Update 666 — Jan. Jobs Gain of 517K

Good News but a Quandary for the Fed

Today’s blow out jobs report indicated US employers added 517,000 jobs in January – many more than forecasters had estimated and a spike not seen since July of 2022. The report brought mixed reactions. In a speech this morning, Biden touted strong employment numbers as an indicator of a robust economy. Meanwhile, capital market futures plummeted this morning as investors were spooked by the shadows of continued rate hikes with high interest rates likely to out last the six more weeks of winter. If only the Fed had projections with the predictive powers of Punxsutawney Phil for inflation.

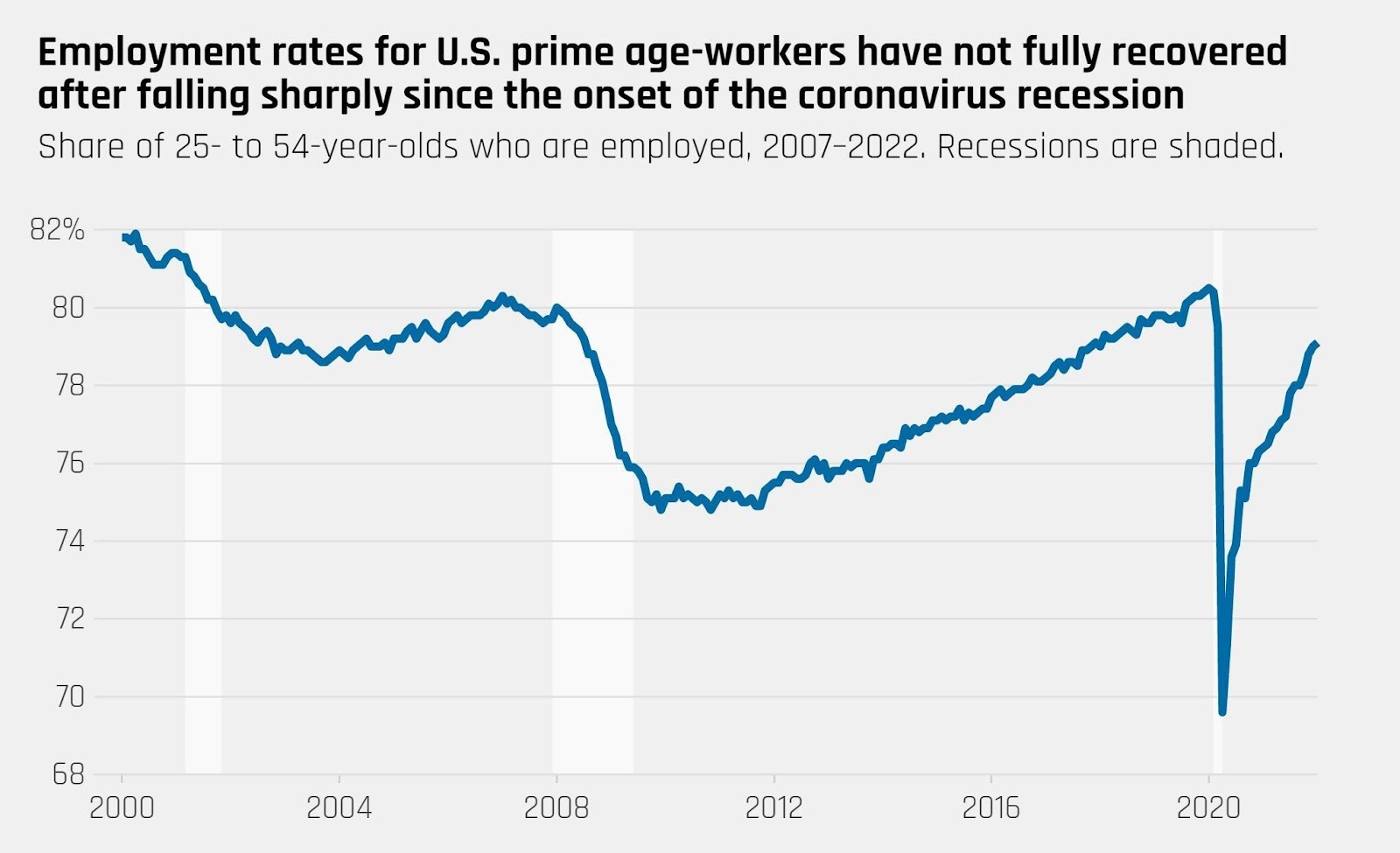

While January has brought higher numbers than average in recent years, the unemployment rate sits at 3.4 percent – a 54 year low not seen since 1969 – so there is still reason to believe the Fed can achieve a soft landing. No talk of recession after “a jobs report I will take any day of the week,” per Labor Secretary Walsh. Below, we analyze what the jobs numbers and Fed action could mean for the macroeconomy.

Good weekends all (and dress warmly),

Dana

_____

On Wednesday the Federal Reserve raised the Target Federal Funds Rate for the eighth consecutive time, continuing its most dramatic series of rate hikes since the early 1980s. The 25 basis point hike takes the range to 4.5 to 4.75 percent, but as its smallest recent hike, may signal a slow down in the central bank’s trend of rate increases as the Fed cautiously eyes slowing inflation. The labor market meanwhile has remained strong, but with wage growth beginning to level off, signaling a wide lane for a soft landing, reaching the target rate without triggering an economic recession.

Not Your Ordinary Jobs Report

On Friday, the Labor Department released its first jobs report of 2023. The unemployment rate ticked down to 3.4 percent in January, the lowest it’s been since 1969. Nonfarm payroll employment rose by a whopping 517,000 jobs in January, far exceeding economists’ expectations of 190,000. Gains were concentrated primarily in the areas of leisure and hospitality, professional and business services, and health care. The BLS also revised up its estimates, showing that job growth at the tail end of 2022 was stronger than previously thought.

Bureau of Labor Statistics, Graphic compiled by the Washington Center for Equitable Growth

Average hourly earnings rose 0.3 percent for the month and average hourly earnings increased 4.4 percent over the last 12 months. While the number of jobs added has remained elevated, the level of wage growth we have seen over the last few months has been moderate. Although the Fed remains cautious of a wage-price spiral, moderate wage growth, especially in the context of productivity increases, sets off no such alarms.

Powell has repeatedly said that the Fed needs to see a softening of labor market conditions in order to pare back its plans to raise rates. The jobs numbers for January, while surprising, are not per se concerning. One month of unusually high jobs growth shouldn’t affect the Fed’s plans too much, particularly given January’s moderate wage growth. The Fed will be careful not to crush labor demand too forcefully in order to bring down inflation.

Prices Across the Board Heading Down

Headline personal consumption expenditures (PCE) – the inflation measure primarily used by the Federal Reserve in determining its policy choices – increased .1 percent for the month of December and five percent over the year. Core PCE – which excludes food and energy and is generally considered a better indicator of inflation trends – rose 4.4 percent year-over-year in December, the smallest annual increase since October 2021. Month-over-over month, core PCE rose 0.3 percent, in line with expectations. Consumer spending fell .02 percent for the month, while personal income rose 0.2 percent.

Inflation also continues to shift from goods to services as supply chains ease and demand bounces back from pandemic lows. Prices for goods decreased by 0.7 percent, driven largely by falling energy prices, while prices for services increased by 0.5 percent. Increases in food prices continued to slow– the food for off-premises consumption index increased just 0.2 percent over the month, down from 0.3 percent in November. Increases to the housing index have remained high, but are expected to start coming down within the next few months. Housing has been driving increases in the services index, but falling rent prices for new leases indicate that we should start seeing housing inflation fall soon.

The Fed can take December’s PCE data as another positive sign that the economy is on the right track. With inflation decelerating and only a modest decrease in consumer spending at the tail end of the year, the economy appears to be on the path the Fed is targeting. The Fed will continue to hike rates in the hopes of seeing deceleration in core services ex-housing, which has shown less improvement than goods and housing in recent months.

“Ongoing Increases”

After Wednesday’s 25 basis point rate hike, market watchers continue to speculate as to whether the Fed will continue to increase rates, pause or even reverse course throughout 2023. The Federal Reserve said, “ongoing increases… will be appropriate” despite hopes by some market watchers that the central bank would instead reference “additional increases.” The Fed’s latest move signals its shift from a strategy of rapid increases to a period of monitoring the effects of hikes to date.

Investors’ hopes of a smaller rate hike were realized and markets reacted strongly to the Fed’s announcement. Following the rate increase, the Dow Jones Industrial Average rose 30 points, the S&P 500 rose 33 points to a two-month high, and the Nasdaq Composite rose 177 points. At the same time, the price of Treasury yields fell sharply during Chairman Powell’s press conference.

The market expects at least two more 25 basis point rate increases in the coming months before the agency pauses. The rate could reach as high as the 5 to 5.25 percent range this year, as the Fed may prefer to raise rates as a precaution, rather than pause prematurely and risk inflation becoming entrenched.

Trading of 30-day Fed funds futures suggests that investors anticipate another 25 basis point rate hike in March but have low confidence in a rate hike holding at the 5 to 5.25 percent range through the rest of the year. Some investors have placed confidence in a reversal of the Fed’s recent trend of rate hikes. Investors, optimistic that inflation is coming down from its peak and seeing wages growth slowing, hope that the Fed will reassess its strategy in coming FOMC meetings.

All Hands on Deck

Democratic lawmakers are still concerned about the recent rate hikes and the possibility that the Fed might tip the economy into a recession. Even capital markets – who were cautiously optimistic after Powell’s comments at Wednesday’s meeting – reversed course this morning after a surprisingly strong jobs report suggested that the Fed may continue its aggressive stance well into this year. However, the Fed must be cautious not to overcorrect. Growth in average hourly earnings has slowed and is not running at inflationary levels. Unless we start seeing more surprises in the coming months, Powell and the FOMC should be able to chalk January’s shocking total up to a one-off.

There are still other circumstances that could derail a soft landing, even if the Fed can thread the needle on rate increases. As Republicans in Congress continue to threaten the full faith and credit of the United States, Powell has made it clear that the Fed does not hold the key to solving the default crisis. It’s up to the White House and Congressional leaders to agree on a solution before the U.S. defaults and sends the economy into a tailspin. As expected, Biden and Speaker McCarthy’s meeting this Wednesday failed to end with an agreement. Efforts towards a resolution will surely accelerate as we near the X-date.