Update 531 — Infrastructure Pay-Fors:

Financing Options and Considerations

Congress has been grappling this week with the question of how to fund President Biden’s two-part $4.5 trillion infrastructure plan. The conversation in hearings on the Hill has largely focused on paying for the package with new or higher taxes, which runs counter to the goal of promoting a rapid and robust recovery.

The less-discussed alternative — deficit financing — is cheaper, fiscally more responsible, more economically stimulative, and politically less risky for tax-sensitive Democrats. Below, we examine the benefits of a mixed approach to funding/financing Biden’s proposals.

Best,

Dana

—————–

This week, the Senate Finance Committee and House Ways and Means Committee held hearings on how to best finance federal infrastructure investments. During these hearings, members brought up a variety of revenue suggestions including higher corporate tax rates, increased user fees, and reviving Build America Bonds. These hearings are emblematic of a larger debate within the Democratic caucus over the scale and duration of pay-fors in Biden’s Build Back Better agenda.

Finding the Right Mix

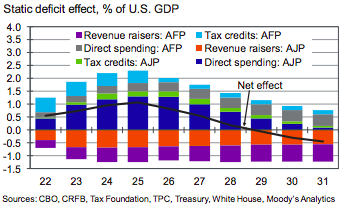

President Biden has proposed increasing federal spending by $4.5 trillion (1.8 percent of GDP) over the next decade. While most of the proposed physical infrastructure and tax credit investments phase out after eight and four years respectively, the investments in education and the care economy would be permanent. This package is financed primarily through taxes on multinational corporations and top-earning individuals, generating $2.8 trillion in direct taxes over ten years.

Budget Impact of Build Back Better

A large chunk of the plan will be deficit-financed in the short term — a fact that is neither negative or a reason to scale back the package. With ten-year Treasury bonds trading at 1.65 percent, the cost of waiting longer to fix our crumbling infrastructure carries more potential fiscal risk than taking out additional loans. One way to leverage investments in physical capital through short-term deficit financing is by issuing project specific bonds.

Building America Bonds Better Than Taxing?

Senators on both sides of the aisle said at yesterday’s Senate Finance hearing that they are interested in reviving an Obama-era bond program to help finance infrastructure projects. Both Senate Finance Chair Wyden and ranking member Sen. Crapo expressed interest in renewing the Build America Bond (BAB) program, which was created by former President Obama’s 2009 stimulus law.

Other senators and the witnesses also advocated for restoration of tax-exempt advance refundings and an expansion of private activity bonds as lawmakers explored options for financing infrastructure.

While there is no exact formula for calculating the optimal taxes-to-deficit-financing ratio, infrastructure spending can partially offset its own costs through positive economic feedback effects. Moody’s Analytics estimates that if the AJP and AFP are fully implemented, they would create 3.5 million new jobs and expand GDP by nearly $900 billion by 2030. This accelerated growth in productivity and employment would increase federal revenue by around $400 billion over ten years

Timing Taxes

For decades, policymakers have used an arbitrary 10-year budget window to assess the fiscal impacts of tax and spending decisions. This narrow scorekeeping does not reflect the policy considerations of federal investments in physical capital and education, both of which have long-term economic benefits. Biden is proposing tax reform to cover “every penny” of federal spending over a longer 15-year period, and Federal Reserve Chair Powell said last month that it is ‘highly unlikely’ the Fed will raise interest rates this year despite a stronger economy. This is an optimal time for the federal government to fund spending through public borrowing and issuing Treasury bills.

The return on investment for infrastructure is significant — estimates of the fiscal “multiplier” for infrastructure are substantially higher than for other fiscal interventions. Per Moody’s, every federal dollar spent on transportation infrastructure yields an additional $1.29 in GDP. Marginal dollars spent on childcare and education more than pay for themselves, almost immediately. Tax cuts, especially favoring high-earners, simply do not offer the same bang for their buck —a one-dollar decrease in corporate tax collected, for example, would result in a $0.32 increase in GDP.

The timing may be right to right-size the tax code as well. Investors and economists — some in Biden’s ear and others attending Cabinet meetings — are worried the macroeconomy may be overheating. If they are right, increasing taxes on the wealthy would not only result in a more equitable tax code and long-term returns on investment, but it could serve as a means to temper unprecedented stock market growth and accompanying inflation. Higher taxes on capital movement need not be an economic drag, and the window of opportunity may be open for a much-needed investment paid for by those who best weathered last year’s economic storms.

The politics around taxation is rapidly changing and public support for tax equity as a fiscal tool has grown dramatically. Polling consistently shows that support for Biden’s infrastructure plan rises when people learn that higher taxes on corporations would fund it. These numbers are encouraging given that Democrats have not yet coalesced around a final plan.

The Equity Question

Congress has the opportunity to not only focus on when infrastructure should be paid for, but who should be paying for it. The tax code currently allows billionaires to pay a lower effective tax rate than ordinary working Americans.

- Capital Gains: While workers are subject to a top tax rate of 37 percent for their labor income, the investor class gets away with a 20 percent preferential tax rate. Taxing capital gains the same as labor income for high-income earners would only impact the wealthiest 0.3 percent of taxpayers, while not changing the tax for 99.7 percent of Americans.

- Multinational Corporate Tax: The largest 1,500 corporations in the United States pay an average tax of 7.8 percent. In a time of record corporate profits, these companies can afford to pay more. The cost of Biden’s corporate tax changes would fall primarily on the top one percent of earners, not working Americans.

Proposals Promising…

- Prescription Drug Reform: Last year, the House passed the Lower Drug Costs Now Act, which would have saved $456 billion over the next decade by allowing the government to simply negotiate down the price of prescription drugs. While the savings from this bill were intended to be used to cover the cost of expanding Medicare coverage, prescription drug negotiation is also a viable fiscal offset for federal infrastructure investments.

- IRS enforcement: Biden is proposing $80 billion dollar investment in the IRS as well increased reporting requirements from banks, which the White House projects will yield $700 billion over the next decade. Independent analysis finds that the revenue return on IRS enforcement ranges from a low of 6:1 to a high of 22:1. However, due to CBO scoring rules, revenue generated this way won’t be considered an on-budget offset.

… and Problematic

- Transportation user fees: While fuel taxes are currently the primary funding source for the Highway Trust Fund to the tune of $40 billion a year, this method is regressive because the cost of transportation is disproportionately higher for low-income families.

Opportunities for Macro Improvements

The AJP and the AFP are far-reaching plans that seek to fulfill a number of President Biden’s campaign promises. The success of these plans will bear on the success of Democrats in 2022 and 2024. That success can be achieved in a fiscally responsible and politically safe way. By shifting the focus away from solely relying on taxes, toward a mix that includes short-term deficit financing — an option that is less risky today — Democrats can maintain a focus on the critically macroeconomic goals and deliver on the promises of bold new investments in education, childcare, broadband, waterways, surface transportation, and more.

abraham lincoln chasseur de vampires english book Dvdrip Torrent mahanati savitri book pdf free download

Sideway Slot Car Casino SupermarchГ© Saint Priest En Jarez Horaires Horaire Ouverture Hyper Casino St Loup

Th Me Soiree Casino Le Petit Casino Rue Du Faubourg National Strasbourg Casino Enghien Decevant

This post will help the internet users for setting up new weblog or even a blog from start to

end.

I am always browsing online for posts that can help me. Thx!

walgreens generic viagra natural viagra foods ViagraCND100Mg – viagra in portland