Update 758 — Capital One/Discover:

Major Test of US Bank Merger Policy

Last week, Capital One, the nation’s ninth-biggest bank, announced an agreement to purchase Discover Financial, the fifth-largest credit card issuer and fourth-largest payment network in the country. The merger would create a financial institution with $620 billion in consolidated assets and the sixth-largest bank in the U.S., one many consider yet another Too Big to Fail bank. Opposition to the deal arose almost instantly from banking consumer advocates, joined this and last week by leading members of Congress on a bipartisan basis concerned about anti-competitive consolidation in the industry.

The proposed merger comes as the Biden administration pushes for an update to U.S. bank merger policy. While the administration’s whole-of-government approach to promoting competition seemed to advance this week with the FTC suing to block the Kroger-Albertson merger, the Capital One-Discover merger poses a new challenge. What are the issues in play and the implications for industry competition, consumers, and financial stability? What is the merger approval process going forward and probable outcomes? See below.

Best,

Dana

The proposed Capital One-Discover merger presents a new threat to the U.S. financial system and American consumers. 20/20 Vision joins the growing chorus of advocates raising questions about the merger, urging regulators like the Federal Reserve and Office of the Comptroller of the Currency (OCC), and the Department of Justice (DOJ) to exercise their power to scrutinize and, if necessary, block the billion-dollar deal.

The Proposed Capital One-Discover Merger

Last Monday, Capital One Financial Corporation announced that it and Discover Financial Services had entered into an agreement under which Capital One would acquire Discover in an all-stock transaction valued at $35.3 billion. Under the deal, Discover shareholders would receive 1.0192 Capital One shares for each Discover share. If the deal closes, Capital One shareholders would own approximately 60 percent and Discover shareholders would own approximately 40 percent of the combined company.

The combined company would be the nation’s sixth-largest bank, largest credit card issuer, and fourth-largest payment network. According to their announcement, the companies expect the deal to close as soon as this year or in early 2025 pending regulatory and shareholder approvals.

Another Too Big to Fail Bank?

The deal would create yet another too-big-to-fail bank. As of December 31, 2023, Capital One was the ninth largest bank in the United States, with $476 billion in total assets and Discover was the twenty-seventh largest, with $149 billion. The merger would make the combined company the nation’s sixth-largest bank, with over $600 billion in assets.

As MRV Associates Principal Mayra Rodriguez Valladares has discussed, the combined company would have significant concentration risk, meaning that a lot of its assets would be sensitive to the same economic and market factors. Credit card loans represent 47 percent of Capital One’s loan portfolio and 79 percent of Discover’s loan portfolio. Although both banks seem well-capitalized, they have both experienced rising delinquency rates and charge-offs in their respective credit card portfolios.

Additionally, Valladares notes that while Capital One is subject to annual stress tests, Discover is only required to conduct an enterprise-wide stress test every two years; its last stress test was conducted in 2022. It is unclear how Discover or the combined company would fare under periods of stress.

Vertical Integration in Credit Card Industry

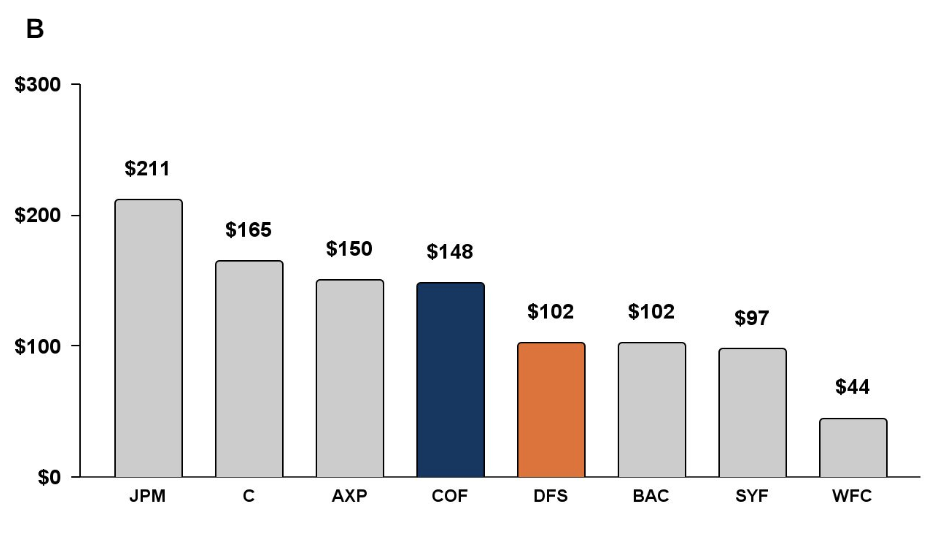

The merger would make the combined company the largest credit card issuer in the country, with over $200 billion in outstanding credit card loans. According to the companies’ investor presentation last week, Capital One was the fourth-largest credit card issuer in America in 2023, with $148 billion in credit card loans while Discover was the fifth-largest alongside Bank of America, with $102 billion. The combined company would surpass JP Morgan which was the largest credit card issuer in America in 2023.

Credit Card Loans Issued by U.S. Institutions in 2023

Source: Capital One Discover Investor Presentation, February 20, 2024.

The merger could lead to increased credit card prices for consumers. As the Consumer Financial Protection Bureau (CFPB) report noted last week, large banks offer worse credit card terms and interest rates than small banks. The report found that the 25 largest credit card issuers charged customers interest rates 8 to 10 points higher than small- and medium-sized banks and credit unions, translating to $400-500 more in annual interest costs for the average cardholder. The report also found that large issuers were more likely to charge annual fees than smaller issuers.

Credit Card Industry Market Structure

The merger also raises significant antitrust questions. The four major payment networks in the United States are Visa, Mastercard, American Express, and Discover, with Visa and Mastercard dominating the payments market with a combined network volume of over $9 trillion. This is compared to American Express’s total network volume of $1.35 trillion and Discover’s $550 billion. The combined company would shift Capital One’s debit and selected credit portfolios from networks run by Visa and Mastercard to the Discover network, giving Capital One access to a network of over 300 million cardholders.

The benefit of such vertical integration is not lost on Capital One CEO Richard Fairbank who said, the day after the merger announcement: “We have always had a belief that the holy grail is to be able to be an issuer with one’s own network.” The companies estimate that by 2027, the combined company would take in $1.2 billion from merchants and consumers due to this shift. The combined company would be able to bring in at least a portion of that substantial figure because, as Matt Stoller has noted, the combined company would be exempt from Fed rules implementing the Durbin amendment, which regulates debit card payment networks. This exemption blocks the Fed from imposing a price cap on debit card swipe fees charged by the combined company, as it can with Visa and Mastercard.

Growing Opposition to a Dangerous Deal

Given that the proposed merger would further consolidate the banking sector, a bank larger than the combined size of three banks that failed last year, and could lead to higher credit card prices for consumers, the deal has faced growing opposition in Congress. Last week, Ranking Member of the House Financial Services Committee Maxine Waters (D-CA) called on bank regulators and the DOJ to block the deal expeditiously.

On Sunday, Senator Elizabeth Warren (D-MA) and 12 members of the House wrote to Federal Reserve Vice Chair of Supervision Michael Barr and OCC Acting Comptroller Michael Hsu calling on their agencies to block the Capital One-Discover proposed merger in order to protect financial stability and consumers. Senator Josh Hawley (R-MO) has also written to DOJ Assistant Attorney General for the Antitrust Division Jonathan Kanter urging the DOJ to block the merger.

Capital One reportedly pushed for an industry lawsuit against the Fed, FDIC, and OCC seeking to undermine Community Reinvestment Act rules. Seven trade groups, including the American Bankers Association and the U.S. Chamber of Commerce, filed such a lawsuit just last month. If Capital One has in fact sought to shirk its responsibility to the consumers and communities it profits off of just before it seeks to increase its own market power, this could undermine its argument that the deal is beneficial to the broader public. This point could encourage even more pushback.

Regulatory Fight Remains Ahead

As the regulators of Capital One and Discover, the Fed and the OCC are required by federal law to review and approve the merger in order for it to proceed. The DOJ can also comment on the proposed merger and litigate to block the deal if it sees fit.

The Biden administration has made clear that competition is a priority. In 2021, President Biden issued an Executive Order on Promoting Competition in the American Economy, encouraging banking regulators and the DOJ to adopt a plan for the revitalization of merger oversight. Just last month the OCC issued a notice of proposed rulemaking to make a common-sense reform to its bank merger approval process by removing the automatic approval of bank mergers following the comment period. Regulators and the DOJ must give the proposed deal the scrutiny it deserves.

The proposed Capital One-Discover merger underscores the need for bank regulators and relevant agencies to finalize a long overdue update of banking merger guidelines to effectively evaluate a bank merger’s impact on financial stability. Today Ranking Member Waters led 15 House Democrats in a letter urging the Fed, FDIC, OCC, and DOJ to finalize robust bank merger guidelines “before all we are left with is an oligopoly of megabanks to serve our constituents.” We continue to call on the Fed, FDIC, OCC, and DOJ to finalize these guidelines to preempt the next dangerous megabank merger.