Update 704 — Implementing Bidenomics

The Economic Return on Industrial Policy

The manifold federal infrastructure investments of the last two years are finally starting to see macroeconomic returns. On Monday, President Biden kicked off the second phase of the Administration’s “Investing in America Tour.” The tour — which consists of 60 stops in 30 states over three weeks – gives Biden a chance to tout the impressive early economic returns in the midst of a presidential campaign. Just hours ago, he gave a speech in Chicago reinforcing his plan for boosting the national economy – a term dubbed “Bidenomics.”

Biden, who kicked off part two of his tour by announcing a $40 billion investment in high-speed internet infrastructure, is expected to showcase the implementation of his legislative accolades, including the CHIPS and Science Act, and explain how his various infrastructure investments have benefited families across the nation. Can the gains yield political returns? We discuss below.

Best,

Dana

The Biden administration compensated for years of neglect of the nation’s infrastructure. The vast economic measures enacted over the past couple of years – incentives worth hundreds of billions for clean energy, semiconductor manufacturing and infrastructure — amount to the most sweeping initiative to kickstart American industry in decades.

The main elements of the administration’s industrial policy are contained in three major industrial revitalizations:

- The Bipartisan Infrastructure Law (IIJA) enacted in 2021

- The Inflation Reduction Act (IRA) enacted in 2022

- The CHIPS and Science act enacted in 2022

How have they fared in their objectives, as far as can be discerned at this early juncture?

Surge In Manufacturing Construction

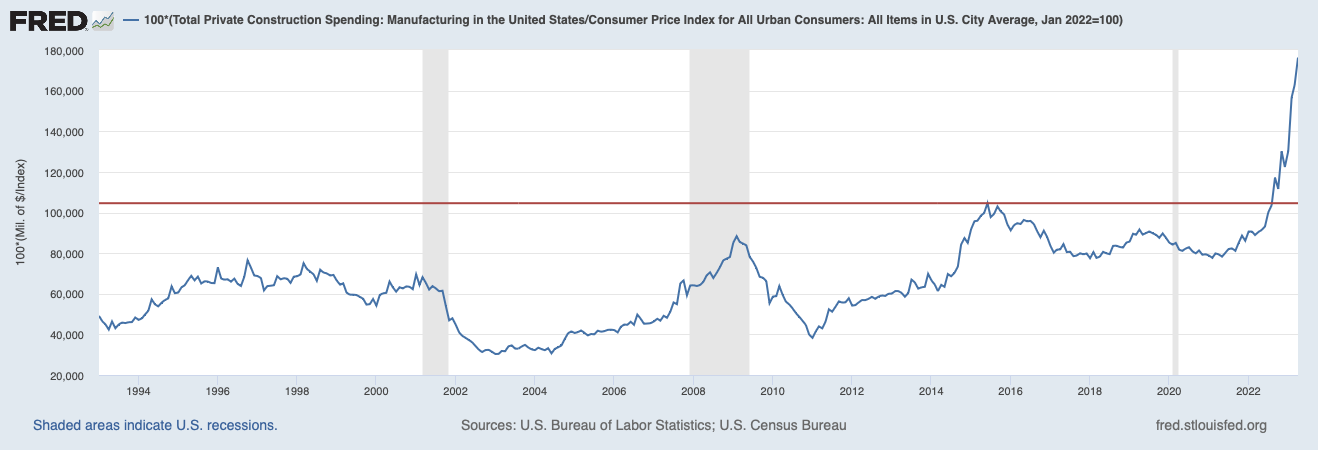

At the beginning of this month, the Census Bureau released data showing a historic surge in construction spending for manufacturing in April of this year. Private spending on the construction of manufacturing facilities peaked in June of 2015, a level not surpassed until September 2022. Since then, private companies have kept spending, and by April of this year, spending had increased by almost 70 percent.

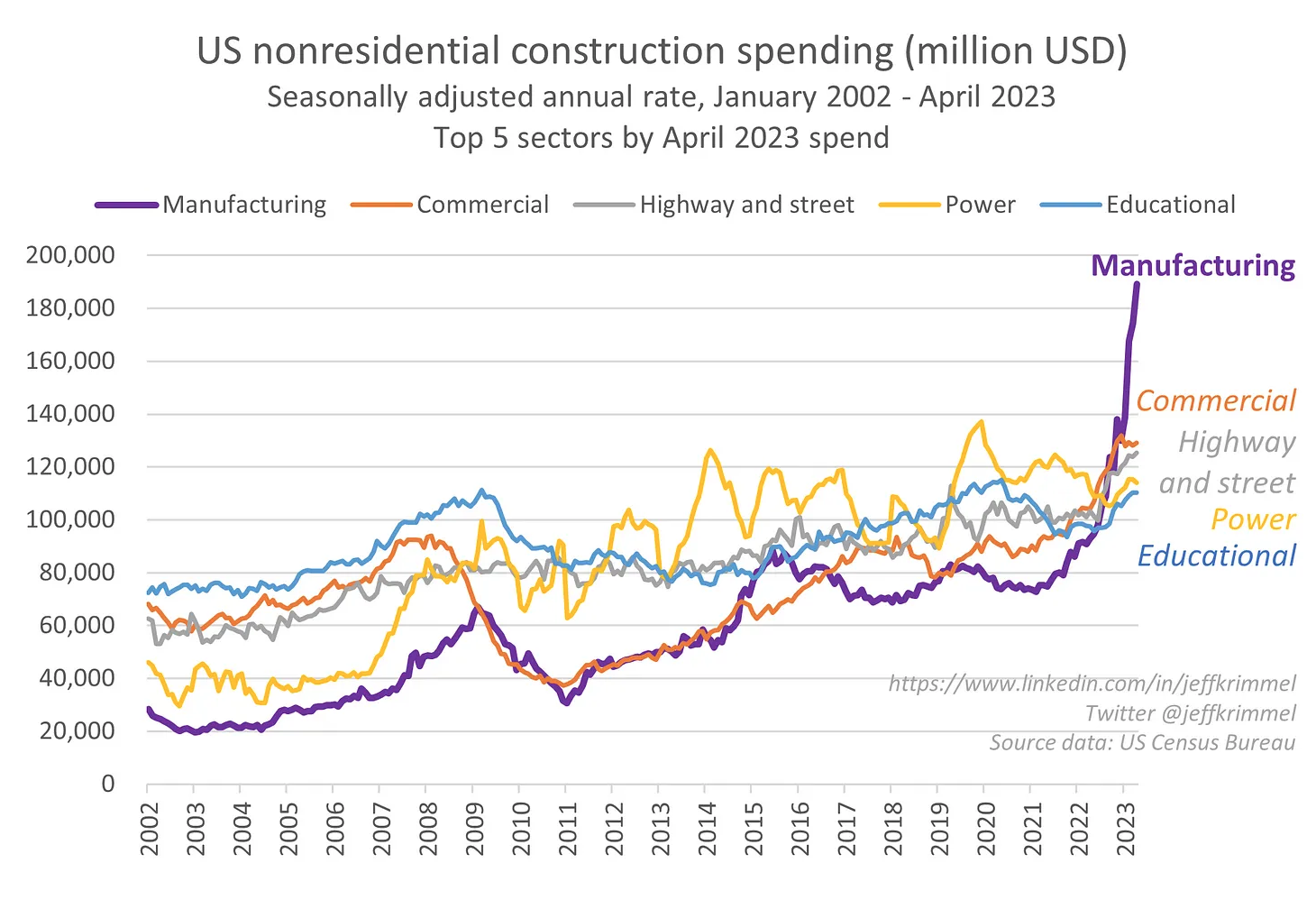

The current unprecedented surge in manufacturing construction spending is truly unprecedented. And while all categories of construction spending have seen rapid growth over the last two years, the graph from Jeff Krimmel below illustrates the extent of the surge, compared to trends in spending in each construction category broken out by the Census Bureau. From April 2022 to April 2023, manufacturing construction spending more than doubled, a result in part of the President’s commitment to revitalizing the industrial base, and Biden is making it a core of his case for reelection. Here is a look at the legislative and policy actions that have led to this point, and reviewing their implications as an economic and political strategy.

Legislative Roots

Starting with the IIJA, more than 35,000 projects have been funded. Most of this funding went to projects to upgrade transportation and water infrastructure, which, combined with the IIJA’s $65 billion to expand high speed internet, vastly expanded the universe of potential locations for industrial production. In addition, the $7.5 billion to build EV chargers represented a direct increase in demand for American manufactured goods in a market that had a total asset value of just $2.4 billion at the time of the law’s passage.

The IRA included billions of dollars in tax incentives for advanced manufacturing energy projects and American-built electric cars, as well as a bonus tax credit for using domestically manufactured materials. The CHIPS and Science Act provided even more direct manufacturing investment from the federal government: $39 billion in direct manufacturing incentives, the largest part of its $52.7 billion price tag.

All told, these three bills provided more than $100 billion in federal manufacturing incentives over ten years, but it is important to note that direct federal support has been a fraction of a percent of recent spending. Since Biden’s inauguration, public manufacturing construction spending peaked at less than 0.8 percent of total manufacturing construction in the middle of 2022 and has fallen dramatically at its current surge.

Private Sector Following Government Leadership

Following decades of suboptimal private sector industrial investment, there has been a surge following this legislation. The best explanation for this phenomenon is the private sector following the government’s lead. Seeing legislative and executive commitments to restoring the American Industrial base, private companies have opened the floodgates to investing in manufacturing in America.

As Sen. Chris Murphy (D-CT) has noted, this pattern follows the Hawthorne effect, a psychological tendency to work harder when attention is being paid to the work being done. By continually enacting generational industrial policies after decades of being unable to muster the political will to do so, the administration has provided this attention.

The private sector’s response to the government’s enactment of policies aimed at bolstering American manufacturing has been nothing short of transformative. Firms, armed with a newfound awareness of government support and the enticing array of benefits, have been invigorated to invest in manufacturing like never before. The Hawthorne effect, known for its ability to influence behavior and performance, has come into play as companies strive to enhance productivity and spur innovation. Capitalizing on recognition and support from the government, businesses are pouring resources into cutting-edge manufacturing technologies, intensive research and development initiatives, and comprehensive worker training programs. This surge in productivity and innovation not only enhances their individual prospects but also bolsters the overall competitiveness of the manufacturing sector.

Furthermore, the Hawthorne effect has yielded a shared mindset among industrial firms. Recognizing the common objectives of expanding manufacturing, companies are forging partnerships and actively participating in industry-wide initiatives. By pooling knowledge, resources, and best practices, they have ignited a virtuous cycle of heightened efficiency and innovation within the sector. Importantly, this collaborative approach extends beyond fleeting gains. Firms maintain their momentum even as the government’s initial focus shifts elsewhere. The manufacturing landscape has undergone a remarkable metamorphosis, poised for sustained growth and global competitiveness, all catalyzed by the government’s initial policies and the pervasive influence of the Hawthorne effect.

Private companies have announced $491 billion in manufacturing commitments that will cover the country: $219 billion in semiconductors and electronics, $149 billion in EVs and batteries, $88 billion in clean energy, $20 billion in biomanufacturing, and $14 billion in heavy industry. These projects are spread around the country.

Translation to Job Growth

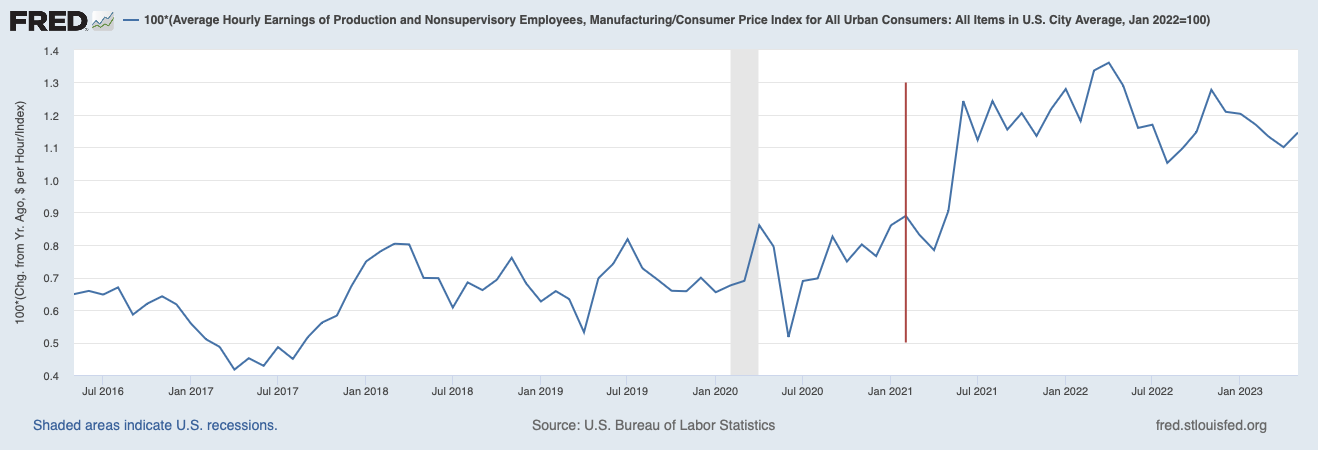

Best of all, this explosion of investment has directly led to more and better paying jobs. Since April of 2021, almost 11 million manufacturing jobs have been created, an average of more than 420,000 per month for the last 25 months.

Inflation-adjusted wages for workers in these jobs have been increasing, especially for production and nonsupervisory workers. The graph below shows the change in wages, measured in January 2022 constant dollars per hour earned by these workers. As can be seen, Biden’s inauguration (the red vertical line) preceded a change in the trend of wage increases for these workers.

All of this activity fits with the administration’s focus on growing wages for lower-income Americans, who have been hit hard by the deindustrialization of the past half-century. And rather than trying to reinvent the heavy industry of the 20th century, the new investment appears to be going toward the advanced industries where it will be possible to maintain a competitive advantage.

Building manufacturing facilities and paying workers more are good, but to judge the success of Bidenomics by these two phenomena would be naive. For Bidenomics to succeed, these facilities have to be able to innovate beyond needing what amounts to infant industry protection to be able to compete globally. The increase in domestic production capacity needs to provide consistent disinflationary pressure, and wages need to continue to outpace inflation for these workers. All in all, the data presented here are promising, but insufficient to prove the central thesis of Bidenomics.

The trajectory is favorable, if the progress slow, for the political calendar. In the real economy, lags are long due to the time it takes to build factories and hire workers. The trend is encouraging, but as we have learned over the last few years, extrapolating from a trend can be dangerous. The byword is rapid implementation, the means by which the economic gains of building the plant become the political gains of hiring.