-in benefits on a per-child basis;

- allow families to use a prior year’s income to calculate their benefits in 2024 and 2025.

Sharon Parrott, President of CBPP, acknowledged these developments as “an important step forward,” citing the proposal could lift 400,000 children above the poverty line and reach children who have previously been excluded from the CTC. Even with new developments in the negotiations, hurdles lie ahead for the scaled-back proposal. Senate Democrats want to see a low-income housing tax credit included in the deal. Republicans in the House and Senate are worried the deal would give President Biden a much-needed legislative win in an election year. And even if a bipartisan deal can be secured, the package still needs a legislative vehicle. As the appropriations process continues to evolve and a short-term CR looks increasingly likely, the fate of the package still remains unclear. However, early indications are that the short-term CR is likely to be clean given its fragility.

Other Developments

Headline CPI Up, Core Continued to Cool in December

In a mixed CPI report, the core measure of inflation continued to cool last month in a positive sign for the Federal Reserve before it decides the fate of interest rates at the end of this month. Yesterday morning’s Consumer Price Index (CPI) data showed that core CPI, which excludes food and energy prices, rose by 3.9 percent over the last 12 months, reflecting the lowest annualized increase in core CPI since May 2021.

Headline CPI, however, rose by 3.4 percent on a year-on-year basis, up from 3.1 percent the prior month but significantly down from its June 2022 peak of 9.0 percent. Core CPI rose by 0.3 percent last month, on par with monthly increases of 0.2 to 0.3 percent over each of the six prior months.

Source: CNBC

The energy index rose by 0.4 percent last month as electricity and gasoline prices rose, offsetting a decrease in the natural gas index. Meanwhile, food prices rose by 0.2 percent over the month.

Price increases in December were mainly driven by an increase in shelter costs, which contributed to over half of the monthly all-items increase. Indexes for motor vehicle insurance and medical care also increased last month.

Today’s data reinforces that inflation overall is moving toward the Fed’s target of two percent. This month’s marginal price changes are expected to incline the Federal Open Market Committee (FOMC) to hold the interest rate steady at the 5.25 to 5.5 percent range for a third consecutive time when it meets next on January 30 and 31.

Senate Sustains Biden’s Veto of CFPB Data Rule

On Wednesday, the Senate voted to reject an attempt to overrule President Biden’s veto of a resolution to nullify the Consumer Financial Protection Bureau’s (CFPB) Small Business Lending Rule. The failed vote stymied the latest step in Republicans’ effort to block CFPB’s Dodd-Frank rule to require business data collection and help prevent discrimination in small business loans.

The CFPB’s Small Business Lending Rule, which was issued last March and became effective in August, would implement Section 1071 of the Dodd-Frank Wall Street Reform and Consumer Protection Act by requiring lenders to report data annually on credit applications to help the Bureau better understand the financing needs of small businesses owned by women and minorities and identify possible discrimination in an effort to facilitate the enforcement of fair lending laws.

Following the release of the rule by the CFPB, Republicans introduced and advanced S.J.Res.32, a joint resolution led by Senator John Kennedy (R-LA) to nullify the rule. After the resolution passed the Senate in October and House in December in largely party-line votes, President Biden vetoed the resolution in December. On Wednesday, the Senate voted 54-45 in a vote requiring a two-thirds majority to sustain President Biden’s veto with five Democrats and Independents – Senators John Hickenlooper (D-CO), Kyrsten Sinema (I-AZ), Joe Manchin (D-WV), Jon Tester (D-MT), and Angus King (I-ME) – voting with Republicans, with all Senators voting as they had when the resolution came to the Senate floor in October.

The data required under the CFPB’s Small Business Lending Rule will provide an important tool in revealing discriminatory lending practices. We look forward to reviewing the first CFPB data report for lenders in October.

Divided SEC Okays Bitcoin Spot ETFs

A day after the SEC’s X (formerly Twitter) account was hacked late Tuesday, with hackers posting an unauthorized announcement that the agency had approved the trading of Bitcoin, the SEC, in a 3-2 vote, approved the applications of 11 asset managers to buy and sell the digital asset. Although at least a half dozen bitcoin-futures ETFs (exchange-traded funds) exist, the SEC had previously rejected the trading applications on the grounds that the underlying assets are subject to fraud and market manipulation, a notion reinforced by the hacking.

SEC Chairman Gary Gensler said that a D.C. Circuit Court ruling last August in favor of asset manager Grayscale’s application compelled the change in position. The Commission’s Republican-nominated members joined with Gensler in the vote. In dissent, Commissioner Caroline Crenshaw called the decision “unsound and ahistorical,” warning it could “sacrifice investor protection” and facilitate non-economic “bogus” and “wash” trading, distorting price and volume and causing volatility in a highly concentrated market.

Groups advocating such protection also worried that integrating and mainstreaming digital asset trading into conventional capital markets offers a platform for products that have facilitated money laundering by groups engaged in illegal trafficking. Mark Hays, policy analyst with Americans for Financial Reform Education Fund, said that approval of Bitcoin ETFs exposes a much larger group of investors to risks seen in last year’s bank crisis. “Following repeated collapses and evidence of massive fraud, the crypto industry is desperate for the imprimatur of legitimacy that an established financial instrument provides.”

Hearings

HFSC GOP Attacks FSOC Designation Guidance

On Wednesday, the House Committee on Financial Services Subcommittee on Digital Assets, Financial Technology and Inclusion held a hearing to examine the impact of the Financial Stability Oversight Council’s (FSOC) revised guidance for non-bank financial company designations.

In November, FSOC issued its final guidance revising the process and analytical framework it uses to determine whether to designate a nonbank financial company as a systemically important financial institution (SIFI) — a nonbank financial company whose material financial distress could pose a threat to U.S. financial stability. SIFI designation leads institutions to face enhanced government oversight, including compliance with heightened capital, liquidity, and risk-management standards

As Ranking Member Stephen Lynch (D-MA) noted, FSOC has only designated four non-bank financial entities as SIFIs and, with those four now delisted, no institutions currently hold that designation. The Ranking Member importantly reminded the Subcommittee that the release of the new guidance follows attempts during the Trump administration to undermine FSOC’s designation authority. Subcommittee Republicans, including Subcommittee Chair French Hill (R-AR), took the opportunity to label FSOC’s approach to revised designations as part of a “mistaken approach.”

As FSOC officials have stated, the activities-based approach used in previous assessments will continue. The new guidance provides clarity on FSOC’s designation process.

HFSC Capital Markets Panel Reviews DOL Fiduciary Rule

The House Committee on Financial Services Subcommittee on Capital Markets convened on Wednesday for a hearing to examine the impact of the Department of Labor’s (DOL) proposed fiduciary rule, particularly implications for retirement savings and access.

In October, the DOL proposed the “Retirement Security Rule: Definition of an Investment Advice Fiduciary” which would establish a new regulatory definition for investment advice fiduciaries for purposes of Title 1 and Title II of the Employee Retirement Income Security Act (ERISA). The rule would ensure strong protections for retirement investors who seek professional investment advice and close existing regulatory loopholes to ensure that investment professionals provide advice in retirement savers’ best interest. The proposal was the latest move in an effort that has been ongoing since President Obama proposed a major overhaul of related rules in 2015 as mandated by the Dodd-Frank Act

As witness Kamila Elliott, Collective Wealth Partners CEO, stated, the proposed rule is consistent with the purpose and meaning of ERISA, which was enacted to protect assets held in tax-preferred retirement savings vehicles from market abuses. Further, despite the claims of those who object to the proposal, the proposed rule will not reduce access to retirement investment advice.

The comment period closed on January 2. 20/20 Vision strongly supports the finalization of a strong fiduciary rule.

Look Ahead

Wednesday, January 17

- Senate Budget Committee hearing: The Great Tax Escape: Closing Corporate Loopholes that Reward Offshoring Jobs and Profits

- Joint Economic Committee hearing: Rebuilding the American Dream: Policy Approaches to Increasing the Supply of Affordable Housing

Thursday, January 18

- House Committee on Financial Services Subcommittee on Oversight and Investigations hearing: Oversight of the SEC’s Proposed Climate Disclosure Rule: A Future of Legal Hurdles

Friday, January 19

- University of Michigan Consumer Sentiment Report