Update 755 — Focus on Entitlements:

Proper Scope of a Fiscal Commission

For the first time since World War II, the U.S. federal debt held by the public, about $27 trillion, is approaching the nation’s gross domestic product of a single year. Furthermore, on current trends, the Social Security and Medicare Trust Funds are headed to insolvency in 2034 and 2031, respectively. Bills to address deficits and the debt by establishing a fiscal commission are making their way through Congress.

But what is the relationship between deficits and the trust funds? Whatever the merits of a proposed fiscal commission to focus on the former, the status of the latter, the Social Security and Medicare trust funds, is a separate matter: nothing done to secure the trust funds directly bears on the nation’s fiscal condition. Today, we examine the relationship between debt and deficits on the one hand and entitlement trust funds on the other.

Best,

Dana

Social Security and Medicare benefits could see automatic cuts of 20 and 11 percent, respectively, should they reach insolvency within the next 10 years, as projected. Barring legislative action to address funding shortfalls amounting to “insolvency,” cuts will be needed to match benefit outlays with trust fund revenue. Concerns about the future state of Social Security and Medicare and the rapidly increasing national debt/deficit have spawned support for a fiscal commission to issue proposals addressing these issues, outside the usual legislative process in Congress. Though legislation to establish a fiscal commission was adopted by the House Budget Committee last month in a 22-12 vote, its path forward is uncertain amidst Democratic concerns about cuts to Social Security and Medicare benefits and Republican apprehension about tax increases to boost general revenue.

If Congress does move forward with legislation for a fiscal commission, safeguards will be needed to prevent cuts to earned benefits (often contentiously referred to as “entitlements”) that millions of Americans rely on. Not only have fiscal commissions frequently failed to enact reform in the past, but, despite common misconception, Social Security and Medicare are outside the scope of a debt commission as their trust funds are almost entirely self-funded and not subject to the annual appropriations process.

Policy to secure Social Security and Medicare benefits must focus on generating revenue by taxing high-income earners to ensure that liabilities are not increased for the most vulnerable Americans. Blueprints for solutions that would shore up trust funds have been presented in the Social Security 2100 Act and the President’s FY 2024 Budget and should be considered separately from concerns about the national debt.

Social Security, Medicare, and the National Debt

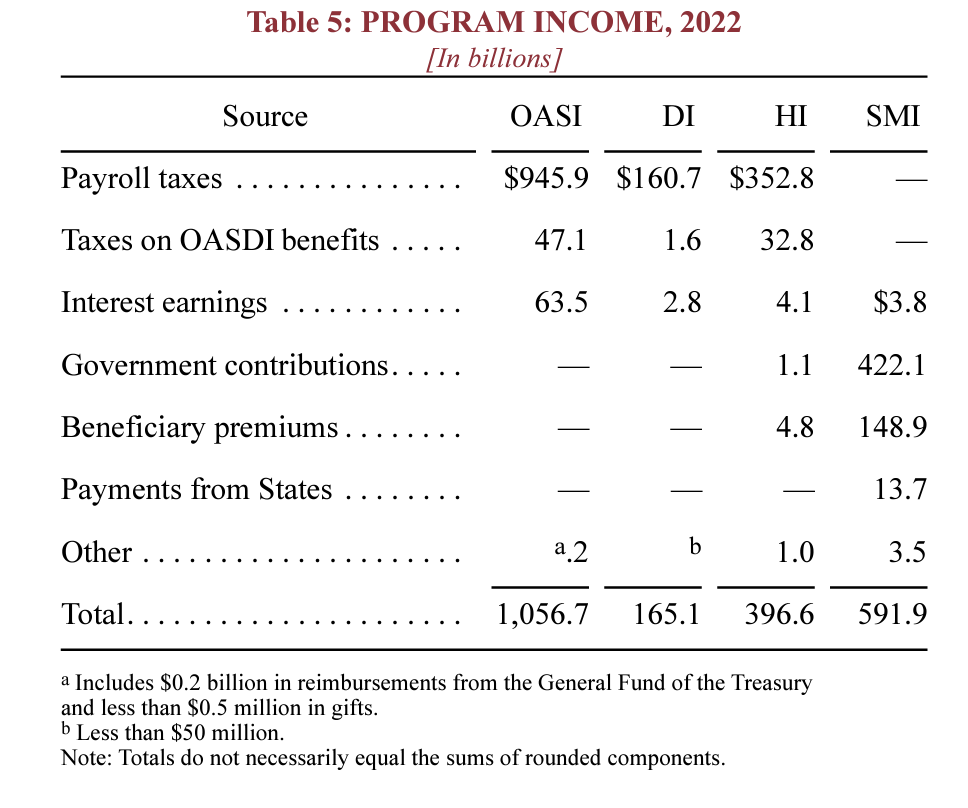

The discussion around entitlement trust funds is often primarily focused on the Hospital Insurance Trust Fund (Medicare), the Old Age and Survivors Insurance Trust Fund (Social Security), and the Disability Insurance Trust Fund (Social Security). These PAYGO trust funds receive very little funding from general revenues (~$1.1 billion in FY 2022) and do not contribute much to the national debt/deficit. Instead, they are almost entirely funded through payroll taxes listed as “Medicare” and “Social Security” on pay stubs and W-2s.

The Supplemental Medical Insurance Trust Fund, a secondary component of Medicare, allows individuals to purchase additional coverage and is supplemented by a considerable amount of general revenues (~$422 billion in FY22). This program does contribute to the national debt/deficit but provides much-needed coverage to more than 14 million Americans.

The table below from the summary of the 2023 Social Security and Medicare Trustees Annual Report shows the program income for each trust fund:

Source: SSA

OASI and HI Trust Funds Face Funding Shortfalls

The Old-Age and Survivors Insurance (OASI) and Hospital Insurance (HI) Trust Funds are on track to become insolvent within the next decade, according to the Social Security and Medicare Boards of Trustees. Projected shortfalls are primarily due to rising healthcare expenditures and baby boomers retiring at a faster rate than younger generations are joining the workforce. Though insolvency is often equated to bankruptcy, the trust funds will be able to pay out benefits at a reduced rate.

The OASDI Trust Fund, which is an aggregate of the two trust funds for Social Security (OASI and DI), is on track to realize funding shortfalls in 2034. At that time, benefits will have to be cut by 20 percent according to the 2023 Social Security Board of Trustees report. The HI Trust Fund, which pays Medicare Part A inpatient hospital expenses, will be able to pay scheduled benefits until 2031 at which point benefits will have to be cut by 11 percent. Even in the case of insolvency, these programs will not contribute to the national debt or deficit under the current design.

Fiscal Commission as a Stalking Horse for Benefit Cuts

Despite the common conflation of major entitlement trust funds and the national debt, members of Congress have continually attributed concerns about our fiscal future to mandatory spending, including Social Security and Medicare. To help address the growing national debt and deficit, legislation has been proposed in the House and the Senate to establish a bipartisan, bicameral fiscal commission. Most Democrats worry that a fiscal commission would be a “stalking horse” for benefit cuts as higher weight would be given to fiscal impacts as opposed to the importance of benefits. Traditionally, commissions have focused on spending cuts over revenue-raising proposals needed to ensure future benefits.

The Fiscal Commission Act of 2023, introduced by Representatives Bill Huizenga (R-MI) and Scott Peters (D-CA), passed out of the House Budget Committee three weeks ago in a 22-12 vote. In addition to stabilizing the debt-to-GDP ratio, “any recommendations related to Federal programs for which a Federal trust fund exists” would need to “improve solvency for a period of at least 75 years.”

During the committee markup for the Fiscal Commission Act of 2023, four amendments were proposed by Democrats to prevent benefits from being cut and expand the revenue base of Social Security and Medicare, among other things. None of them were passed by House Budget members.

Though proponents of a fiscal commission like House Budget Chair Jodey Arrington (R-TX) have noted that cuts are the status quo given projected funding shortfalls, their refusal to accept amendments that would secure benefits for those who rely on Social Security and Medicare betrays and perpetuates an issue conflation and raises questions about the true motives behind a commission.

Securing social programs that do not rely heavily on general revenues for their continued operation should not be confused with policy to reduce the national debt. Keeping the issues properly separate would avoid making decisions about benefits in pursuit of lowering government spending alone. It would also allow experts on Social Security and Medicare to take a bigger role in the process. Members and outside experts appointed to a fiscal commission focused on the national debt may not be equally suited to tackle unique issues that are driving projections for trust fund shortfalls.

Whether Congress chooses to address Social Security and Medicare through the formation of a separate commission/task force, or the traditional legislative process, there are multiple paths forward to prevent harmful cuts to previously promised benefits.

Social Security 2100: Secure SS Benefits for 32 Years

The Social Security 2100 Act, sponsored by Representative John Larson (D-CT), would prevent scheduled benefit cuts by increasing revenue for the Social Security Trust Funds. Additional revenue would be collected by changing the FICA cap for the payroll tax and adding a net investment income tax (NIIT) for high earners, financing the program for an additional 32 years and temporarily expanding benefits.

- Social Security FICA cap

Currently, only $168,600 of earned income is subject to the payroll tax that collects revenue for the Social Security Trust Funds. The Social Security 2100 Act would reinstate the Social Security payroll tax for income above $400,000 (less than 2 percent of Americans) with diminishing returns in associated retirement benefits.

- Net Investment Income Tax

The Social Security 2100 Act would enact a 12.4% NIIT for those who make over $400,000 a year to prevent taxpayers from taking advantage of loopholes that allow them to pay lower FICA tax rates on investment income.

Biden Proposal: Secure Medicare for 25 Years

President Biden’s FY 2024 Budget presented a way to protect full Medicare benefits for at least 25 years while accomplishing program reform that lowers costs for beneficiaries. The Biden Administration’s proposal would finance reform and prevent automatic benefit cuts by:

- increasing the Medicare Payroll Tax rate from 3.8 percent to 5 percent for income over $400,000,

- closing loopholes in Medicare’s Net Investment Income Tax and ensuring this money goes directly toward to HI Trust Fund, and

- giving savings from prescription drug reform proposed in the President’s budget directly to the HI Trust Fund.

These changes would help the millions of Americans who rely on Medicare for their health and well-being while only marginally increasing tax liabilities for high-income earners. President Biden is expected to release revenue-raising proposals for Social Security as well in his FY 2025 Budget, which will be released on March 11 of this year.

Conclusion

The above solutions have one thing in common: they focus on taxing high-earners to strengthen the Social Security and Medicare trust funds and expand benefits for those with the greatest need. To some, increased taxes on high earners may be viewed as “discriminatory” against those who do not rely on program benefits. But benefit cuts would similarly be discriminatory — or worse — for lower-income individuals for whom Social Security and Medicare mean avoiding poverty.

Members of Congress should look to comprehensive and progressive reform to secure benefits for millions of Americans. Critically, they must do so outside of a closed-door debt commission that would prioritize cost savings over beneficiaries and exploit confusion about fiscal realities, suggesting an association between Social Security/Medicare Part A and the national debt.