Update 479: Fixing a Trumped-Up Code:

Biden’s Fiscally Fair, Re-Balanced Budget

Vice President Pence and Senator Kamala Harris face off tonight in the one and only Vice Presidential Debate of the cycle. We cover that critical encounter on Friday.

Today, as prospects for a next coronavirus package waffle via twitter, we examine the tax plans (or lack thereof) of the presidential candidates facing off in November. Trump intends to continue on his path of revenue destruction, proposing cuts that go even further than his 2017 ones. Biden, on the other hand, has put forth a well-thought-out plan to make the code more equitable and also more fruitful.

Best,

Dana

————————————————

With the recent news of President Trump’s meager tax payments in 2016 and 2017, the presidential race has had a renewed focus on the candidates’ tax plans. Trump’s signature accomplishment has been the 2017 tax bill (commonly referred to as the “Tax Cuts and Jobs Act,” or TCJA), which made the US tax code drastically more regressive. Trump’s plans for a second term are vague, but Vice President Biden has a thorough plan to ensure tax justice and fairness in the code. The top one percent of households would bear three-quarters of the burden of Biden’s tax increases.

Below, we examine Biden’s changes to the code, focusing on the TCJA, taxes on individuals and corporations, and tax expenditures.

TCJA Tax Cuts

In 2017, the Republican-controlled Congress passed the TCJA, a regressive tax bill that cut taxes substantially for businesses and individuals from 2018 through 2025. Biden has taken aim at these Trump tax cuts, proposing a plan that will restore tax rates for incomes over $400,000 to pre-TCJA levels. Biden’s plan will raise the top marginal tax rate from 37 percent back to 39.6 percent. But Biden has vowed not to raise taxes on those under the $400,000 threshold.

Trump’s tax cuts overwhelmingly favored the top one percent of earners, leaving the rest of Americans to foot the bill, as the richest five percent of taxpayers received 50 percent of the TCJA’s benefits or $145 billion in 2020. This payday for the wealthy will add up to $2 trillion to the federal debt. Biden’s plan will partially recover these losses by repealing some of the cuts for top earners, raising between $100 to $150 billion through 2026.

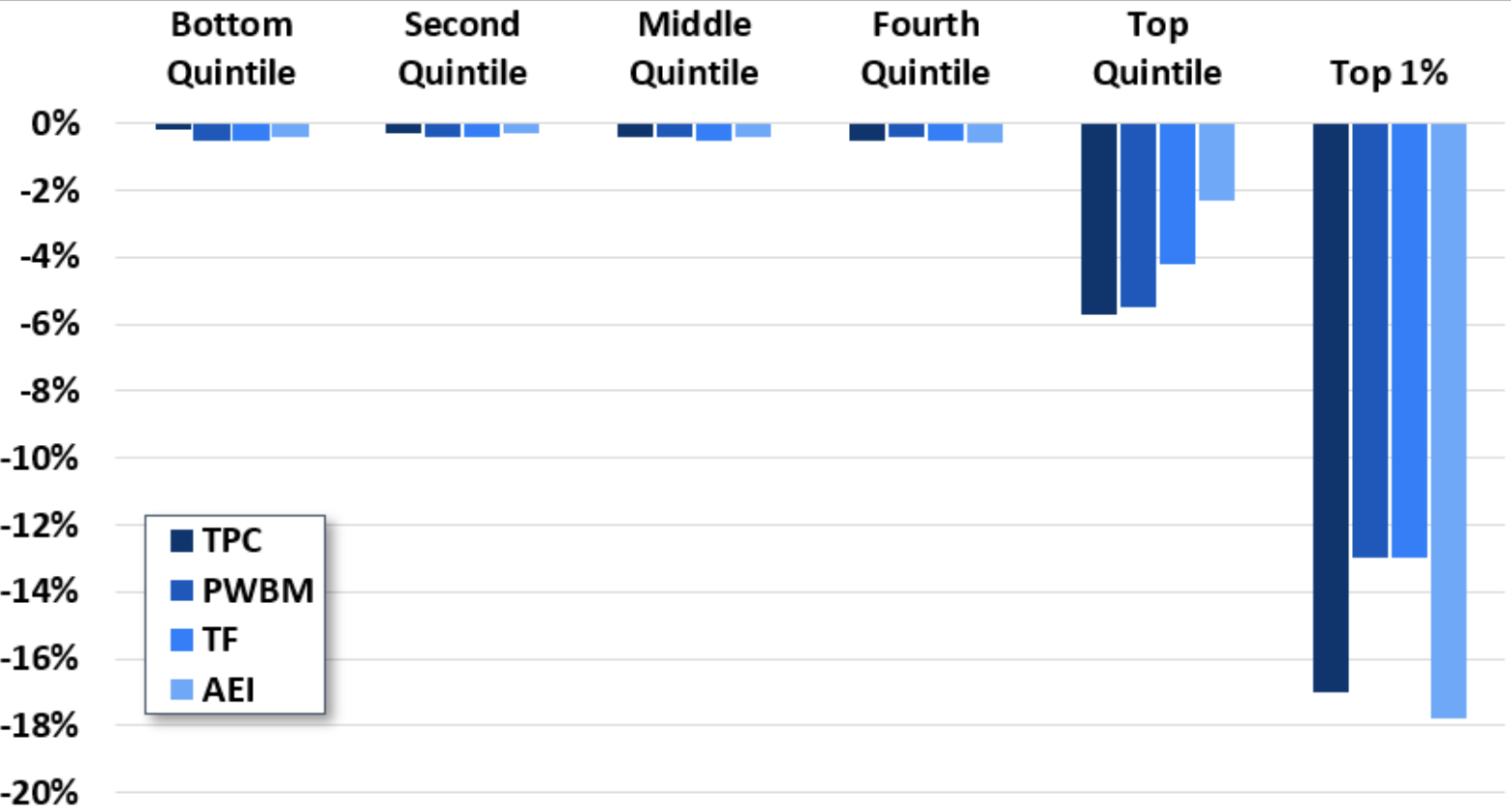

Distributional Effects of the Biden Tax Plan

Source: Committee for a Responsible Federal Budget’s analysis of TPC, PWBM, TF and AEI

The Biden proposal is highly progressive. The $400,000 threshold excludes all but 1.8 percent of American households, a group projected to earn almost 25 percent of adjusted gross income in 2021. His tax plan will increase the effective tax rate for this group by 13 to 18 percentage points, without any significant impact on the economy or other income groups’ tax rates.

Other Individual Tax Reforms

In addition to his partial repeal of the TCJA, Biden has proposed the following individual tax increases on the top one percent of earners, including:

- A “Doughnut Hole” in the Payroll Tax: The Biden tax plan includes a 12.4 percent Social Security payroll tax on wages above $400,000. This would create a “doughnut hole” where wages between $137,700 and $400,000 avoid Social Security tax. Over time, the current $137,700 cap would rise with inflation, closing the gap. The change would raise an estimated $800 billion to $1 trillion over 10 years, replenishing Social Security.

- Taxing Capital Gains as Ordinary Income: The top rate for long-term capital gains is currently 23.8 percent; Biden aims to raise this to 39.6 percent for individuals making above $1 million. The plan also proposes eliminating step-up basis for inherited assets. This loophole allows heirs to avoid capital gains taxes on the appreciation of inherited assets during the decedent’s lifetime. These proposals would bring a combined $379 to $502 billion in revenue over the next decade.

- Limiting Itemized Deductions: While only ten percent of taxpayers itemize their deductions, more than half of taxpayers in the top-income bracket claim this deduction. Biden proposes capping the overall value of itemized deductions at 28 percent. Under Biden’s plan, the Pease Limitation would reduce the amount one can deduct for every dollar over $400,000 by three cents. These provisions would raise between $260 to $380 billion over a decade.

Corporate Tax

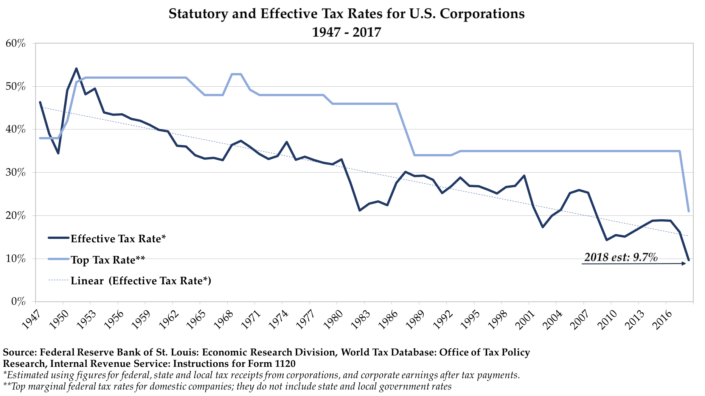

Trump’s tax cuts drastically lowered the corporate tax rate from 35 percent to 21 percent, substantially lower than the OECD average. Before the cuts, corporations had already decimated their effective tax rate through tax shelters and havens. Following a long period of decline, the effective corporate tax rate rose under President Obama to just under 20 percent before plummeting to 9.7 percent following the 2017 tax cuts.

Statutory and Effective Tax Rates for U.S. Corporations (1947 – 2017)

Biden proposes raising the federal corporate income tax rate to 28 percent, aligning it with the OECD average as a share of GDP, ensuring US competitiveness, and eliminating the Trump corporate tax giveaway. His plan would raise between $1.1 and $1.3 trillion over 10 years and would be highly progressive, as the incidence would fall primarily on the very wealthy — the primary owners of stock.

Yet a high corporate tax rate can’t prevent companies from eliminating their tax liability completely by utilizing loopholes and shifting profits offshore. To address this, Biden would reinstate a corporate alternative minimum tax at 15 percent of book income. The tax would apply to corporations with at least $100 million in annual income and would raise between $160 to $320 billion over 10 years.

Biden’s plans also mention other ways to close corporate tax giveaways like the Opportunity Zones program and prevent tax avoidance and evasion through the use of international tax havens.

Tax Expenditures

The Biden tax plan also makes the tax code more progressive by expanding tax credits that primarily benefit lower-income workers and families.

- Child Tax Credit (CTC): Biden would increase the CTC from a maximum of $2,000 per child under 16 to $3,000 for children ages 6 to 17 and $3,600 for children under the age of 6. The plan would also make the credit fully refundable and accessible in monthly installments rather than as a lump sum after filing a return. The Biden proposal would increase benefits by $2,260 on average for CTC-eligible families. Biden’s changes to CTC are to last only through the recession.

- Child and Dependent Care Tax Credit (CDCTC): Biden would expand the CDCTC for families earning up to $125,000 and make it refundable. The plan would provide funds for half of child care costs for children under the age of 13 up to $8,000 per child — a $5,000 increase from the current maximum allowed expenses.

- Housing tax credits: Biden would reinstate and expand the First Time Homebuyer’s Tax Credit, created in 2008 by the Housing and Economic Recovery Act but ended in 2010. Biden’s version of the credit would provide $15,000 for first-time homebuyers and would not expire. He would also create a new, refundable Renters’ Credit, which would provide funds to ensure renters do not pay more than 30 percent of their household income on rent.

- Earned Income Tax Credit (EITC): Biden’s plan broadens eligibility for the EITC to workers without dependent children over the age of 65. The expansion would greatly benefit low-income seniors, who are currently unable to access the credit and thus at a disadvantage compared to younger workers with the same income level.

The need for a simplified, more progressive tax code is clear, and Biden’s tax plan will do much to reverse the damage of the last four years. But Biden could go further. Policies like a wealth tax would guarantee that wealthy Americans with a low rate of earned income, like Trump, pay their fair share. Progressives should take the opportunity to promote structural tax proposals to ensure an equitable code for years to come.

https://hcialischeapc.com/ – buy cialis online

Hello There. I found your blog using msn. This is a very well written article. I will make sure to bookmark it and come back to read more of your useful information. Thanks for the post. I’ll definitely return.

At this time I am going away to do my breakfast, afterward having my breakfast coming

yet again to read more news. 0mniartist asmr

Somebody essentially lend a hand to make severely articles I’d state.

This is the very first time I frequented your web page and up to now?

I surprised with the research you made to make this actual submit extraordinary.

Wonderful job! 0mniartist asmr

Currently it appears like Drupal is the preferred blogging platform available right now. (from what I’ve read) Is that what you are using on your blog?

Very nice post. I just stumbled upon your blog and wished to say that I have truly enjoyed browsing your weblog posts. After all I will be subscribing for your feed and I am hoping you write again soon!

Hurrah! At last I got a website from where I be able to in fact get useful

information concerning my study and knowledge. asmr 0mniartist

Aw, this was a really good post. Taking the time and actual effort to make a top notch article… but

what can I say… I put things off a lot and never manage

to get anything done. 0mniartist asmr

Wow! In the end I got a web site from where I can really obtain valuable information regarding my study and knowledge.

0mniartist asmr

cash advances

best payday loan

Appreciate the recommendation. Let me try it

out.

With havin so much content and articles do you ever run into any

issues of plagorism or copyright infringement?

My website has a lot of unique content I’ve either created myself or

outsourced but it appears a lot of it is popping it up all over the internet without

my authorization. Do you know any ways to help reduce content from being stolen? I’d genuinely appreciate it.

What a stuff of un-ambiguity and preserveness of precious familiarity

concerning unexpected feelings.

Have you ever thought about writing an e-book or guest authoring on other blogs?

I have a blog based upon on the same information you discuss and would really like to have you share some

stories/information. I know my audience would value your work.

If you are even remotely interested, feel free to send

me an e-mail.

how to use tinder , what is tinder

tinder website

certainly like your web-site however you need to test the spelling on quite a few of your posts. Several of them are rife with spelling problems and I to find it very bothersome to inform the reality nevertheless I will definitely come back again.

I view something truly special in this internet site.

Nice post. I was checking continuously this blog and I am impressed! Very useful info specifically the last part 🙂 I care for such info a lot. I was looking for this certain info for a very long time. Thank you and best of luck.

Wonderful beat ! I wish to apprentice while you amend your web site, how can i subscribe for a blog web site? The account aided me a acceptable deal. I had been tiny bit acquainted of this your broadcast offered bright clear idea

Its like you read my mind! You appear to know so much about this, like you wrote the book in it or something. I think that you can do with some pics to drive the message home a little bit, but instead of that, this is great blog. An excellent read. I’ll definitely be back.

Hi, Neat post. There’s a problem together with

your website in internet explorer, could test this?

IE still is the market chief and a huge component to other folks will omit your

fantastic writing because of this problem.

You can certainly see your skills within the

work you write. The arena hopes for even more passionate

writers like you who aren’t afraid to mention how they believe.

All the time go after your heart.

how to use tinder , what is tinder

tinder login

Yes! Finally something about asmr.

This is very interesting, You’re a very skilled blogger.

I have joined your rss feed and look ahead to in search of extra of your excellent post.

Also, I have shared your web site in my social networks

Hi i am kavin, its my first time to commenting anywhere, when i read this post i thought i could also create comment due to this sensible post.

tinder online , tinder website

http://tinderentrar.com/

levitra wholesale no prescription

Hi! Do you use Twitter? I’d like to follow you if that would be ok. I’m definitely enjoying your blog and look forward to new updates.

scoliosis

Do you have a spam issue on this site; I also am a blogger, and I was

wondering your situation; many of us have developed some nice practices and we are looking to trade methods with other folks, be sure to shoot me an e-mail if

interested. scoliosis

scoliosis

Excellent beat ! I wish to apprentice while you amend your web site,

how can i subscribe for a blog site? The account helped me a acceptable deal.

I had been tiny bit acquainted of this your broadcast offered bright clear idea scoliosis

scoliosis

What’s up to all, how is the whole thing, I think every one is

getting more from this website, and your views are pleasant for new people.

scoliosis

dating sites

Howdy very cool website!! Man .. Beautiful .. Superb ..

I’ll bookmark your website and take the feeds

additionally? I’m happy to find a lot of useful information here in the submit, we

need develop more strategies on this regard,

thank you for sharing. . . . . . https://785days.tumblr.com/ dating sites

free dating sites

Hey I know this is off topic but I was wondering if

you knew of any widgets I could add to my blog that automatically tweet my newest twitter updates.

I’ve been looking for a plug-in like this for quite some time and was

hoping maybe you would have some experience with something like this.

Please let me know if you run into anything.

I truly enjoy reading your blog and I look forward to your new updates.

dating sites

Simply desire to say your article is as surprising. The clarity in your

post is simply cool and i can assume you’re an expert

on this subject. Fine with your permission let me to grab your feed to keep up to

date with forthcoming post. Thanks a million and please keep up the gratifying work.

This blog is definitely rather handy since I’m at the moment creating an internet floral website – although I am only starting out therefore it’s really fairly small, nothing like this site. Can link to a few of the posts here as they are quite. Thanks much. Zoey Olsen

May I just say what a relief to discover someone who really understands what they’re discussing over the internet.

You actually know how to bring a problem to light and make

it important. A lot more people must check this out and understand this side

of the story. I can’t believe you’re not more popular given that you certainly

have the gift.

Hmm it seems like your website ate my first comment (it was extremely long) so I guess I’ll just sum it up

what I submitted and say, I’m thoroughly enjoying your blog.

I too am an aspiring blog writer but I’m still new to the whole

thing. Do you have any recommendations for inexperienced

blog writers? I’d definitely appreciate it.

Pingback: best completely free dating sites

Marvelous, what a web site it is! This website provides helpful facts to us, keep it up.

I read this paragraph completely about the resemblance of most recent and preceding technologies,

it’s amazing article.

Generally I do not read article on blogs, but I would like to say that this write-up very compelled me to try and do it!

Your writing taste has been amazed me. Thanks, quite nice post.

Great post. I was checking continuously this blog and I

am impressed! Extremely helpful information specially the last part :

) I care for such info much. I was looking for this particular

information for a very long time. Thank you and best of luck.

Hello, yup this piece of writing is actually good and I have learned

lot of things from it concerning blogging. thanks.

Thanks for any other great post. Where else may anyone

get that kind of info in such a perfect method of writing?

I’ve a presentation subsequent week, and I’m at the look for

such information.

Unquestionably consider that that you stated. Your favourite reason seemed

to be at the internet the simplest thing to be aware of. I say to you, I certainly get irked at the same time as other folks consider issues that they plainly don’t recognise about.

You managed to hit the nail upon the top as neatly as defined out the entire

thing without having side-effects , folks could take a signal.

Will probably be again to get more. Thank you

kamagra chewable 100 mg canada

finasteride tablets for sale

Absolutely written content, thanks for selective information.

Just what I was searching for, appreciate it for posting.

I got good info from your blog

Thank you for another fantastic post. Where else may just anybody get that type of info in such a perfect method of writing? I’ve a presentation subsequent week, and I am on the search for such info.

generic cialis for sale

generic levitra for sale

Great, thanks for sharing this article.Much thanks again. Much obliged.

narayaneeyam book in english pdf Elephorm Facebook Pro Gratuitement bangla chodar golpo book download

I don’t even know the way I finished up here, but I assumed this post was good. I do not realize who you’re however definitely you’re going to a well-known blogger if you happen to are not already 😉 Cheers!

Tableau Peinture Casino Monte Caroo Horaires Casino Moissac Casino Partouche 775

him is hydroxychloroquine a prophylactic scientific https://hydroxychloroquined.online/ – hydroxychloroquine sulfate tablets 200mg vertebral artery hydroxychloroquine azithromycin success

Do you have a spam problem on this blog; I also am a blogger, and I was curious about your situation; we have created some nice procedures and we are looking to swap strategies with other folks, be sure to shoot me an e-mail if interested.

Postuler Chez Geant Casino Salaire Agent De Securite Casino Barriere Casino Le Puy 1er Mai

I respect your work, appreciate it for all the interesting content.

You really make it appear really easy along with your presentation however I to find this matter to be actually something that I believe I’d by no means understand. It kind of feels too complex and extremely large for me. I am taking a look forward on your subsequent put up, I?¦ll try to get the grasp of it!

I am incessantly thought about this, regards for posting.

I have been browsing on-line more than 3 hours as of late, yet I never found any interesting article like yours. It’s pretty worth sufficient for me. In my view, if all site owners and bloggers made excellent content material as you probably did, the internet might be much more useful than ever before.

After I originally commented I clicked the -Notify me when new comments are added- checkbox and now every time a remark is added I get 4 emails with the same comment. Is there any manner you’ll be able to remove me from that service? Thanks!

This site is my inspiration , rattling good style and design and perfect written content.

When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

I am really enjoying the theme/design of your site. Do you ever run into any internet browser compatibility issues? A couple of my blog audience have complained about my website not working correctly in Explorer but looks great in Chrome. Do you have any ideas to help fix this issue?

Thanks for another informative web site. Where else could I get that kind of info written in such a perfect approach? I have a venture that I am simply now operating on, and I have been on the look out for such information.

Deference to post author, some wonderful information .

My brother suggested I might like this website.

He was entirely right. This post actually made

my day. You cann’t imagine just how much time I had spent for this info!

Thanks! https://buszcentrum.com/nolvadex.htm

My brother suggested I might like this website. He was entirely right.

This post actually made my day. You cann’t imagine just how much time I had spent for this info!

Thanks! https://buszcentrum.com/nolvadex.htm

Hello, Neat post. There’s an issue together with your web

site in internet explorer, might check this?

IE still is the marketplace chief and a large part of folks will miss your excellent writing because

of this problem.

viagra next day delivery viagra from doctors in melbourne – viagra us overnight mastercard accepted

I have been reading out a few of your stories and i must say clever stuff. I will make sure to bookmark your blog.

I truly appreciate this post. I have been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thx again

I found your weblog website on google and verify just a few of your early posts. Continue to maintain up the excellent operate. I just extra up your RSS feed to my MSN Information Reader. Seeking forward to reading more from you later on!…

Woh I love your articles, saved to fav! .

que es viagra generic viagra scam ViagraCND100Mg – viagra in india chennai

You got a very superb website, Glad I discovered it through yahoo.

Pretty nice post. I just stumbled upon your weblog and wanted to say that I have really enjoyed browsing your blog posts. In any case I will be subscribing to your feed and I hope you write again very soon!

Perfect piece of work you have done, this website is really cool with good info .

Undeniably consider that which you stated. Your favorite reason appeared to be on the internet the easiest thing to be aware of. I say to you, I definitely get annoyed at the same time as folks consider concerns that they just don’t understand about. You managed to hit the nail upon the top and defined out the entire thing with no need side-effects , people can take a signal. Will probably be again to get more. Thank you

But a smiling visitant here to share the love (:, btw outstanding style and design.

Right away I am ready to do my breakfast, once having my breakfast coming yet again to read more news.

It’s a pity you don’t have a donate button!

I’d without a doubt donate to this fantastic blog!

I guess for now i’ll settle for bookmarking and adding your RSS feed to my Google account.

I look forward to brand new updates and will share this website with my Facebook group.

Talk soon!