Update 749 — Accelerating a Virtuous Cycle:

CFPB Aims to Cut Predatory Overdraft Fees

Traditionally, overdraft fees charged by banks have been treated as privileged service charges by financial institutions under the Fed’s rules implementing the Truth in Lending Act (TILA). In the decades since the loophole was created, overdraft fees became profit centers for many large banks, producing over $12 billion in revenues a year, falling mainly on customers least able to afford them. In recent years, under competitive and political pressure, and following new supervisory and enforcement action, some banks have begun curtailing overdraft policies.

Last week, the Consumer Financial Protection Bureau proposed a rule that would build on this progress, which has already cut overdraft revenues by over $3 billion a year. A battle by banks resisting the proposed rule is on, with firms hoping to delay its implementation until the election of an administration that might withdraw it. What would the proposed rule mean for predatory overdraft charges? See below.

Best,

Dana

CFPB Proposes Rule to Rein in Excessive Overdraft Fees

Last week, the Consumer Financial Protection Bureau (CFPB) proposed a new rule to limit excessive predatory overdraft fees charged by the largest financial institutions in America. The rule would close a loophole that banks have long used to extract billions in profit, overwhelmingly from their least wealthy customers.

The CFPB’s proposal, “Overdraft Lending: Very Large Financial Institutions,” would apply to insured financial institutions, including banks and credit unions, with over $10 billion in assets, covering the roughly 175 largest depository institutions in the country.

While financial institutions are providing credit when they cover an overdraft, the Federal Reserve Board created a loophole in its rules implementing the Truth in Lending Act (TILA) that carved out an exemption to Truth in Lending protections for banks honoring a check or other overdraft when depositors “inadvertently” overdraw their accounts. Under CFPB’s proposed rule, covered firms would have two choices. They could cover overdrafts through transparent overdraft lines of credit, which would be required to provide clear lending disclosures and the other protections required for credit cards and other loans. Alternatively, they could charge a lower overdraft fee in line with their costs or with established benchmarks of $3 to $14, to be decided by the CFPB in the rulemaking.

The proposed rule would do this by updating non-statutory exceptions in CFPB Regulation Z, which protects customers when they use consumer credit. The proposed rule would move overdraft credit out of Regulation Z and into CFPB Regulation E, which protects consumers when they use electronic fund and remittance transfers.

The proposed change in policy would likely lower overdraft fees, typically $35 today — even though the majority of consumers’ debit card overdrafts are for less than $26 and are repaid within three days. The CFPB estimated that the rule might save consumers $3.5 billion or more in fees per year, translating to $150 in potential savings for households that pay overdraft fees, on top of $3.5 billion that has already been saved through voluntary changes at some banks.

Overdraft: Convenience Fee to Big-Bank Profit Center

Financial institutions charge consumers an overdraft fee when they honor a check or electronic payment despite a consumer having insufficient funds to cover it. Financial institutions may issue a loan, which consumers repay when a deposit is made to their account, to cover the difference in these instances.

In the 1960s, consumers typically withdrew funds from their bank accounts through in-person withdrawals or by writing checks. They also regularly received and sent checks through the mail, making it difficult for consumers to know when their deposits and withdrawals would clear. Overdraft services were an occasional courtesy provided by banks to help their customers avoid the negative consequences of a bounced check if they inadvertently overdrew their account. Overdraft, and by extension its fees, remained an infrequently used modestly-priced convenience until financial institutions widely adopted information technology systems and debit card transactions that can overdraw accounts expanded in the 1990s and early 2000s.

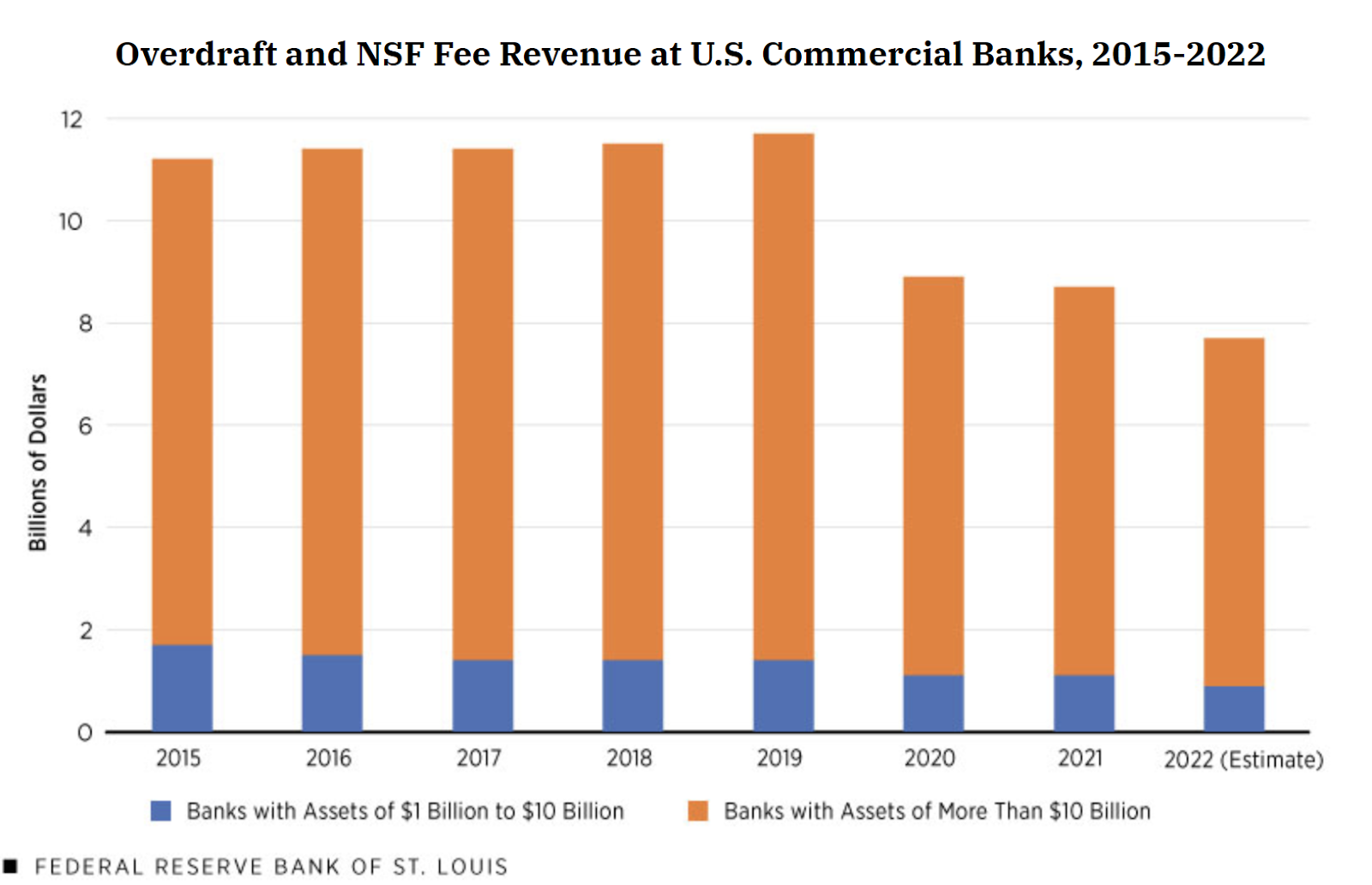

Although paying consumers’ occasional or inadvertent overdrafts was not a long-established customer service, in 2005, the Federal Reserve Board created an exemption for overdraft fees in the rules implementing TILA. Banks then began exploiting the overdraft fee loophole, utilizing overdrafts as a profit center. By 2019, annual overdraft fee revenue was an estimated $12.6 billion.

Financially disadvantaged families and individuals are hit particularly hard by overdraft fees. The CFPB has found that just nine percent of accounts with a median balance of $350 generated 80 percent of all overdraft revenue. Furthermore, lower-wage workers, young people, people of color, and consumers living paycheck to paycheck pay a disproportionate share of overdraft fees. A 2021 Bankrate survey found that Black and Hispanic consumers were respectively 1.9 and 1.4 times more likely to pay an overdraft fee on checking than white consumers.

In 2021, the CFPB began to focus substantial enforcement and supervision attention on overdraft fees. In response, some banks significantly lowered or outright eliminated overdraft fees. Seven of the twenty banks that reported the most overdraft or non-sufficient fund fees (NSFs) revenue during 2021 reduced or eliminated overdraft fees in 2021 or 2022.

Source: Federal Reserve Bank of St. Louis

Despite these proactive efforts taken by individual banks, big banks still make billions of dollars from overdraft fees. Overdraft revenue remains at about $9 billion per year. Last year, the ten largest banks still using overdraft fees – including JPMorgan Chase & Co. and Wells Fargo – extracted over $2.34 billion from the practice.

Overdraft fees also continue to surprise many consumers who are hit by them. A December 2023 report by the CFPB that considered consumers’ experiences with overdrafts and NSF fees at large banks found that over two in five consumers (43 percent) charged an overdraft fee in the past year were surprised by their most recent account overdraft. Only 22 percent of consumers expected their most recent overdraft charge.

More Work Ahead on Financial Junk Fees

20/20 Vision applauds the CFPB’s continued work to rein in junk fees, including overdraft fees, and encourages the CFPB to finalize a strong rule limiting overdraft fees in a timely manner.

The proposal has received support from President Biden, who referred to the CFPB’s proposal as “part of my Administration’s broader plan to lower costs for hardworking families.” Despite the estimated savings for the most financially vulnerable Americans, Republicans on the House Financial Services Committee have said that the proposal would raise the cost of banking for all consumers. They also claim that the proposal would diminish financial inclusion although overdraft fees are one of the leading reasons that people become or remain unbanked.

Republicans on the Senate Committee on Banking, Housing, and Urban Affairs have opposed the CFPB’s efforts to rein in exploitative overdraft fees since April of last year when they wrote a letter to CFPB Director Rohit Chopra claiming that overdraft fees help the very consumers burdened by the charges. Americans, however, appear to disagree. A poll released late last year found that Americans across political, geographic, and demographic lines cite rising costs as the most pressing issue facing the country today, with 60 percent believing that “crack[ing] down on price gouging by banning hidden junk fees” would be effective at lowering costs. Americans broadly support the Administration’s effort to protect consumers rather than corporations.

Banking industry opponents of the proposal have suggested that consumers want and are willing to pay for overdraft fees, framing these charges as a helpful form of credit banks offer to those who need it. But the CFPB proposal would allow banks to continue providing overdraft protection as long as they did it with lower fees or honest and transparent overdraft lines of credit. The fact that over 40 percent of consumers who incurred overdraft fees or NSF fees in the past year were surprised by these charges suggests that consumers are not actually making a conscious decision to access needed credit through overdraft protection rather than other available forms of credit that may be cheaper.

While the proposal would significantly impact the overall overdraft revenue raked in by the largest banks and credit unions, financial institutions with under $10 billion in assets would continue to be allowed to exploit the overdraft fee loophole. The CFPB said that it would continue to monitor overdraft fee practices by smaller institutions, and it is possible that it will expand the rule in the future.

The CFPB is seeking comments on all aspects of the proposal, including whether benchmarks identified in the proposal are appropriate and whether the date suggested for the proposal to take effect should be adjusted. The comment period on the proposal will close on April 1. The CFPB proposal aims for a final rule relating to this proposal to become effective on October 1.