Update 761 — Biden’s SOTU: Opening Salvo

Offers Contrast on Economic Policy Priorities

In last night’s State of the Union, President Biden delivered a forceful reprisal of the powerful American economic recovery and proposed measures to build on it — cutting costs, protecting and expanding programs, and making the wealthy pay their fair share in taxes. He referred repeatedly to his predecessor and November opponent, though not by name, drawing stark contrasts with Trump. While little mention was made of the post-pandemic economic insecurity felt by a majority of Americans, Biden made clear the differences in their priorities.

Fed chair Jerome Powell indirectly addressed this anxiety, testifying before Congress twice this week, suggesting that the Fed is nearing comfort with the progress made on inflation and the time when the Fed can finally cut interest rates. We also heard from Super Tuesday voters, who, in every state, all but determined a November rematch between Biden and Trump, though turnout lagged. We cover these and key economic developments of the week below.

Good weekend, all…

Best,

Dana

State of the Union Reprisal

President Biden, lagging in polling on the state of the economy and underwater on policy dis/approval, delivered a pointed State of the Union address last night, highlighting the economic successes of his administration’s first term and offering numerous proposals — particularly on tax policy — in a campaign-style pitch to American voters as he tees up to battle Trump for a second time.

He touted the economy’s strong post-COVID recovery, with wages rising, inflation continuing to fall and unemployment remaining at historic lows, while also praising his administration’s $1.2 trillion investment in infrastructure. In addressing the affordable housing crisis, Biden proposed a pair of new tax credits to encourage homeownership and called on Congress to pass legislation to build and renovate over two million homes.

The President also lifted up his administration’s work to promote corporate tax fairness, which has vowed to raise the corporate tax rate from 21 to 28 percent and increase the 15 percent Corporate Minimum Income Tax – a Biden policy that kicked in this tax year – to 22 percent. Biden pitched a 25 percent billionaire income tax for the wealthiest 0.01 percent of Americans worth over $100 million and highlighted his administration’s efforts to protect American consumers from junk fees and price gouging by corporations padding their bottom lines by charging “more and more for less.”

Biden delivered a strong message in support of protecting and expanding Social Security, calling out Republican attacks on the program. A more detailed proposal for the program is expected to be outlined in the administration’s FY25 budget, which will be released on Monday.

Headline

Congress Passes First FY24 Spending Package

This week, Congress looks on track to approve funding for a $459 billion funding package consisting of six of the twelve FY 2024 appropriations bills. Despite longstanding concerns from Democrats, the package is relatively clean of harmful policy riders, negotiations on which have extended the FY24 appropriations process well into the fiscal year.

Among Democratic wins are an increase of $1 billion in funding for the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) and the defeat of a rider that aimed to limit food choices for SNAP nutrition assistance recipients. Though the package does not contain everything that Democrats could hope for, it can be considered a best-case outcome in the context of tight non-defense discretionary caps set in the Fiscal Responsibility Act (FRA) last summer.

The package passed the House on Wednesday in a 339-85 vote, with slightly more Republicans supporting the measure than last week’s Continuing Resolution (CR). The Senate voted to advance the funding legislation out of the amendment process 63-35, setting up a vote for final passage later this afternoon.

Next comes the second and last tranche of appropriations bills, which contains funding for controversial areas like health and human services and homeland security — expected to be much harder to negotiate, as it represents about 70 percent of the discretionary budget. In the coming weeks, Congressional leadership will attempt to resolve differences on policy riders that could endanger the second package’s path to the finish line before its provisions’ funding expires on March 22. The National Leadership Conference on Human Rights provided an extensive summary of riders to watch out for as these negotiations develop in a letter sent to Congress this week.

House Budget Passes FY2025 Budget Resolution

With the contentious FY 2024 funding fight still unresolved, the House Budget Committee released its budget resolution for FY 2025 on Wednesday night ahead of the State of the Union address. The extreme proposal — which will never become law — looks much like the House Budget resolution put forth last September for FY 2024 and would make trillions of dollars in cuts to discretionary and mandatory programs while lowering taxes and associated federal revenue. The budget framework includes language for a fiscal commission that would likely cut Social Security and Medicare, work requirements for Medicaid recipients, and an additional $35 billion cut to IRS enforcement funding from the Inflation Reduction Act (IRA).

While budget resolutions themselves do not provide funding for the government, they do lay out goals for revenues and spending. In this case, the budget resolution was used by the conservative House majority to send a message about their budget priorities. Congress will have to hash out differences through normal order.

The House Budget Committee held a markup for the budget resolution on Thursday, which Republicans used to focus narrowly on the role government spending has in accelerating the national debt. Though the growing national debt is a major concern, Republicans’ targeting of popular social programs that millions of Americans rely on over revenues further highlights their backward priorities. The budget resolution was passed out of the Budget Committee along party lines following Thursday’s markup.

President Biden will release his own budget proposal for FY25 on Monday following its soft launch during last night’s State of the Union address. It is expected to include revenue provisions (i.e. tax increases for the wealthy and corporations) and an expansion of important programs like Social Security, completely contradictory to the latest House Budget proposal. The distance between House proposals and what is expected to be included in President Biden’s framework accelerates concerns surrounding the FY 2025 funding process even before FY 2024 has concluded.

Other Developments

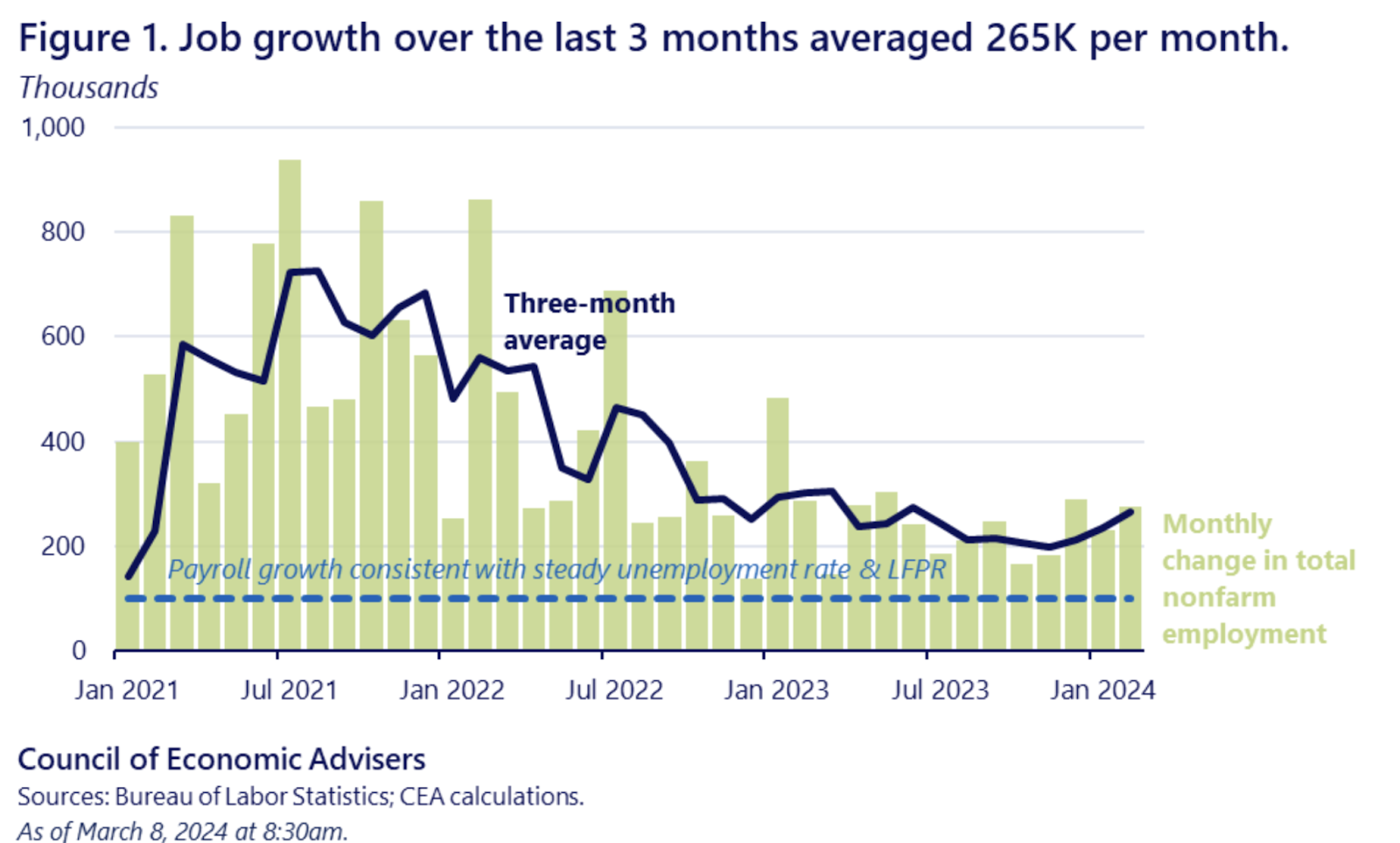

275,000 Jobs Added in February; Labor Market Strong

This morning’s jobs report shows the labor market remaining remarkably strong for yet another month. Total nonfarm payroll employment rose by 275,000 in February, exceeding expectations. The unemployment rate ticked up by 0.2 percent to 3.9 percent last month, remaining at the historically low level of below four percent for the twenty-fifth consecutive month.

Source: Council of Economic Advisors

The largest gains came in health care, government, food services and drinking places, social

assistance, and transportation and warehousing. No major industries lost a substantial number of jobs over the month. Job growth in December and January were revised down by a total of 167,000 jobs, reflecting higher volatility during this part of the year, with December’s total being revised down by 43,000, from +333,000 to +290,000 and January’s total being revised down by 124,000, from +353,000 to +229,000.

The labor force participation rate remained steady at 62.5 percent last month for the third consecutive month. Average hourly earnings were up by 0.1 percent in February and 4.3 percent over the year.

The strong jobs report is unlikely to have a major influence on the Federal Open Market Committee when it meets in two weeks to decide the fate of interest rates. Fed Chair Jerome Powell noted at the conclusion of the Committee’s last meeting in January that the Fed is not looking to see a weakening in the labor market before it begins cutting rates. Fed officials will likely be paying closer attention to consumer price index data for February which will be released on Tuesday, hoping to see inflation continuing its trend towards the Fed’s target of two percent on an annualized basis.

CFPB Releases Final Rule Cutting Credit Card Late Fees

On Tuesday, the Consumer Financial Protection Bureau (CFPB) released its final credit card late fee rule which will reduce the typical credit card late fee from $32 to $8. According to the Bureau, the rule will save American families an estimated $10 billion in late fees annually, translating to an average savings of $220 per year for the more than 45 million people who are charged late fees.

The CFPB has found that in 2022, credit card issuers raked in over $14 billion in late fee revenue, more than five times the associated costs to issuers. Credit card late fees continue to be the most significant fee assessed to cardholders in both dollar amount and frequency and disproportionately affect low- and moderate-income consumers and people of color at a time when credit card debt has reached historic highs.

The final rule will become effective 60 days after it is published in the federal register.

President Biden highlighted the rule as he discussed his administration’s broader effort to tackle junk fees and protect American families from corporate greed.

Hearings

Powell’s Testimony on Endgame and Other Regs

Federal Reserve Chair Jerome Powell testified before the House Committee on Financial Services and the Senate Committee on Banking, Housing, and Urban Affairs this week as he delivered the Fed’s Semi-Annual Monetary Policy Report in what are known as the Humphrey-Hawkins hearings.

Federal banking regulators’ Basel III Endgame proposal received attention from members on both sides of the aisle with Republicans calling for the proposal to be withdrawn and several Democrats raising concerns. In his opening statement, Senate Banking Committee Chair Sherrod Brown (D-OH) called for the rule to be finalized. Powell said that he expected “broad and material changes to the proposal.” The joint proposal by the Fed, FDIC, and OCC would implement stricter capital requirements on banking firms with $100 billion or more in total assets as well as firms that engage in significant trading activities. It would effectively enhance the financial system’s ability to withstand periods of stress like the one seen following the collapse of Silicon Valley Bank and other firms last spring. Powell noted that the Fed was reviewing comments following the close of the public comment period earlier this year.

Several legislators asked the Fed Chair whether he still considered the commercial real estate (CRE) identified by the Financial Stability Oversight Council (FSOC) in its annual report to be manageable. Powell stated that he expected some financial institutions to experience losses and noted that small- and medium-size banks have higher concentrations of commercial real estate loans. Responding to questions from Representatives Jim Himes (D-CT) and Stephen Lynch (D-MA), Powell said that the Fed was in touch with relevant banks to make sure that they have a plan to deal with the risk.

Powell also faced questions about the need to finalize Section 956 of the Dodd-Frank Act, which requires a rule to ban incentive-based executive compensation that encourages “inappropriate” risk-taking. Banning compensation packages that encourage high-risk behavior would be a powerful tool in protecting society from the harms of banking crises. But the May 2011 deadline set by Congress to put Section 956 rules into force passed over 12 years ago, and still, a final rule has yet to be finalized. Powell failed to commit to helping finalize such a rule this year when pressed by Representative Rashida Tlaib (D-MI), saying “I would like to understand the problem we’re solving and then I would like to see a proposal that addresses that problem.” Representative Nydia Velázquez (D-NY) also stressed the importance of finalizing such a rule.

HFSC Considers Bills that Could Harm Consumers

The House Committee on Financial Services Subcommittee on Financial Institutions and Monetary Policy convened on Thursday morning to consider four bills during a hearing on the impact of financial regulation on consumer credit and community development.

The hearing considered:

- H.R. 3161, the CDFI Fund Transparency Act

- H.R. 6789, the Rectifying UDAAP Act

- The Secure Payments Act

- A bill to amend the Truth in Lending Act to allow covered entities to offer small-dollar credit products, and for other purposes

In his opening remarks, Subcommittee Ranking Member Bill Foster laid out the Consumer Financial Protection Bureau’s broad success in protecting American consumers from unfair and deceptive practices, including its securing of $20 billion in relief for harmed consumers. Witness Santiago Sueiro, Senior Policy Analyst at Unidos US emphasized the Bureau’s critical role in securing a fair marketplace. Their strong defense followed attacks from Subcommittee Chair Andy Barr (R-KY). Despite the Bureau’s broad popularity and continued work to protect the American people, Barr and Republicans used the hearing to once again label the Bureau as partisan and seek to undermine its ability to continue to deliver.

Look Ahead

Tuesday, March 12

- February CPI report

- Senate Committee on Finance hearing: American Made: Growing U.S. Manufacturing Through the Tax Code

- Senate Committee on Banking, Housing, and Urban Affairs hearing: Examining Proposals to Address Housing Affordability, Availability, and Other Community Needs

- Senate Committee on the Budget hearing: The President’s Fiscal Year 2025 Budget Proposal

- Joint Economic Committee hearing: The Fiscal Situation of the United States

Wednesday, March 13

- House Committee on Financial Services Subcommittee on Financial Technology and Inclusion hearing: Bureaucratic Overreach or Consumer Protection? Examining the CFPB’s Latest Action to Restrict Competition in Payments