Update 520 — Macro Reconciliation Act:

Survey of Labor and Capital Markets 1Q21

Despite strong numbers coming out of the March jobs report, the economy still has 8.4 million fewer employed Americans than it did a year ago. With a new set of infrastructure proposals from the Biden administration on the table, the questions arise: how long will it take to close this jobs gap, a key metric of the recovery, with and without this new plan?

Today, we look at the macroeconomy’s performance over the first quarter of 2021, examining labor and financial markets — two key markets that operate on different principles and time horizons. In the labor market, a picture of the real economy for workers and consumers now emerges while in the financial markets, the investor’s take on the future is reflected.

Best,

Dana

—————–

Last Friday, the Bureau of Labor Statistics released its monthly jobs data showing an increase of 916,000 new jobs in March. This figure widely exceeded expectations and represented the fastest job growth since August. The leisure and hospitality sectors saw the strongest gains, a welcome sign for an industry that has struggled this past year. With the Biden administration preparing to move forward with a multi-trillion dollar infrastructure package, the improving state of the economy will likely be a factor in upcoming congressional negotiations.

Labor Market Record, Issues Ahead

In March, the Federal Reserve projected a slightly rosier labor market picture than forecasted last December. Since the passage of Biden’s American Rescue Plan (ARP), the Fed predicts that the unemployment rate will drop to 4.5 percent by the end of 2021 down from its prior five percent estimate. The unemployment rate now sits at just six percent, but nearly five million people have dropped out of the labor force since the beginning of the pandemic.

Not all areas of the labor force are recovering equally. Even as sectors such as professional services and retail approach near full labor market recovery, the leisure and hospitality sector has barely retained 80 percent of the workforce it had prior to the pandemic, despite adding 280,000 jobs in March. And state and local government job growth has not only stagnated but remains far below even its pre-Great Recession levels. This uneven recovery underlines the need for Biden’s Build Back Better infrastructure package designed to make long-term investments in the American workforce.

Financial Markets: Records, not Rebounds

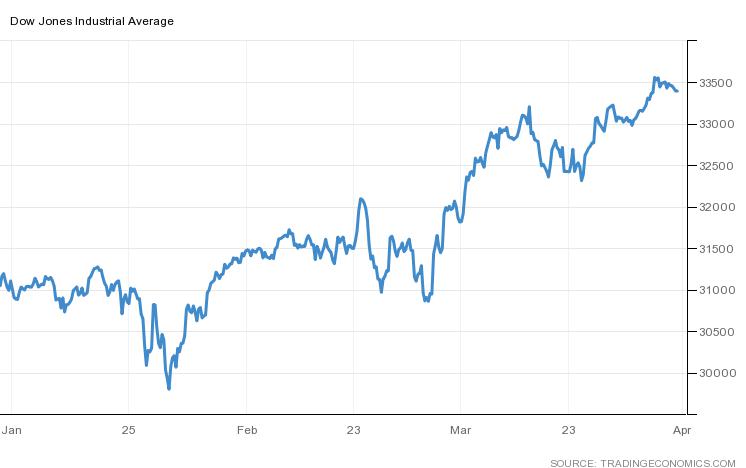

Financial markets have exceeded even bullish expectations so far in 2021, despite a rocky start. The S&P 500 and Dow indices increased in Q1 by 7.8 percent and 5.8 percent, respectively. The NASDAQ saw a more modest gain of 2.8 percent. This market growth has been driven by an effective vaccine rollout, continued accommodative monetary policy by the Fed, and unprecedented fiscal stimulus both in December 2020 ($900 billion) and March 2021 ($1.9 trillion).

Markets were able to overcome a period of volatility in January due to the GameStop short squeeze — a massive spike in the price of the video game company due to trading by internet investors. This quarter was also marked by an increase in the pace of sale of Special Purpose Acquisition Companies (SPACs), which has led to concerns about these companies’ high fees, historically poor performance, and mismatched incentives.

Dow Jones Industrial Average, 2021

Source: TradingEconomics.com

With the Fed showing no signs of raising interest rates, consumer spending on the rise, and another major federal spending package on the horizon, financial markets could continue to push higher in the coming months. Now, there are even fears that the economy may be accelerating too quickly. Biden’s Build Back Better infrastructure plan would add another $2.25 trillion to the economy, raising eyebrows among inflation hawks. Federal Reserve Chairman Jerome Powell, testifying before the House and Senate last month, expressed only limited concern about recent volatility in capital markets and lauded the banking system’s performance over the past 12 months.

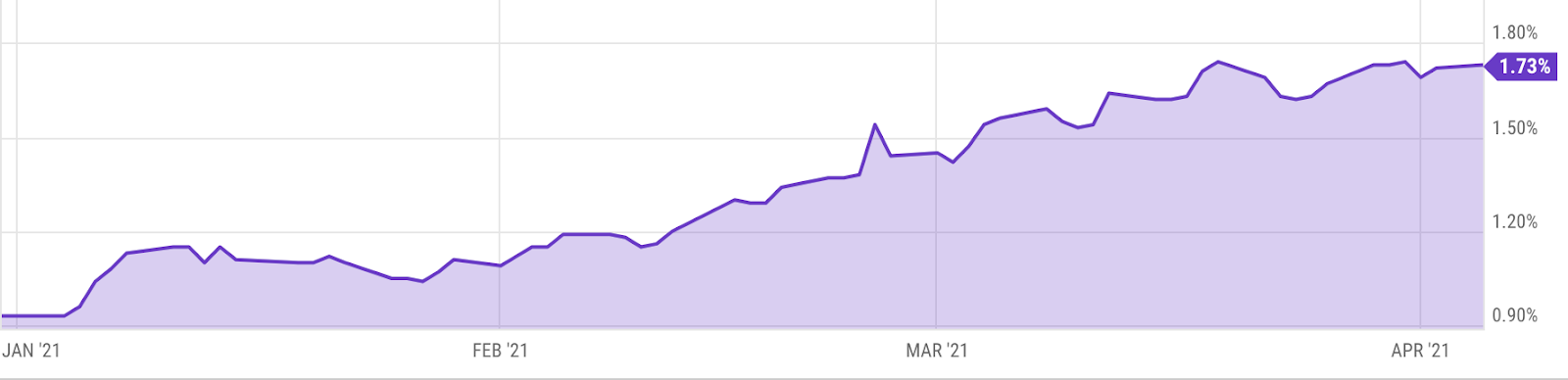

One area of slight concern is the bond market. While the Fed, in its mid-March FOMC projection, stressed that rate hikes are unlikely before 2024, bond investors are skeptical. Bond yields have risen sharply since the beginning of this year, particularly the 10 Year Treasury, which saw a significant jump during Q1. This trend indicates that investors are betting either that the Fed will raise interest rates at a sooner date or that inflation in 2021 will be more pronounced than the Fed has projected. Still, yields remain historically low, and evidence of severe inflation is uncertain for now.

10 Year Treasury Rate, 2021

Source: YCharts

Economic Outlook Ahead

The economic outlook for the remainder of 2021 looks promising. Most economists expect that as the country reaches herd immunity and the threat of the pandemic abates, the economy will enjoy a strong period of growth. A forecast by the International Monetary Fund released yesterday projected six percent growth for the world economy in 2021, an increase from its earlier projection of 5.5 percent in January. The IMF projected that US GDP is expected to grow by 6.4 percent.

Likewise, the Federal Reserve recently forecasted a 6.5 percent increase in real GDP this year, a significant increase from its December projection of 4.2 percent growth. Powell attributed this better-than-expected outlook to growing vaccine access and “unprecedented” fiscal and monetary policy from Congress and the Fed. Q2 is expected to be especially big, with economists predicting growth higher than 9 percent.

Undoubtedly, this growth will be fueled by an increase in consumer spending, as pent-up demand from the past year is finally unleashed. The Conference Board Consumer Confidence Index increased by 19.3 points in March, a significant improvement leading to the index’s highest reading since the beginning of the pandemic. With many Americans receiving upwards of $2,000 in stimulus payments in recent months, retail spending is expected to surge, and increased vaccinations have already led to a spike in travel. Whether this increase in spending will continue for the remainder of the year will depend in large part on the success of vaccinations and to what extent the virus continues to spread.

At the same time, consumer prices have been increasing and are expected to continue to do so. In its March forecasts, the Fed projected 2.4 percent inflation in 2021, an increase from its December forecast of 1.8 percent. However, Powell has repeatedly downplayed the risk of higher inflation and has indicated that the Fed has no plans to raise interest rates this year.

Infrastructure and the Biden Economy

Many are cautiously optimistic that robust growth can be maintained going forward. But a strong economy in the coming months may complicate President Biden’s push for an infrastructure package in Congress. Detractors have already begun to argue that additional federal spending will not be needed as the economy improves. Others point to risks of withdrawing or tapering support, citing rued historical experience.

But if the economy improves this year as expected, Biden will have greater credibility when making the case for more government spending. And the purpose and time horizon of the infrastructure package are different from that of the ARP. Build Back Better aims to reduce inequality and ensure long-term economic growth. These ends are still very much worth pursuing even as the economy recovers from the recession.

EverlyNVDaly City

In fact no matter if someone doesn’t know then its up to other visitors

that they will help, so here it happens. 0mniartist asmr

It’s not my first time to pay a quick visit

this website, i am browsing this web page dailly and get fastidious

information from here every day. asmr 0mniartist

Hey very nice blog! asmr 0mniartist

Having read this I believed it was rather informative.

I appreciate you taking the time and energy to put this content

together. I once again find myself spending a significant amount of time both reading and leaving comments.

But so what, it was still worth it! asmr 0mniartist

VictoriaNMTacoma

Good day! This is my first comment here so I just wanted to give a quick shout out and say I truly enjoy

reading through your posts. Can you recommend any other blogs/websites/forums that cover the same subjects?

Thank you so much! 0mniartist asmr

Een bepaalde type onder de planten is erg bijzonder, en daar hebben wij het over:

de Fortuneipalm. Meer specifiek, het is een soort palm.

De Trachycarpus fortunei is de uiterst aangetroffen palmensoort die de Nederlandse kou

kan doorleven.

Take a look at my web-site; Phoenix Roebelenii

BraydenMTOrlando

Hmm it looks like your site ate my first comment (it was

extremely long) so I guess I’ll just sum it up what I

submitted and say, I’m thoroughly enjoying your blog.

I too am an aspiring blog writer but I’m still new to everything.

Do you have any points for rookie blog writers? I’d certainly appreciate it.

asmr 0mniartist

Besproei de palmboom elke week met vocht, tijdens de lente/herfst en de avonden van de zomers.Besproei de palm elke week met water, in de lente/herfst en de avondjes van de zomers.

Feel free to surf to my web page … Winterharde Agave

Right here is the perfect webpage for anyone who wishes

to find out about this topic. You realize so much its almost hard

to argue with you (not that I actually would want

to…HaHa). You certainly put a fresh spin on a subject which has been written about for many years.

Wonderful stuff, just great! 0mniartist asmr

mature adult phone chat

free online dating sites

I¦ve recently started a site, the info you provide on this web site has helped me greatly. Thanks for all of your time & work.

best free dating site for serious relationships

free dating site

best free dating site for serious relationships

single women dating

Als de gevoelstemperatuur voorbij -18C arriveert, dan wordt het mogelijk dat de ernstige kou plus stormwind de palmboom schaadt.

De Trachycarpus fortunei heeft nodig een prachtig zonnig plekje, want daar houdt hij van, sinds het een palm i

my website Palmboom Kopen

In de winterperiode gaat de Wagnerianus palm in een slaap, en dan hoeft

hij bijna niet water meer te krijgen. Vervolgens kan het wel 3 dagen duren voordat de fortunei weer water nodig heeft.

Look into my web blog :: https://www.Pokemongo.nl/

If you wish for to increase your knowledge just keep visiting this website and be updated with the most

up-to-date news update posted here.

I couldn’t refrain from commenting. Exceptionally well written!

I know this web site presents quality depending articles or reviews and additional stuff, is there any

other website which gives these information in quality?

I’m not that much of a online reader to be

honest but your blogs really nice, keep it up!

I’ll go ahead and bookmark your website to come back later.

All the best

how to use tinder , tinder online

tinder date

tinder date , tider

tinder login

When I originally commented I clicked the “Notify me when new comments are added” checkbox and now

each time a comment is added I get several emails with the

same comment. Is there any way you can remove me from that

service? Thanks!

Hi there! I could have sworn I’ve been to your blog before but after looking

at some of the articles I realized it’s new to me.

Anyhow, I’m definitely pleased I stumbled upon it and I’ll be bookmarking it and checking back regularly!

I needed to thank you for this fantastic read!! I absolutely enjoyed every

bit of it. I’ve got you saved as a favorite to check out new things you post…

Elke week is het een voorkeur om uw palm met water te

besproeien, en dat bovenal tijdens de herfst of lente,

plus in de avonden van de zomers.

My page :: winkel voor palmbomen

Wonderful items from you, man. I’ve be mindful your stuff prior to and you are just extremely great.

I actually like what you have obtained here, certainly like what you are saying and the way by which you

say it. You are making it entertaining and you still

care for to keep it smart. I can not wait to learn much more from you.

This is really a wonderful site.

Whoa! This blog looks exactly like my old one!

It’s on a entirely different topic but it has pretty much the same layout and design.

Great choice of colors!

cialis 5mg

kamagra chewable 100 mg canada

tinder sign up , tinder dating app

how to use tinder

browse tinder for free , tinder sign up

tinder date

I couldn’t resist commenting

tinder date , tinder dating app

http://tinderentrar.com/

tider , tinder date

http://tinderentrar.com/

scoliosis

I do not know whether it’s just me or if everyone else experiencing issues with your

website. It looks like some of the text within your content are running off the screen. Can someone else please comment and let me know if this is happening to them too?

This may be a issue with my internet browser because I’ve had this happen previously.

Thanks scoliosis

You are my aspiration, I possess few blogs and often run out from brand :). “Never mistake motion for action.” by Ernest Hemingway.

scoliosis

Very quickly this website will be famous among all blogging people, due to it’s pleasant content scoliosis

scoliosis

Hello there! I simply wish to offer you a big thumbs up for your great info you’ve got here on this post.

I am returning to your web site for more soon. scoliosis

dating sites

The other day, while I was at work, my cousin stole my iphone and tested to see if it can survive a 40 foot drop, just so she can be a youtube

sensation. My apple ipad is now broken and she has 83

views. I know this is entirely off topic but I had to share it with someone!

dating sites https://785days.tumblr.com/

free dating sites

Hey There. I discovered your weblog the use of msn.

That is an extremely neatly written article. I will be sure to bookmark it and return to read extra of your helpful information.

Thank you for the post. I will certainly comeback.

dating sites

I’m really inspired with your writing talents and also with

the format for your blog. Is this a paid subject or did you customize it

yourself? Anyway keep up the excellent quality writing,

it’s rare to look a nice weblog like this one nowadays..

Tijdens de winter hoeft de palmboom haast geen water te

hebben, dan verkeert hij in een soort van winter slaap.

Eenmaal in de drie dagen is dan aan te raden vocht te verstrekken.

Also visit my web blog :: yucca Rostrata

In de winter hoeft de palm bijna geen water te ontvangen, dan is hij

in een soort van winter slaap. 1 maal in de drie dagen is dan aan te raden vocht te verstrekken.

Here is my web page :: Teeninga palmen

Just want to say your article is as amazing. The clearness

in your post is simply nice and i could assume you’re an expert on this subject.

Well with your permission allow me to grab your feed to

keep updated with forthcoming post. Thanks a million and please continue the gratifying work.

Normally I don’t learn post on blogs, but I wish to

say that this write-up very forced me to check out and do it!

Your writing taste has been amazed me. Thank you,

quite nice article.

I must thank you for the efforts you’ve put in penning this blog.

I’m hoping to check out the same high-grade content from you

later on as well. In fact, your creative writing abilities has motivated

me to get my own, personal site now 😉

fantastic publish, very informative. I ponder why the opposite specialists of this sector don’t notice

this. You should continue your writing. I’m sure, you’ve a huge readers’ base already!

Its like you read my mind! You appear to know a lot about this, like you wrote the book in it or something.

I think that you can do with a few pics to drive the message

home a little bit, but other than that, this is wonderful blog.

A fantastic read. I’ll certainly be back.

I blog quite often and I seriously thank you for your content.

Your article has really peaked my interest. I’m going to bookmark your website and keep checking for new information about once

a week. I opted in for your RSS feed too.

I know this website offers quality dependent articles or reviews

and other information, is there any other site which gives these kinds of information in quality?

Een zonnig plekje is de beste positie voor een Trachycarpus fortunei, aangezien hij daarvan houdt

als palmboom. Echter raden wij wel aan in de winter om hem te afschutten tegen wind.

Review my webpage palmbomen te koop

Er zijn ook periodes dat de fortuneipalm haast niet vocht hoeft te

ontvangen, want dan slaapt hij vrijwel, tijdens de winter.

Een keer per 3 dagen is dan toereikend.

Here is my site :: op deze site

Pretty nice post. I just stumbled upon your blog and wanted to say that

I’ve truly enjoyed surfing around your blog posts. After all

I’ll be subscribing to your feed and I hope you write again soon!

Onder de palmensoorten, vindt u de Trachycarpus fortunei.

Beter nog, het is de uiterst populaire palmboom dat in ons landje wordt tegengekomen. Dit heeft te maken met de winterhardheid, waarvan de Fortunei de aller winterhardste is.

Have a look at my web-site … winkel Voor palmbomen

De Fortunei is een palmbomen soort. Sterker gezegd,

het is de meest populaire palm welke in ons kikkerlandje wordt aangetroffen. Dit is aangezien de Trachycarpus fortunei het allermeest vorst bestendig is.

Check out my blog; science-marketplace.org

cheap cialis

Indien de gevoelstemperatuur voorbij -18C komt, dan is het

mogelijk dat de hevige vorst plus stormwind de palmboom beschadigt.

Visit my web page … palmbomen kopen

Een zonnig plekje is de beste locatie voor een Trachycarpus wagnerianus, aangezien hij daarvan houdt als palm.

Doch raden wij wel aan in de winters om hem te afschermen tegen wind.

Also visit my webpage http://Flightseasy.Net

Tijdens de herfst en lente en de avonden van de zomers is het aanbevolen om de palm met vocht te besproeien. Dat verwijdert stofdeeltjes van de bladeren waardoor zij

beter licht kunnen oppakken en evenzo mooier worden. Alsmede voorkomt het ongediert

Here is my web-site; Yucca rostrata

Indien de gevoelstemperatuur voorbij -16C komt, dan wordt

het mogelijk dat de hevige kou en stormwind de palm beschadigt.

De Trachycarpus fortunei houdt heel erg van zon, het is namelijk

een palm, dus geef hem een mooi opgewekt plekj

my web page: http://Www.Interleads.Net

discount non prescription generic lasix

kamagra

purchasing cialis online

buy prednisone no rx from canada

Mocht je een trachycarpus aanschaffen, verpot hem vervolgens Mocht je zo’n fortunei aankopen, verpot hem vervolgens onmiddelijk..

Feel free to surf to my web blog :: Howard

Daglicht is heel erg gewild bij palmen in het algemeen, wat dus alsmede

geldt voor de Wagnerianus. Zorg voor een bekoorlijk plekje buiten de tocht, waar hij veel zonlicht kan ontvangen.

Have a look at my webpage: Palmboom

Er zijn ook periodes dat de fortunei haast geen vocht hoeft te ontvangen, want dan slaapt hij feitelijk, tijdens

de winters. Een keer per 3 dagen is dan voldoende.

Feel free to visit my web page Tropische Planten

Het is mogelijk de palmboom te havenen wegens kou door extreme vorst en stormwind, dat de gevoelstemperatuur voorbij -17C komt.

De Trachycarpus fortunei houdt heel erg van zon, het is namelijk een palmboom,

daarom geef hem een mooi opgewekt plekj

My web page – yucca Rostrata

De fortuneipalm moet in de zomers veel water ontvangen, dat zal hij verwelkomen. Tijdens de hitte neemt hij

veel vocht op uit de grond, dus maak de kluit kletsnat.

my blog post; winterharde Palmboom

Een bepaalde species onder de planten is volkomen speciaal, en daar hebben we het over:

de Fortunei palm. Deze soort plant is een palmboom, een tropische soort dus.

Feel free to surf to my web page teeningapalmen

De fortuneipalm mag in de zomer veel water ontvangen, dat zal hij graag ontvangen. Met de warmte

neemt hij overvloedig vocht op uit de bodem, dus maak de kluit kletsnat.

Check out my web site; Lesley

Im obliged for the blog.Really looking forward to read more. Will read on…

Besproei de palmboom wekelijks met water, tijdens

de herfst of lente en de avonden van de zomers.Besproei de palmboom elke week met vocht, tijdens de lente/herfst plus de avondjes van de zomers.

My blog – agave

Verpot gelijk een fortunei indien je deze aanschaft.

In de verkoopwinkel doen ze een zo klein mogelijke bloempot om

de kluit zonder de groei in de weg te zitten zodat hij verplaatsbaar is.

Nadat je hem verpot groeit hij weer verde

my web site – oneshot.lk

De Trachycarpus fortunei houdt van veel licht, dus plaats hem op een zonnige locatie.

Tijdens de winters wordt aanbevolen de waaierpalm keurig afgeschermd te worden tegen wind, omdat het

weleens wel buitengewoon koud kan worden.

Also visit my website Winterharde Agave

In de winters hoeft de palm haast geen water te hebben, dan is hij in een soort

van winter slaap. 1 maal in de drie dagen is dan aan te raden vocht

te geven.

Also visit my web page – Teeninga Palmen

Een bepaalde soort tussen de planten is heel speciaal, en daar hebben wij het

over: de Fortuneipalm. Meer specifiek, het is een echte palm.

Also visit my web site: Forum.roboindia.com

pratiyogita darpan year book 2019 ebook Un Homme A Part 1080p Gratuitement rukmini prakashan science book pdf

I have learn some excellent stuff here. Certainly worth bookmarking for revisiting.

I surprise how so much attempt you set to create the sort of magnificent

informative website.

Casino Supermarche 321 Avenue Berthelot 69008 Lyon Fr Geant Casino Auxerre Lundi De Paques Casonic Jackpots

Shop Casino Nozay Slots Telephone Marque Belle France Chez Casino

cialis on sale in usa

You are my breathing in, I own few web logs and rarely run out from to post .

Wow that was odd. I just wrote an incredibly long comment but after

I clicked submit my comment didn’t appear.

Grrrr… well I’m not writing all that over again. Anyways,

just wanted to say great blog!

I like this web blog very much, Its a very nice spot to read and obtain information. “The absence of war is not peace.” by Harry S Truman.

viagra for women uk viagra usa pharmacy ViagraCND100Mg – cod viagra online

I do not even understand how I stopped up here, but I thought this

post used to be good. I don’t understand who you are however certainly you’re going to a famous blogger should you are

not already. Cheers!

generic viagra medication for sale otc viagra walmart ViagraCND100Mg – discount viagra usa

I do consider all of the ideas you’ve offered in your

post. They’re very convincing and can definitely work. Nonetheless, the posts are very brief for beginners.

May you please lengthen them a bit from subsequent time?

Thank you for the post.

I am curious to find out what blog system you are using?

I’m experiencing some small security issues with my

latest site and I’d like to find something more secure.

Do you have any recommendations?

good

good